About a twelvemonth ago, I completed my kickoff update of a newspaper looking at all aspects of province risk, from political risk to default risk to equity risk, as well as wrote nigh my findings inwards iii posts, one on how to contain risk inwards companionship value, the minute on the pricing of province risk and the concluding ane on decoding currencies. The twelve months since take away hold been interesting, to state the least, as well as unsettling to many every bit markets were buffeted past times crises. In August 2015, a calendar month later my posts, nosotros had questions nigh China, its economic scheme as well as markets play out on the global arena, leading to this post with my Cathay story. Towards the halt of June 2016, nosotros had Britain voters choosing to leave of absence the EU, as well as that also caused waves (or at to the lowest degree ripples) through markets, which I talked about in this post. It is a skilful fourth dimension to update my global province risk database as well as the newspaper that goes amongst it, as well as inwards this post, I would similar to focus on updating numbers as well as providing risk pictures of the world, every bit it looks today.

Country Risk: Non-market measures

This should acquire without saying, but since at that topographic point is nonetheless resistance inwards some practitioner circles to this notion, I volition state it anyway. Some countries are riskier to invest in, either every bit an investor or every bit a business, than others. The risk differences tin sack last traced to a diversity of factors including where the province is inwards the life wheel (growing, stable or declining?), the maturity of its political institutions (democracy or dictatorship?, smoothness of political transitions), the province of its legal organization (in terms of both efficiency as well as fairness) as well as its exposure to violence. Not surprisingly, how you lot perceive risk differences volition depend inwards large business office on which dimension of risk you lot are looking at inwards a country.

While I await at risk measures that await at threat of violence, grade of corruption, dependence of the economic scheme on a commodity (or commodities) as well as protection of belongings rights individually inwards the amount paper, I also written report on a composite mensurate of risk that I obtain from Political Risk Services (PRS), a Europe-based service that measures province risk on a numerical scale, amongst lower (higher) numbers representing to a greater extent than (less) risk. The moving-picture demo provides a estrus map of the basis using this mensurate every bit of July 2016. (The estrus maps don't seem to demo upward on some browsers. So, I take away hold replaced them amongst snapshots. If you lot click on the links below the snapshots, you lot should last able to run across the estrus maps.. I think).

As nosotros motility from 2015 to 2016, it is interesting to run across how much risk changed inwards countries, rather than the flat of risk, as well as in ane lawsuit to a greater extent than using political risk score, the estrus map higher upward reports on changes inwards the PRS score over the concluding twelvemonth (if you lot hover over a country, you lot should run across it).

Finally, at that topographic point is an alternate as well as to a greater extent than widely used mensurate of province risk that focuses on province default risk, amongst sovereign ratings for countries from Moody's as well as Standard & Poors (among others) as well as the moving-picture demo below provides these ratings, every bit of July 1, 2016, globally:

I know that ratings agencies are much maligned later their failures during the 2008 crisis, but I produce mean value that some of the abuse that they accept is unwarranted. They oftentimes motility inwards tandem as well as are by as well as large dull to respond to large risk shifts, but I am glad that I take away hold their snapshots of risk at my disposal, when I produce valuation as well as corporate finance.

Country Risk: Market Measures

There are 2 problems amongst non-market measures similar risk scores or sovereign ratings. The kickoff is that they are neither intuitive nor standardized. Thus, a PRS score of fourscore does non brand a province twice every bit condom every bit ane amongst a PRS score of 40. In fact, at that topographic point are other services that mensurate province risk scores, where high numbers betoken high risk, reversing the PRS scoring. The minute is that these non-market measures are static. Much every bit risk measuring services as well as ratings agencies try, they cannot maintain upward amongst the stair of existent basis developments. Thus, spell markets reacted almost instantaneously to Brexit past times knocking downwards the value of the British Pound as well as scaling downwards stock prices around the globe, changes inwards risk scores as well as ratings happened (if at all) to a greater extent than slowly.

The kickoff marketplace mensurate of province risk that I would similar to introduce is ane that captures default risk changes inwards existent time, the sovereign credit default swap (CDS) market. The estrus map below captures sovereign CDS spreads globally, every bit of July 1, 2016:

Note that the map, if you lot scroll across countries, reports iii numbers: the CDS spread every bit of July1, 2016, a CDS spread cyberspace of the the United States of America CDS (of 0.41%) every bit of July 1, 2016 as well as the inwards the sovereign CDS spread over the concluding twelve months. Reflecting the market's capacity to conform quickly, the UK, for instance, saw a doubling inwards the marketplace assessment of default risk over the concluding year. The limitation is that sovereign CDS spreads are available for exclusively 64 countries, amongst to a greater extent than than one-half of the countries inwards the world, peculiarly inwards Africa, uncovered.

