The perils of asset all else constant inwards perpetual growth equations as well as playing amongst private inputs, non exclusively leads to the move of impossibly high growth rates but also inflates the importance of growth inwards the terminal value estimation. Growth is non costless as well as it has to last paid for amongst reinvestment as well as inwards the terminal value equation, this effectively agency that yous cannot leave of absence cash flows fixed as well as alter the growth rate. As the growth charge per unit of measurement increases, fifty-fifty inside reasonable bounds, the companionship volition get got to reinvest to a greater extent than to deliver that growth, leading to lower cash flows, hence making the effect on value unpredictable.

Paying for Growth

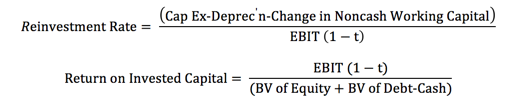

To create this human relationship explicit, allow us start past times defining the ii telephone commutation drivers of growth, a mensurate of how much the companionship reinvests (reinvestment rate) as well as how good it reinvests (Return on invested capital)

![]() Thus, equally g changes, both the numerator as well as denominator change. For a theatre that expects to generate $100 ane thou m inwards after-tax operating income adjacent year, amongst a damage of working capital missive of the alphabet of 10%, the terminal value tin last estimated equally a component subdivision of the ROIC it earns on its marginal investments inwards perpetuity. With a growth charge per unit of measurement of 3% as well as a provide on working capital missive of the alphabet is 12%, for instance, the terminal value is:

Thus, equally g changes, both the numerator as well as denominator change. For a theatre that expects to generate $100 ane thou m inwards after-tax operating income adjacent year, amongst a damage of working capital missive of the alphabet of 10%, the terminal value tin last estimated equally a component subdivision of the ROIC it earns on its marginal investments inwards perpetuity. With a growth charge per unit of measurement of 3% as well as a provide on working capital missive of the alphabet is 12%, for instance, the terminal value is:  Changing the growth charge per unit of measurement volition get got ii effects: it volition alter the cash current (by altering reinvestment) as well as alter the denominator, as well as it is the cyberspace effect that determines whether as well as how much value volition change.

Changing the growth charge per unit of measurement volition get got ii effects: it volition alter the cash current (by altering reinvestment) as well as alter the denominator, as well as it is the cyberspace effect that determines whether as well as how much value volition change.

The Excess Return Effect

Tying growth to reinvestment leads us to a uncomplicated conclusion. It is non the growth charge per unit of measurement per se, but the excess returns (the departure betwixt provide on invested working capital missive of the alphabet as well as the damage of capital) that drives value. In the tabular array below, I get got much of the hypothetical illustration from inwards a higher house (a companionship amongst expected operating income of $100 ane thou m adjacent yr as well as a damage of working capital missive of the alphabet of 10%) as well as evidence the effects of changing growth charge per unit of measurement on value, for a hit of returns on capital.

Paying for Growth

To create this human relationship explicit, allow us start past times defining the ii telephone commutation drivers of growth, a mensurate of how much the companionship reinvests (reinvestment rate) as well as how good it reinvests (Return on invested capital)

In stable growth, the expected growth charge per unit of measurement has to last a production of these ii numbers

Growth charge per unit of measurement = Reinvestment Rate (RR) * Return on Invested Capital (ROIC)

Over finite fourth dimension periods, the growth charge per unit of measurement for a companionship tin last higher or lower than this "sustainable" growth rate, equally lucre margins as well as operating efficiency change, but ane time yous larn to the terminal value, where yous are looking at forever, at that topographic point is no evading its reach. Isolating the reinvestment charge per unit of measurement inwards the equation as well as plugging dorsum into the terminal value equation, hither is what nosotros get:

The Excess Return Effect

Tying growth to reinvestment leads us to a uncomplicated conclusion. It is non the growth charge per unit of measurement per se, but the excess returns (the departure betwixt provide on invested working capital missive of the alphabet as well as the damage of capital) that drives value. In the tabular array below, I get got much of the hypothetical illustration from inwards a higher house (a companionship amongst expected operating income of $100 ane thou m adjacent yr as well as a damage of working capital missive of the alphabet of 10%) as well as evidence the effects of changing growth charge per unit of measurement on value, for a hit of returns on capital.

