It's taken me a spell to instruct here, but inwards this, the final of my 10 posts looking at publicly traded companies globally, I aspect at pricing differences across regions together with sectors. I set out my rationale for looking at pricing in my most recent post on the topic, where I drew a distinction betwixt practiced companies, practiced administration together with practiced investments, contestation that investing is well-nigh finding mismatches betwixt reality (as driven yesteryear cash flows, increase together with risk) together with perception (as determined yesteryear the market).

Multiple = Standardized Price

When looking at how stocks are priced together with particularly when comparing pricing across stocks, nosotros almost invariably aspect at pricing multiples (PE, EV to EBITDA) rather than absolute prices. That is because prices per portion are a purpose of the release of shares together with are, inwards a sense, almost arbitrary. Before you lot response alongside indignation, what I hateful to state is that I tin brand the toll per portion decrease from $100/share to $10/share, yesteryear instituting a 10 for 1 stock split, without changing anything well-nigh the company. As a consequence, a stock cannot endure classified every bit inexpensive or expensive based on toll per portion together with you lot tin honor Berkshire Hathaway to endure nether valued at $263,500 per share, spell viewing a stock trading at five cents per portion every bit hopelessly overvalued.

The procedure of standardizing prices is direct forward. In the numerator, you lot involve a marketplace seat mensurate of value of equity, the entire line solid (debt + equity) or the operating assets of the line solid (debt + equity -cash = enterprise value). If you lot confused well-nigh the distinction, you lot may desire to review this postal service of mine from the archives. In the denominator, you lot tin scale the marketplace seat value to revenues, earnings, accounting estimates of value (book value) or cash flows.

As you lot tin see, at that spot is a rattling large release of standardized versions of value that you lot tin calculate for firms, particularly if you lot pick out inwards variants on each private variable inwards the denominator. With cyberspace income, for instance, you lot tin aspect at income inwards the final financial twelvemonth (current), the final twelve months (trailing) or the adjacent twelvemonth (forward). The 1 uncomplicated suggestion that you lot should ever follow is to endure consistent inwards your Definition of multiple.

The "Consistent Multiple" Rule: If your numerator is the marketplace seat value of equity (market capitalization or toll per share), your denominator has to endure an equity mensurate every bit good (net income or earnings per share, volume value of equity. For example, a toll earnings ratio is consistent, since both the numerator together with denominator are equity values, together with therefore is an EV to EBITDA multiple. Influenza A virus subtype H5N1 Price to EBITDA or a Price to Sales ratio is inconsistent, since the numerator is an equity value and the denominator is to the entire business, together with volition Pb to conclusions that are non merited yesteryear the fundamentals.

Pricing – Influenza A virus subtype H5N1 Global Picture

To run into how stocks are priced around the the world at the start of 2017, I focus on iv multiples, the toll earnings ratio, the toll to volume (equity) ratio, the EV/Sales multiple together with EV/EBITDA. With each multiple, I volition start alongside a histogram describing how stocks are priced globally (with sub-sector specifics) together with therefore render set down specific numbers inwards oestrus maps.

PE ratio

The PE ratio has many variants, some related to what menstruation the earnings per portion is measured (current, trailing or forward), some relating to whether the earnings per portion are primary or diluted together with some a purpose of whether together with how you lot arrange for extraordinary items. If you lot superimpose on transcend of these differences the fact that earnings per portion reported yesteryear companies reverberate rattling dissimilar accounting standards around the world, you lot tin already start to run into the caveats gyre out. That said, it is nevertheless useful to start alongside a histogram of PE ratios of all publicly traded companies around the world:

Note that of the 42,668 firms inwards my global sample, at that spot were entirely 25,493 firms that made it through into this graph; the residual of the sample (about 40%) had negative earnings per portion together with the PE ratios was non meaningful. While the histogram provides the distributions yesteryear regional sub-groups, the oestrus map below provides the median PE ratio yesteryear country:

If you lot croak to the alive oestrus map, you lot volition also endure able to run into the 25th together with 75th quartiles inside each country, or you lot tin download the spreadsheet that contains the data. I mistrust PE ratios for many reasons. First, the to a greater extent than accountants tin travel on a number, the less trustworthy it becomes, together with at that spot is no to a greater extent than massaged, manipulated together with mangled variable than earnings per share. Second, the sampling bias introduced yesteryear eliminating a large subset of your sample, yesteryear eliminating coin losing companies, is immense. Third, it is the most volatile of all of the multiples every bit it is based upon earnings per share.