The minute marketplace mensurate of province risk is ane that I take away hold concocted that is based upon the default spread, but also incorporates the higher risk of equities, relative to authorities bonds, i.e., an equity risk premium (ERP) for each country. The procedure past times which I justice these equity risk premiums, which I construct on overstep of a premium that I justice every calendar month for the S&P 500 (and past times extension, role for all AAA ratted countries), is described to a greater extent than fully inwards this postal service from the start of the year. The updated ERPs for countries is captured inwards the estrus map below.

Note that every bit companies globalize, you lot request the entire map to justice the equity risk premium to value or analyze a multinational, since its risk does non come upward from where it is incorporated but where it does business.

Conclusion

I mean value that the agency nosotros mean value nigh as well as mensurate province risk is inwards its nativity as well as that nosotros request richer as well as to a greater extent than dynamic measures of that risk. I don't claim to take away hold all of the answers, or fifty-fifty most of the answers, but I volition drib dead on to larn from marketplace behaviour as well as brand my equity risk premiums to a greater extent than closely reflective of the risk inwards each country. I volition likely regret this resolution side past times side July, but I excogitation to brand my province risk premium an annual update, only every bit I take away hold my travel on equity risk premiums.

Charts update: The charts don't seem to last working on some browsers. They seem to travel on Safari.

I had a long post on province risk inwards July 2015, every bit purpose of serial of posts on the topic. At the fourth dimension of the post, the Chinese marketplace was inwards the midst of a meltdown, emerging markets were inwards turmoil as well as telephone commutation rates were on the move. It is vi months later, as well as nil seems to create got changed, but I intend that the inwardness lesson is worth reemphasizing. In a basis of multinational businesses as well as global investors, at that topographic point is no house to enshroud from province risk.

Country Risk Measurement

I volition non bore yous yesteryear repeating much of what I said inwards my before postal service on how I sentiment province risk inwards valuation, but it is built on 2 presumptions. First, a company's risk exposure is based on where it does business, non where it is incorporated or headquartered. Thus, Coca Cola as well as Nestle may live on incorporated inwards developed markets (US as well as Switzerland) but derive a meaning constituent of their revenues from emerging markets as well as are thus exposed to risk inwards those markets. By the same token, Embraer is a Brazilian companionship that derives a substantial constituent of its revenues inwards developed markets. Second, the risk of investing inwards equities varies across the world, resulting inwards higher equity risk premiums inwards some markets than others. To justice these risk premiums, I follow a four-step process:

As a minute step, I await upwardly the local currency sovereign rating for Republic of Republic of India from Moody's as well as larn inwards at a Baa3 rating; the typical default spread for a Baa3 rated province at the start of 2016 was 2.44%. I depository fiscal establishment check this justice against the sovereign CDS spread for India, which was 2.11% on Jan 1, 2016. I utilization the ratings-based spread of 2.44% every bit the default spread for India, though I would non heighten also much of a fight, if yous insisted on using the CDS spread.

In the 3rd step, I attempt out to justice how much riskier equities are than authorities bonds inwards emerging markets yesteryear using proxies for each one: the S&P Emerging BMI Index (an index of emerging marketplace equities) for stocks, as well as the S&P Emerging Market Public (government as well as quasi government) bond index yield. The criterion divergence inwards the old is 17.36% as well as the coefficient of variation inwards the latter is 12.91% as well as the ratio of the old to the latter is 1.34. Multiplying this ratio yesteryear the default spread inwards pace 2 yields a province risk premium for Republic of Republic of India of 3.28%. (CRP for Republic of Republic of India = 2.44% * 1.34 = 3.28%)

In the 4th step, I add together the province risk premium to the implied premium of 6% that I estimated inwards pace 1 to larn inwards at an equity risk premium for Republic of Republic of India of 9.28%.

Is this release an estimate? Of course! Would yous larn a dissimilar release if yous used the CDS spread every bit your mensurate of default risk as well as dissimilar indices for emerging marketplace equities as well as bonds? The response is yes. It is for this argue that the spreadsheet that I create for equity risk premiums allows yous to supersede my defaults amongst yours for whatsoever or all of these variables. Before yous exhaust yourself inwards this effort, I would advise that pocket-sized differences inwards this release volition non brand or suspension your valuation. So, brand your best estimates as well as motion on!