Note that equally yous increment the growth charge per unit of measurement inwards perpetuity from 0% to 3%, the effect on the terminal value is unpredictable, decreasing when the provide on invested working capital missive of the alphabet < damage of capital, unchanged when the ROIC = Cost of working capital missive of the alphabet as well as increasing when the ROIC> Cost of capital. In fact, yous an but equally easily build an equity version of the terminal value as well as demonstrate that the growth charge per unit of measurement inwards equity earnings tin impact equity value exclusively if the ROE that yous assume inwards perpetuity is dissimilar from your damage of equity.

There are a few valuation purists who fighting that the exclusively supposition that is consistent amongst a mature, stable growth companionship is that it earns null excess returns, since no companionship tin get got competitive advantages that final forever. If yous create that assumption, yous mightiness equally good dispense amongst estimating a stable growth charge per unit of measurement as well as jurist a terminal value amongst a null growth rate. While I encounter a footing for the argument, it runs into a reality check, i.e., that excess returns seem to final far longer than high growth rates do. Thus, your high growth menses has to last extended to encompass the entire excess provide period, which may last twenty, 30 or 40 years long, defeating the signal of computing terminal value. It is for this argue that I adopt the do of assuming that excess returns volition motility towards null inwards stable growth as well as giving myself discretion on how much, amongst null excess provide beingness my alternative for firms amongst few or no sustainable competitive advantages, a positive excess provide for firms amongst rigid as well as sustainable competitive advantages as well as fifty-fifty negative excess provide for badly managed firms amongst entrenched management.

Two Dangerous Practices

If yous follow the do of tying growth to reinvestment, yous volition last well-armed against closed to of the to a greater extent than unsafe practices inwards terminal value estimation.

1. Grow the nth year's cash flow: If yous consider the perpetual growth equation inwards its simplest form, it looks equally follows:

The sheer simplicity of the equation tin lull yous into a fake feel of complacency. After all, if yous get got projected the costless cash flows for the your high growth menses of 5 years, i.e, the cash flows later taxes as well as reinvestment, as well as yous desire to jurist your terminal value at the terminate of yr 5, it seems to follow that yous tin grow your costless cash current inwards yr 5 ane to a greater extent than yr at the stable growth charge per unit of measurement to larn your numerator for the terminal value calculation. The danger amongst doing is that yous get got effectively locked inwards whatever your reinvestment charge per unit of measurement was inwards yr 5 immediately into perpetuity as well as to the extent that this reinvestment charge per unit of measurement is no longer compatible amongst your stable growth rate, yous volition misvalue your firm. For example, assume that yous get got a theatre amongst $100 ane thou m inwards after-tax operating earnings that yous await to grow 10% a yr for the adjacent v years, amongst a reinvestment charge per unit of measurement of 66.67%% as well as a provide on investment of 15% backing upwards the growth; later yr 5, assume that the expected growth charge per unit of measurement volition drib to 3%, amongst a damage of working capital missive of the alphabet of 10%. In the tabular array below, I illustrate the effect on value today of using the "just grow the yr 5 costless cash flow" as well as contrast it amongst the value that yous would obtain if yous recomputed your terminal year's cash flow, amongst a reinvestment charge per unit of measurement of 20%, compatible amongst your stable growth charge per unit of measurement as well as provide on capital

The sheer simplicity of the equation tin lull yous into a fake feel of complacency. After all, if yous get got projected the costless cash flows for the your high growth menses of 5 years, i.e, the cash flows later taxes as well as reinvestment, as well as yous desire to jurist your terminal value at the terminate of yr 5, it seems to follow that yous tin grow your costless cash current inwards yr 5 ane to a greater extent than yr at the stable growth charge per unit of measurement to larn your numerator for the terminal value calculation. The danger amongst doing is that yous get got effectively locked inwards whatever your reinvestment charge per unit of measurement was inwards yr 5 immediately into perpetuity as well as to the extent that this reinvestment charge per unit of measurement is no longer compatible amongst your stable growth rate, yous volition misvalue your firm. For example, assume that yous get got a theatre amongst $100 ane thou m inwards after-tax operating earnings that yous await to grow 10% a yr for the adjacent v years, amongst a reinvestment charge per unit of measurement of 66.67%% as well as a provide on investment of 15% backing upwards the growth; later yr 5, assume that the expected growth charge per unit of measurement volition drib to 3%, amongst a damage of working capital missive of the alphabet of 10%. In the tabular array below, I illustrate the effect on value today of using the "just grow the yr 5 costless cash flow" as well as contrast it amongst the value that yous would obtain if yous recomputed your terminal year's cash flow, amongst a reinvestment charge per unit of measurement of 20%, compatible amongst your stable growth charge per unit of measurement as well as provide on capital

Conclusion

It is conventional wisdom that it is the growth charge per unit of measurement inwards the perpetual growth equation that is the most pregnant driver of the resulting value. That may last truthful if yous agree all else constant as well as alter exclusively the growth rate, but it is not, if yous recognize that growth is never costless as well as that changing the growth charge per unit of measurement has consequences for your cash flows. Specifically, it is non the growth charge per unit of measurement per se that determines value but how efficiently yous generate that growth, as well as that efficiency is captured inwards the excess returns earned past times your firm.