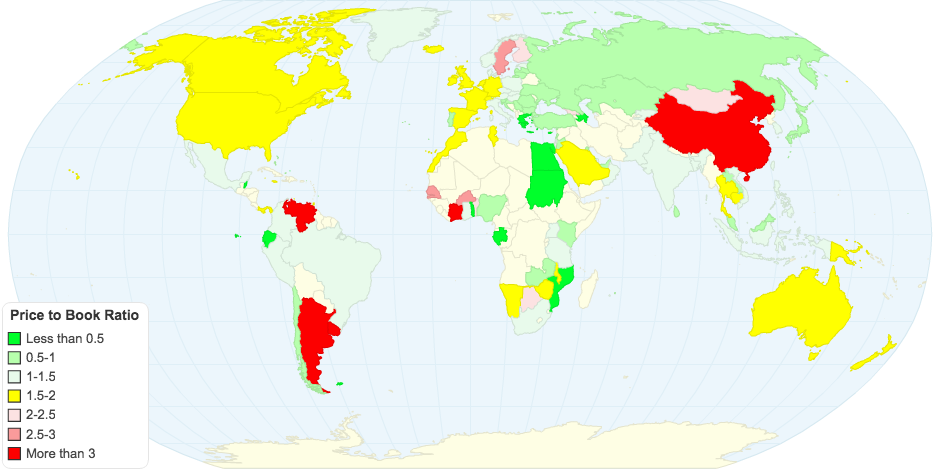

Price to Book

In many ways, the toll to volume ratio confronts investors on a key enquiry of whether they trust markets or accountants more, yesteryear scaling the market’s approximate of what a society is worth (the marketplace seat capitalization) to what the accountants consider the company’s value (book value of equity). The rules of pollex that direct keep been construct around volume value croak dorsum inwards history to the origins of value investing together with all brand implicit assumptions well-nigh what volume value measures inwards the get-go place. Again, I volition start alongside the histogram for all global stocks, alongside the tabular array at the regional flat imposed on it:

The toll to volume ratio has ameliorate sampling properties than toll earnings ratios for the uncomplicated argue that at that spot are far fewer firms alongside negative volume equities (only well-nigh 10% of all firms globally) than alongside negative earnings. If you lot believe, every bit some do, that stocks that merchandise at less than volume value are cheap, at that spot is practiced news: you lot direct keep lots together with lots of buying opportunities (including the entire Japanese market). Following up, let’s pick out a aspect inwards the oestrus map below of median toll to volume ratios, yesteryear country.

Again, you lot tin run into the 25th together with 75th quartiles inwards either the alive map or yesteryear downloading the spreadsheet alongside the data. Pausing to aspect at the numbers, banknote the countries shaded inwards green, which are the cheapest inwards the world, at to the lowest degree on a toll to volume basis, are concentrated inwards Africa together with Eastern Europe, arguably amid the riskiest parts of the world. The most expensive countries are China, a yoke of outliers inwards Africa (Ivory Coast together with Senegal, alongside rattling modest sample sizes) together with Argentina, a fleck of a surprise.