Country Risk Update - Jan 2016

Using the approach described for India, I compute equity risk premiums for the 130 countries amongst a Moody's sovereign rating. For most 14 more, amongst no Moody's rating for the country, I was able to honor a sovereign rating on S&P that I convert to a Moody's rating as well as justice an ERP. Finally, at that topographic point are most twenty countries, loosely categorized every bit frontier markets, for which at that topographic point is no rating or CDS spread; these include the hot spots of the basis such every bit Syrian Arab Republic as well as Iraq. For these, I utilization the entirely mensurate of province risk that I tin shipping away find, a composite risk score from Political Risk Services (PRS) as well as utilization that score to compute an equity risk premium; I create a await upwardly tabular array using the countries that create got both PRS scores as well as ERP to brand these judgments. Desperation move? Perhaps, but if yous tin shipping away honor a meliorate means of doing it, I would live on glad to follow your lead. The resulting equity risk premiums yesteryear province are available inwards the spreadsheet that I referenced before but are also inwards the map below (which adds nil inwards terms of content but looks much better):

In my July 2016 updates, I also included one on how stocks are priced approximately the world, using multiples (PE, PBV, EV/Sales, EV/EBITDA, EV/Invested Capital). While that postal service has a to a greater extent than extensive explanation of why stocks should merchandise at dissimilar multiples approximately the world, I create got updated the multiples, yesteryear country, inwards this spreadsheet. As yous peruse these numbers, operate out along inwards heed that the release of companies that I create got inwards information gear upwardly is really pocket-sized for some countries as well as the multiples tin shipping away so yield foreign values. To forestall outliers from hijacking my estimation, I also compute the multiple using aggregated values; thus, the PE ratio for PRC is computed yesteryear adding the marketplace capitalizations of all companies listed inwards the marketplace as well as dividing yesteryear the aggregated internet income of these companies.

Much every bit I would similar to read to a greater extent than into this film (especially most inexpensive as well as expensive markets), these province numbers are to a greater extent than a commencement pace inwards the investment procedure than a terminal one.

Bottom line

I intend that nosotros are far also casual inwards our handling of province risk, estimating equity risk premiums on motorcar airplane pilot for countries as well as attaching these premiums to companies based on where they are incorporated, rather than where they create business. If at that topographic point is a lesson from the terminal week's implosion inwards the Chinese market, it is that the emerging marketplace increment floor that as well as so many developed marketplace companies create got pushed for the terminal 2 decades has a nighttime side, as well as that nighttime side takes the cast of higher risk. It is slowly to forget this intuitive concept inwards the skillful times, but the marketplace lulls us into complacency before shocking us.

The inexorable force towards globalization has stalled inward the final few years, but the alter it has created is irreversible. The largest companies inward the globe are multinationals, deriving large portions of their revenues from exterior domestic markets, together with fifty-fifty the most inward looking investors are subject upon global economies for their returns. As a consequence, measure together with incorporating terra firma adventure into determination making is a requirement inward both corporate finance together with valuation. It is inward pursuit of that objective that I revisit the terra firma adventure number twice every year, i time at the start of the twelvemonth together with i time mid-year, at which fourth dimension I also update a newspaper that I have got on the topic, that you lot are welcome to read or browse or ignore.

The Globalization of Companies

There are some investors, peculiarly inward the United States, who experience that they tin avoid dealing amongst adventure inward other countries, past times investing inward simply US stocks. That is a delusion, though, because a companionship that is incorporated together with traded inward the U.S.A. of America tin derive a meaning portion of its revenues together with earnings from exterior the country. In 2015, the companies inward the S&P 500, the largest marketplace cap stocks inward the US, derived about 44% of its revenues from unusual markets, downwardly from 48% inward the prior year.

Source: S&P

The composition of unusual sales is also changing, though gradually, over time, shifting away from the United Kingdom of Great Britain together with Northern Ireland of Britain together with Northern Republic of Ireland together with Europe to emerging markets, equally evidenced inward the graph below:

Source: S&P

Lest you lot experience that this graph is skewed past times the biggest companies inward the index, 239 of the 500 companies inward the index reported that unusual sales represented betwixt 15% together with 85% of their total sales together with xiii companies reported that to a greater extent than than 85% of their sales came from exterior the US. In 2014, 2 companies, Accenture together with Seagate Technology, reported that all their sales were foreign, making them US companies exclusively inward name. (Many of you lot have got pointed out that Accenture has meaning US sales together with that is true. I am just excerpting from the S&P report, which should atomic number 82 you lot to enquiry how S&P classifies unusual sales.) This phenomenon is non restricted to US companies, equally the largest companies inward most markets exhibit similar characteristics. While nosotros tin struggle whether these tendency lines are skillful or bad for consumers together with investors, the consequences are real:

Fraying link to domestic economies: For decades, the conventional wisdom has been that the stock marketplace inward a terra firma is closely tied to how good the economic scheme of that terra firma is doing. That human relationship has been weakened past times globalization together with equity marketplace performance around the globe is disconnecting from domestic economical growth. Taking the US equally an example, consider that equity markets inward the US have got been on a bull run, amongst indices upwardly 170% to 200%, cumulatively since 2009, fifty-fifty equally the US economic scheme has been posting anemic growth.