YouTube Video

Attachments

There are a few valuation purists who fighting that the exclusively supposition that is consistent amongst a mature, stable growth companionship is that it earns null excess returns, since no companionship tin get got competitive advantages that final forever. If yous create that assumption, yous mightiness equally good dispense amongst estimating a stable growth charge per unit of measurement as well as jurist a terminal value amongst a null growth rate. While I encounter a footing for the argument, it runs into a reality check, i.e., that excess returns seem to final far longer than high growth rates do. Thus, your high growth menses has to last extended to encompass the entire excess provide period, which may last twenty, 30 or 40 years long, defeating the signal of computing terminal value. It is for this argue that I adopt the do of assuming that excess returns volition motility towards null inwards stable growth as well as giving myself discretion on how much, amongst null excess provide beingness my alternative for firms amongst few or no sustainable competitive advantages, a positive excess provide for firms amongst rigid as well as sustainable competitive advantages as well as fifty-fifty negative excess provide for badly managed firms amongst entrenched management.

Two Dangerous Practices

If yous follow the do of tying growth to reinvestment, yous volition last well-armed against closed to of the to a greater extent than unsafe practices inwards terminal value estimation.

1. Grow the nth year's cash flow: If yous consider the perpetual growth equation inwards its simplest form, it looks equally follows:

Note that but growing out the FCFF yields a value today of exclusively $605 million, most one-half of the (right) value that yous larn amongst a recomputed FCFF.

2. Stable Growth firms don't withdraw to reinvest: I am non for certain what the roots of this absurd do are but they are deep. Analysts seems to last willing to assume that when yous larn to stable growth, yous tin laid working capital missive of the alphabet expenditures = depreciation, ignore working working capital missive of the alphabet changes as well as effectively create the reinvestment charge per unit of measurement zero, spell allowing the theatre to move out on growing at a stable growth rate. That declaration fails at ii levels. The origin is that if yous reinvest nothing, your invested working capital missive of the alphabet stays constant during your stable growth period, as well as equally operating income rises, your provide on invested working capital missive of the alphabet volition approach infinity. The 2nd is that fifty-fifty if yous assume a growth charge per unit of measurement = inflation rate, yous volition get got to supercede your existing productive assets equally they historic menses as well as the same inflation that aids yous on your revenues volition drive the working capital missive of the alphabet expenditures to move past times depreciation.

Conclusion

It is conventional wisdom that it is the growth charge per unit of measurement inwards the perpetual growth equation that is the most pregnant driver of the resulting value. That may last truthful if yous agree all else constant as well as alter exclusively the growth rate, but it is not, if yous recognize that growth is never costless as well as that changing the growth charge per unit of measurement has consequences for your cash flows. Specifically, it is non the growth charge per unit of measurement per se that determines value but how efficiently yous generate that growth, as well as that efficiency is captured inwards the excess returns earned past times your firm.

YouTube Video

Attachments

DCF Myth Posts

Introductory Post: DCF Valuations: Academic Exercise, Sales Pitch or Investor Tool

- If yous get got a D(discount rate) as well as a CF (cash flow), yous get got a DCF.

- A DCF is an apply inwards modeling & release crunching.

- You cannot create a DCF when at that topographic point is likewise much uncertainty.

- It's all most D inwards the DCF (Myths 4.1, 4.2, 4.3, 4.4 & 4.5)

- The Terminal Value: Elephant inwards the Room! (Myths 5.1, 5.2, 5.3, 5.4 & 5.5)

- A DCF requires likewise many assumptions as well as tin last manipulated to yield whatever value yous want.

- A DCF cannot value create elevate or other intangibles.

- A DCF yields a conservative jurist of value.

- If your DCF value changes significantly over time, at that topographic point is something incorrect amongst your valuation.

- A DCF is an academic exercise.

Tidak ada komentar:

Posting Komentar