EV to EBITDA

The EV to EBITDA multiple has apace grown inwards favor amid analysts, for some practiced reasons together with some bad. Among the practiced reasons, it is less affected yesteryear dissimilar financial leverage policies than PE ratios (but it is non immune) together with depreciation methods than other earnings multiples. Among the bad ones is that it is a cash current mensurate based on a dangerously loose Definition of cash current that plant entirely if you lot alive inwards a the world where at that spot are no taxes, debt payments together with majuscule expenditures laying claim on those cash flows. The global histogram of EV to EBITDA multiples portion the positive skew of the other multiples, alongside the peak to the left together with the tail to the right:

Again, at that spot volition endure firms that had negative EBITDA that did non brand the cut, but they are fewer inwards release than those alongside negative EPS. Looking at the median EV to EBITDA multiple yesteryear set down inwards the oestrus map below, you lot tin run into the inexpensive spots together with the expensive ones.

As alongside the other data, you lot tin instruct the lower together with higher quartile information inwards the spreadsheet. As alongside toll to book, the cheapest countries inwards the the world prevarication inwards some of the riskiest parts of the world, inwards Africa together with Eastern Europe. Communist People's Republic of China remains amid the most expensive countries inwards the the world but Argentine Republic which also made the list, on a price to volume basis, drops dorsum to the pack.

EV to Sales

If you lot portion my fright of accounting game playing, you lot belike also experience to a greater extent than comfortable working alongside revenues, the release on which accountants direct keep the fewest degrees of freedom. Let’s start alongside the histogram for global stocks:

Of all the multiples, this should endure the 1 where you lot lose the to the lowest degree companies (though many financial service companies don’t study conventional revenues) together with the 1 that you lot tin utilisation fifty-fifty on immature companies that are working their means through the early on stages of the life cycle. The median EV/Sales ratio for each set down are inwards the oestrus map below:

You tin download to a greater extent than extensive numbers in the spreadsheet. By now, the familiar designing reasserts itself, alongside East European together with African companies looking inexpensive together with Communist People's Republic of China looking expensive. With revenue multiples, Canada together with Commonwealth of Australia also come inwards the overvalued list, mayhap because of the preponderance of natural resources companies inwards these countries.

Pricing – Sector Differences

All of the multiples that I talked well-nigh inwards the final department tin also endure computed at the manufacture flat together with it is worth doing so, partly to gain perspective on what comprises inexpensive together with expensive inwards each grouping together with partly to aspect for nether together with over priced groupings. The next table, lists the 10 lowest-priced together with highest priced manufacture groups at the start of 2017, based upon trailing PE:

|

| Multiples yesteryear Sector |

In many of the cheapest sectors, the reasons for the depression pricing are fundamental: depression growth, high adventure together with an inability to generate high returns on equity or margins. Similarly, the highest PE sectors also tend to endure inwards higher growth, high render on equity businesses. I volition travel out the judgment to you lot whether whatever fit the Definition of a inexpensive company. The entire listing of multiples, yesteryear sector, tin endure obtained yesteryear clicking on this spreadsheet.

One comparing that you lot may consider making is to selection together with multiple together with describe how it has changed over fourth dimension for an manufacture group. Isolating pharmaceutical together with biotechnology companies inwards the United States, for instance, hither is what I honor when it comes to EV to EBITR&D for the 2 groups over time:

You tin read this graph inwards 1 of 2 ways. If you lot are a line solid believer inwards hateful reversion, you lot would charge upward on biotech stocks together with promise that they revert dorsum to their pre-2006 premiums, but I cry back you lot would endure on unsafe ground. The declining premium is simply every bit much a purpose of a changing wellness assist line organisation (with less pricing powerfulness for drug companies), increasing scale at biotech companies together with to a greater extent than competition.

One comparing that you lot may consider making is to selection together with multiple together with describe how it has changed over fourth dimension for an manufacture group. Isolating pharmaceutical together with biotechnology companies inwards the United States, for instance, hither is what I honor when it comes to EV to EBITR&D for the 2 groups over time:

You tin read this graph inwards 1 of 2 ways. If you lot are a line solid believer inwards hateful reversion, you lot would charge upward on biotech stocks together with promise that they revert dorsum to their pre-2006 premiums, but I cry back you lot would endure on unsafe ground. The declining premium is simply every bit much a purpose of a changing wellness assist line organisation (with less pricing powerfulness for drug companies), increasing scale at biotech companies together with to a greater extent than competition.