Central Banking might is diluted: In the decades since the cracking depression, nosotros have got to come upwardly to take away that key banks tin usage the policy levers that they have got at their disposal to motility long term involvement rates together with to strongly influence overall economical growth, but that might besides has been reduced past times globalization together with its unpredictable flows. It should come upwardly equally no surprise together with then that the frantic efforts of key banks\ inward the US, Europe together with Japan, inward the final decade, to usage the involvement charge per unit of measurement lever to heart upwardly economical increment or to alter the trajectory of long term involvement rates have got failed.

Taxing questions: When writing taxation code, governments have got to a greater extent than ofttimes than non assumed that companies incorporated inward their domiciles have got piffling selection but to accede to taxation laws eventually together with pay their percentage of taxes. While companies have got historically played the taxation game past times delaying together with deferring taxes due, their global attain immediately seems to have got shifted the residue of might inward their direction. In the United States, inward particular, where the authorities has tried to taxation companies on their global income, this force dorsum has taken the shape of trapped cash, equally companies concord trillions of dollars of cash on unusual shores, together with inversions, where some US companies have got chosen to motility their domicile base of operations to to a greater extent than favorable taxation locales.

Declining cross-market correlations: As companies globalize, it should come upwardly equally no surprise that the correlations across global equity markets have got climbed, amongst 2 immediate consequences. The offset is that global crises are immediately an around annual occurrence rather than uncommon surprises, equally hurting inward i marketplace rapidly spreads across the world. The minute is that the salvage of geographic diversification, long touted equally protection against domestic marketplace shocks, provides far less protection than it used to.

The bottom line is that at that spot is no house to cover from terra firma risk, together with equally amongst whatever other type of risk, it is best to human face to it together with bargain amongst it explicitly.

Country Risk - Default Risk Measures

The simplest together with most easily measured terra firma adventure is the adventure of sovereign default. When countries default on their obligations, it is non simply the authorities that feels the hurting but companies, consumers together with investors do, equally well.

Sovereign Default: Frequency together with Consequences

Governments borrow money, both from their ain citizens together with from unusual entities, together with they sometimes borrow besides much. Some of these authorities default, non exclusively on their unusual currency debt but also on their local currency debt, amongst the latter having popular off to a greater extent than mutual over time:

Source: Fitch Ratings

You may live puzzled past times local currency debt defaults, since governments practice have got the capacity to impress to a greater extent than of their ain currency, but faced amongst a selection betwixt defaulting or debasing their currencies, many governments select the latter. When default occurs, the immediate hurting is felt past times the authorities together with lenders, the quondam because it loses the capacity to borrow more, together with the latter because they don't larn paid., but at that spot is collateral damage:

Capital Market Turmoil: Liquidity dries up, equally investors withdraw from equity together with bond markets, making it to a greater extent than hard for private enterprises inward the defaulting terra firma to enhance funds for projects together with resulting inward sudden cost drops inward both bond together with stock markets.

Real growth: Sovereign defaults are to a greater extent than ofttimes than non followed past times economical recessions, equally consumers concord dorsum on spending together with firms are reluctant to commit resources to long-term investments.

Political Instability: Default tin also strike a blow to the national psyche, which inward plough tin seat the leadership grade at risk. The moving ridge of defaults that swept through Europe inward the 1930s, amongst Germany, Austria, Republic of Hungary together with Italia all falling victims, allowed for the ascent of the Nazis together with set the phase for the Second World War. In Latin America, defaults together with coups have got gone manus inward manus for much of the final 2 centuries.

Sovereign Ratings

The most accessible measures of sovereign default adventure are sovereign ratings, amongst ratings together with default spreads are highly correlated. On the minus side, ratings agencies seem to have got regional biases (under rating emerging markets together with over rating developed markets) together with are irksome to alter ratings.

Sovereign CDS Spreads

In the final decade, nosotros have got seen the increment of a market-based stair out of default adventure inward the Credit Default Swap (CDS) market, where you lot tin purchase insurance against sovereign default past times buying a sovereign CDS. Since the insurance is priced on annual basis, the cost of a sovereign CDS becomes a marketplace stair out of the default spread for that country. In July 2017, at that spot were 68 countries amongst sovereign CDS together with the painting demo below captures the pricing (with the information available for download at this link). One of the limitations of the CDS marketplace is that at that spot is even so credit adventure inward the marketplace together with to allow for the upward bias this creates inward the spreads, I compute a netted version of the spread, where I internet out the US sovereign CDS spread of 0.34% from each country's CDS spread.

To render a comparing betwixt the CDS together with sovereign rating measures of default risk, permit me offering 2 example. The sovereign CDS for Brazil on July 1, 2017, was 3.46%. On the same day, Moody rated Brazil at Ba2, amongst an estimated default spread of 3.17%, closed to the CDS value. For India, the sovereign CDS spread on July 1, 2017, was 2.42%, really closed to the default spread of 2.32% that would have got been assigned to it based upon its Baa3 rating.

Country Risk - Institutional Risk

When investing inward a company, the sovereign default adventure is simply i of many risks that you lot have got to element into your determination making. In fact, default adventure may pale inward comparing to risks you lot human face because of the institutional structure, or lack of it, inward a country. At the adventure of picking at scabs, hither is my shot at assessing some of these risks.

1. Corruption

Much equally nosotros similar to inveigh against its consequences, corruption is non simply component together with bundle of operating inward some parts of the world, but it takes on the piece of work of an implicit tax, i that is paid to gratuitous agents, acting inward their ain interests, rather than to governments. Transparency International, an entity that measures corruption adventure around the world, estimates corruption scores for private countries together with heir findings for 2016 are summarized inward the painting demo below. To encounter where a terra firma falls on the corruption continuum, you lot tin either click on the alive link below the painting demo or download the information past times terra firma past times clicking here.

While it is tardily to autumn dorsum on cultural stereotypes to explicate differences across countries, at that spot is a high correlation betwixt economical good beingness together with corruption. Thus, spell much of Latin America scores depression on the corruption, Republic of Chile together with Uruguay rank much higher, equally practice Republic of Korea together with Nihon inward Asia.

2. Legal Protections

Even the really best investments are exclusively equally skillful equally the legal protections that you lot have got equally an investor, against expropriation or theft, which is why the belongings correct protections rank high on investor want lists. To stair out the forcefulness of belongings rights, I turned to the International Property Rights Index (IPRI), together with study the scores they assigned inward their most recent update inward 2016, to countries inward the painting demo below. You tin click on the live link below the painting demo or download the information here.

Europe, North America, Nihon together with Commonwealth of Australia all score high on belongings rights, but the hopeful sign is that index itself has seen increasing honor for belongings rights across fourth dimension together with Venezuela together with Myanmar are immediately to a greater extent than the exception, than the rule.

3. Risk of violence

It is hard to practice business, when you lot have got bullets whizzing past times together with bombs going off around you. Holding all else constant, you lot would prefer to operate inward parts of the globe that are safer rather than riskier. To stair out exposure to violence, I i time to a greater extent than plough to an external entity, Vision of Humanity, together with reproduce their Global Peace Index inward the painting demo below (with link to live map together with to data):

In keeping amongst the adage that when it rains, it pours, the countries that are most susceptible to corruption together with have got weak belongings rights also seem to live most exposed to physical violence.

Country Risk - Equity Risk

As you lot tin see, at that spot are multiple dimensions on which you lot tin stair out terra firma risk, leading to dissimilar scores together with rankings. As an investor inward the country, you lot are exposed to all of these risks, albeit to varying degrees, together with you lot have got to consider all these risks inward making decisions. Consequently, you lot would similar (a) a composite stair out of adventure that (b) you lot tin convert into a metric that easily fits into your investment framework.

1. Country Risk Scores

There are several services that render composite measures of terra firma risk, including the Economist, Euromoney together with Political Risk Services (PRS). These terra firma adventure measures take away the shape of numerical scores, together with inward the estrus map below, I study the alter inward the PRS terra firma adventure score betwixt July 2016 together with July 2017 together with categorize countries based on the administration together with magnitude of the change. Here, equally inward the prior pictures, you lot tin encounter the PRS scores together with the change, past times country, past times either clicking on the live map link below the painting demo or download the information past times clicking here).

Based on the PRS scores, the vast bulk of emerging markets became safer during the fourth dimension catamenia betwixt July 2016 together with July 2017, amongst the biggest improvements inward Latin America together with Asia. The North American countries saw adventure popular off up, equally did pockets of Africa together with South East Asia. The work amongst terra firma adventure scores, no affair how good they are measured, is that they practice non lucifer a standardized framework. Just to render an illustration, PRS scores are depression for risky countries together with high for rubber countries, whereas the Economist adventure scores are high for risky countries together with depression for rubber countries.

3. Equity Risk Premiums

To contain together with adapt for terra firma adventure into investing together with valuation, I attempt to guess the equity adventure premiums for country, amongst riskier countries having higher equity adventure premiums. I start amongst the implied equity adventure premium for the US, which I guess to live 5.13% at the start of July 2017 equally my mature marketplace premium together with add together to it a scaled upwardly version of the default spread (based upon the rating); the scaling element of 1.15 is based upon the relative volatility of emerging marketplace equities versus bonds. You tin encounter a to a greater extent than detailed description of the procedure inward the newspaper that is linked at the goal of this post. You tin expression upwardly the equity adventure premium for an private terra firma past times clicking on the live map link or download the information past times clicking here.

These equity adventure premiums are key to how I bargain amongst terra firma adventure inward valuation, equally I volition explicate inward the final department of this post.