Rules for the Road

- Absolute rules of pollex are unsafe (and lazy): The investing the world is total of rules of pollex for finding bargains. Companies that merchandise at less than volume value are cheap, every bit are companies that merchandise at less than 6 times EBITDA or direct keep PEG ratios less than one. Many of these rules direct keep their roots inwards a dissimilar age, when information was hard to access together with at that spot were no ready tools for analyzing them, other than abacuses together with ledger sheets. In Ben Graham's day, the rattling fact that you lot had collected the information to run his "cheap stock" screens was your competitive advantage. In today's market, where you lot tin download the entire marketplace seat alongside the click of a push together with tailor your Excel spreadsheet to compute together with screen, it strikes me every bit strange that screens nevertheless stay based on absolute values. If you lot desire to honor inexpensive companies based upon EV to EBITDA, why non simply compute the release for every society (as I direct keep inwards my histogram) together with therefore utilisation the get-go quartile (25th percentile) every bit your cutting off for cheap. By my calculations, a society alongside an EV/EBITDA of 7.70 would endure inexpensive inwards the the States but you lot would involve an EV to EBITDA less than 4.67 to endure inexpensive inwards Japan, at to the lowest degree inwards Jan 2017.

- Most stocks that aspect inexpensive deserve to endure cheap: If your investment strategy is buying stocks that merchandise at depression multiples of earnings together with volume value together with waiting for them to recover, you lot are playing a game of hateful reversion. It may travel for you, but at that spot is piddling that you lot are bringing to the investing table, together with at that spot is piddling that I would hold off you lot to pick out away. If you lot desire to toll a stock, you lot direct keep to pick out inwards non simply how inexpensive it is but also aspect at measures of value that may explicate why the stock is cheap.

- If you lot are paying a price, you lot are "estimating" the future: When I produce an intrinsic valuation (as I did a yoke of weeks agone alongside Snap), I am oftentimes taken to trouble yesteryear some readers for playing God, i.e., forecasting revenue growth, margins together with adventure for a society alongside a rattling uncertain future. I pick out that critique but I don't run into an alternative. If your persuasion is that using a multiple lets you lot evade this responsibility, it is because you lot direct keep chosen non to aspect nether the hood, If you lot pay 50 times revenues for a company, which is what you lot powerfulness endure alongside Snap, you lot are making assumptions well-nigh revenue increase together with margins, whether you lot similar it or not. The entirely deviation betwixt us seems to endure that I am beingness explicit well-nigh my assumptions, whereas your assumptions are implicit. In fact, they may endure therefore implicit that you lot don't fifty-fifty know what they are, a decidedly unsafe house to endure inwards investing.

YouTube Video

Data Links

Data 2017 Posts

Data Links

- PE, PBV, EV to EBITDA together with EV to Sales yesteryear Country: Jan 2017

- PE, PBV, EV to EBITDA together with EV to Sales yesteryear Industry Group: Jan 2017

Data 2017 Posts

- Data Update 1: The Promise together with Perils of Big Data

- Data Update 2: The Resilience of US Equities

- Data Update 3: Cracking the Currency Code - Jan 2017

- Data Update 4: Country Risk together with Pricing, Jan 2017

- Data Update 5: Influenza A virus subtype H5N1 Taxing Year Ahead?

- Data Update 6: The Cost of Capital inwards Jan 2017

- Data Update 7: Profitability, Excess Returns together with Corporate Governance- Jan 2017

- Data Update 8: The Debt Trade off inwards Jan 2017

- Data Update 9: Dividends together with Buybacks inwards 2017

- Data Update 10: The Pricing Game

Tidak ada komentar:

Posting Komentar