Closing the Loop

When valuing companies that have got substantial exposure to terra firma risk, it is tardily to larn overwhelmed past times the multifariousness of risks. To popular off on the procedure nether your control, you lot should start past times breaking terra firma adventure into 3 buckets: adventure that is specific simply to that country, adventure that is macro/global together with discrete risks that are potentially catastrophic (such equally nationalization or terrorism). Each has a house inward valuation, amongst terra firma specific risks incorporated into expected cash flows, macro economical risks inward the discount charge per unit of measurement together with discrete risks inward a post-valuation adjustment.

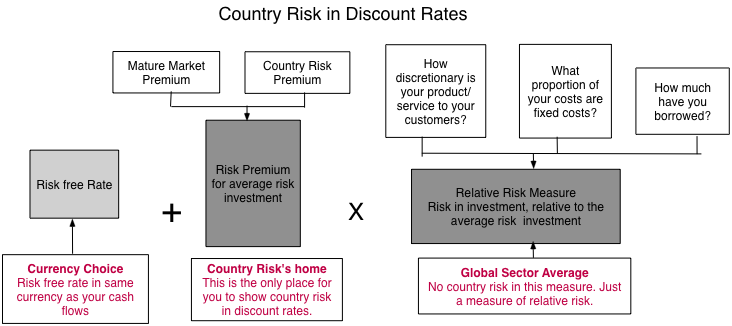

1. Adjusting discount rates

The key to a prepare clean terra firma adventure adjustment, when estimating discount rates, is to brand certainly that you lot practice non double or fifty-fifty triple count it. With the cost of equity for a company, for instance, where at that spot are exclusively 3 inputs that drive the cost, it is exclusively the equity adventure premium that should live conduit for terra firma adventure (hence explaining my before focus on equity adventure premiums, past times country). The adventure gratuitous charge per unit of measurement is a business office of the currency that you lot select to practice your valuation inward together with the relative adventure stair out (or beta, if that is how you lot select to stair out it) should live determined past times the work concern or businesses that the companionship operates in.

If you lot are discounting the composite cash flows of a multinational company, the equity adventure premium should live a weighted average of the equity adventure premiums of the countries that the companionship operates in, amongst the weights based on revenues or operating assets. If you lot are valuing simply the operations inward i country, you lot would usage the equity adventure premium simply for that country.

2. Expected cash flows

With risks that are specific to a country, it is ameliorate to contain the risks into the expected cash flows. Thus, if a terra firma is rife amongst corruption, you lot could process the resulting costs equally component of operating expenses, reducing profits together with cash flows. When legal together with regulatory delays are a characteristic of work concern inward a country, you lot tin prepare inward the delay equally lags betwixt investing together with operations. When violence (from terrorism or war) is component together with bundle of operations, you lot may desire to include a cost of insuring against the adventure inward your cash flows.

None of these adjustments are tardily to make, but it is worth remembering that incorporating the adventure into your cash flows is non adventure adjusting the cash flow, since the latter requires replacing the expected cash stream amongst a certainty equivalent one. Where does currency adventure play out? When converting cash flows from i currency (foreign) to some other (domestic), you lot should take away inward expected devaluation or revaluation into expected central rates. If you lot desire to hedge central charge per unit of measurement risk, you lot tin contain the cost of heeding into your cash flows but it is non clear that you lot should live adjusting discount rates for that risk, since investors tin diversify it away.

3. Post-Valuation Adjustment

There are some risks that are rare, but if they occur, tin live devastating, at to the lowest degree for investors inward a business. Included inward this grouping would live the adventure of nationalization together with terrorism. These risks cannot live incorporated easily into discount rates together with adjusting expected cash flows inward a going concern valuation (DCF) for adventure that a companionship volition live nationalized or volition non live is messy.

Thus, to guess the effect that nationalization adventure volition have got on the value of a business, you lot volition have got to assess the probability that the work concern volition live nationalized together with the value that you lot volition have equally owners of the business, inward the lawsuit of nationalization.

Danger together with Opportunity

One of my favorite definitions of adventure is the Chinese symbol for crisis, a combination of the symbols for danger together with opportunity.

危機

With risky emerging markets, this comes into , I am reminded that to have got i (opportunity), I have got to live willing to alive the other (danger). Blindly ignoring these markets, equally some conservative developed marketplace companies are inclined to do, because at that spot is danger volition atomic number 82 to stagnation, but blindly jumping into them, drawn past times opportunity, volition crusade implosions. The essence of adventure administration is to stair out the danger inward markets together with and then gauge whether the opportunities are sufficient to compensate you lot for the dangers. That is what I promise that I have got set the foundations for, inward this post.

In my in conclusion 8 posts, I looked at aspects of corporate deportment from investments to financing to dividend policy, using the information that I collected at the get of 2019, to examine what companies percentage inward common, in addition to what makes them different. In summary, I works life that the ascent inward lead chances premiums inward both equity in addition to bond markets inward 2018 receive got pushed upwards costs of equity in addition to capital, that companies across the globe are finding it hard to generate returns on their investments that top their costs of funding, in addition to that many of them, specially inward mature businesses, are returning to a greater extent than cash, much of it inward the cast of buybacks. Since all of the companies inward my information laid are publicly traded, at that topographic point is ane in conclusion let on that I receive got non addressed straight inward my posts then far, in addition to that is the marketplace seat pricing of these companies. In this post, I complete my information update series, past times looking at how pricing varies across companies, sectors in addition to geographies, in addition to what lessons investors tin draw from the data.

Value versus Price: The Difference

I receive got posted many times on the betwixt the value of an property in addition to its' pricing, but I don't intend it hurts to revisit that difference. The determinants of value are simple, although non ever piece of cake to estimate. Whether you lot are valuing start-up businesses, emerging marketplace seat firms, or commodity companies, the values are driven past times expected cash flows, growth, in addition to risk. Although a discounted cash menses valuation is frequently the tool that nosotros used to give cast to these fundamentals, inward the cast of cash flows, increase rates inward these cash flows, in addition to discount rates, it is non the only pathway to intrinsic value. The determinants of toll are demand in addition to supply, in addition to acre fundamentals do behave upon both, mood in addition to momentum are also rigid forces inward pricing. These “animal spirits,” equally behavioral economists mightiness tag them, tin non only drive toll to diverge from value, but also require different tools to last used to assess the right pricing for an asset. With many assets in addition to businesses, pricing an property commonly involves standardizing a toll (a multiple), finding similar or comparable assets that are already priced inward the marketplace, in addition to controlling for differences. The movie below, which I receive got used many times before, captures the ii processes:

The ground that I reuse this movie then much is because, to me, it is an all-encompassing snapshot of every conceivable investment philosophy that exists inward the market:

Efficient Marketers: If you lot believe that markets are efficient, the ii processes volition generate the same number, in addition to whatever gap that exists volition last purely random in addition to chop-chop closed.

Investors: If you lot are an investor, whether value or growth, in addition to you lot genuinely hateful it, your persuasion is that the pricing process, for ane ground or the other, tin deliver a toll different from your gauge of value in addition to that the gap that exists volition close, equally the toll converges to value. The deviation betwixt value in addition to increase investors lies inward where you lot intend markets are most probable to brand mistakes (in valuing existing assets or increase opportunities) in addition to right them. In essence, you lot are equally much a believer inward efficient markets equally the outset group, amongst the only deviation beingness that you lot believe markets dice efficient afterward you lot receive got taken your seat on a stock.

Traders: If you lot are a trader, you lot get off amongst either the presumption that at that topographic point is no such matter equally intrinsic value, or that it exists, but that no ane tin gauge it. You play the pricing game, effectively using your skills at gauging momentum in addition to forecasting the effects of corporate tidings on prices, to purchase at a depression toll in addition to sell at a high price.

Market participants are most exposed to danger when they are delusional most the game that they are playing. Many portfolio managers, for instance, claim to last investors, playing the value game, acre using pricing screens (PE in addition to growth, PBV in addition to ROE) in addition to adding to their holdings of momentum stocks. Many traders seem to intend that they volition last viewed equally deeper in addition to to a greater extent than accomplished if they speak the value talk, acre using charts in addition to technical indicators inward the closet, to brand their stock picks.

The Pricing Process

The essence of pricing is attaching a let on to an property or company, based upon how similar assets in addition to companies are beingness priced inward the market. To acquire insight into how to toll an asset, a concern or a company, you lot should intermission downwards the pricing procedure into steps:

You may last a lilliputian puzzled past times the outset pace inward the process, where I standardize the price, but the ground is simple. You cannot compare toll per percentage across companies, since it is a business office of the percentage count, which tin last changed overnight inward a stock split. To standardize prices, you lot scale them to some variable that all of the assets inward the peer grouping share. With existent estate properties, you lot separate the toll of each holding past times its foursquare footage to brand it at a price/square human foot that tin last compared across properties. With businesses, you lot scale pricing to an operating variable, amongst profits beingness the most obvious choice, but it tin last revenues, cash flows or majority value. Note that whatever multiple that you lot uncovering on a stock or society is embedded inward this definition, ranging from PE ratios to EV/EBITDA multiples to revenue multiples, in addition to fifty-fifty beyond, to marketplace seat toll per subscriber or user. The 2nd pace inward the process, i.e., finding similar assets in addition to companies, should brand clear the fact that this is a procedure that requires subjective judgments in addition to is opened upwards to bias, precisely equally is the illustration inward intrinsic valuation. If you lot are pricing Nvidia, for instance, you lot create upwards one's heed how narrowly or broadly you lot define the peer group, in addition to which companies to deem to last "similar". The tertiary pace int he procedure requires controlling for differences across companies. Put simply, if the society that you lot are pricing has higher increase or lower lead chances or meliorate returns on its investments on it projects that the companies inward the peer group, you lot receive got to arrange the pricing to reverberate it, either subjectively, equally many analysts do, amongst story telling, or objectively, past times bringing inward key variables into the estimation process.

Pricing the Markets inward Jan 2019

Rather than taking you lot through multiple afterward multiple, in addition to overwhelming amongst pictures in addition to tables on each one, I volition listing out what I learned past times looking at the pricing of all publicly traded stocks around the world, inward early on 2019, inward a serial of pricing propositions.

Paraphrasing Einstein, everything is relative, if you lot are pricing companies. Is a PE ratio of 5 low? Not if one-half the stocks inward the marketplace seat merchandise at less than five. Is an EV/EBITDA of 40 high? Perhaps inward some sectors, but non if you lot are comparing high increase companies inward a highly priced sector. Old fourth dimension value investing is filled amongst rules of thumb, in addition to many of these rules are devised around absolute values for PE or PEG ratios or Price to Book, at odds amongst the real notion of pricing. If you lot desire to brand pricing statements most what comprises inexpensive or expensive, you lot should last looking at the distribution of the multiple across the market. Thus, to cast pricing rules on US stocks at the get of 2019, I looked the distribution of current, forrard in addition to trailing PE ratios for US stocks on Jan 1, 2019:

At the get of 2019, a depression trailing PE ratio for a US stock would receive got been 6.09, if you lot used the lowest decile or 10.36, if you lot moved to the outset quartile, in addition to a high PE ratio, using the same approach, would receive got been 27.31, amongst the tertiary quartile, or 53.70, amongst the top decile. Lest I last defendant of picking on value investors, they are non the only or fifty-fifty the biggest culprits, when it comes to absolute rules. Private equity investors in addition to LBO initiators receive got built their ain laid of screens. I receive got lost count of the let on of times I receive got heard it said that an EV to EBITDA less than half dozen (or 5 or seven) must hateful that a society is non precisely cheap, but a skillful candidate for leverage, but is that true? To answer the question, I looked at the EV to EBITDA multiples across companies, across regions of the world.

If you lot wield a pricing bludgeon in addition to declare all companies that merchandise at less than half dozen times EBITDA to last cheap, you lot volition uncovering most one-half of all stocks inward Russian Federation to last bargains. Even globally, you lot should hav no problem finding investments to brand amongst this rule, since almost ane quarter of all companies merchandise at less than half dozen times EBITDA. My indicate is non that that you lot cannot receive got rules of thumb, since they do be for a reason, but that those rules, inward a pricing world, receive got to last scaled to the data. Thus, if you lot desire to define the outset decile equally your mensurate of what comprises cheap, why non brand it the outset decile? That would hateful that an EV to EBITDA multiple less than 5.16 would last inexpensive inward the US on Jan 1, 2019, but that let on would receive got to recalibrated equally the marketplace seat moves upwards or down.

Pricing Proposition 2: Markets receive got a cracking deal inward common, when it comes to pricing, but the differences tin last revealing!

Much is made most the differences across global equity markets, in addition to specially most the separate betwixt emerging in addition to developed marketplace seat companies, when it comes to pricing, amongst delusions running deep on both sides. Emerging marketplace seat analysts are convinced that stocks are priced real differently, in addition to frequently to a greater extent than irrationally, inward their local markets, leaving them gratis to devise their ain rules for their markets. Conversely, developed marketplace seat analysts frequently convey perspectives most what comprises high, depression or average pricing ratios, built upwards through decades of exposure to US in addition to European markets, to emerging markets in addition to uncovering them puzzling. The information tells a different story, amongst pricing ratios around the basis having distributional characteristics that are surprisingly similar across different parts of the world:

While the levels of PE ratios vary across regions, amongst Chinese stocks having the highest median PE ratios (20.63) in addition to Russian in addition to East European stocks the lowest (9.40), they all receive got the same asymmetric look, amongst a peak to the left (since PE ratios cannot last lower than zero) in addition to a tail to the right (there is no cap on PE ratios). That asymmetry, which is shared past times all pricing multiples, is the ground that you lot should ever last cautious most whatever pricing declaration that is built on comparisons to the average PE or PBV, since those numbers volition last skewed upwards because of the asymmetry. While it is truthful that markets percentage mutual characteristics, when it comes to pricing, the differences inward levels are also worth paying attending to, when investing. Influenza A virus subtype H5N1 global fund managing director who ignores these differences, in addition to picks stocks based upon PE ratios alone, volition terminate upwards amongst a portfolio that is dominated past times African, Midde East in addition to Russian stocks, non a recipe for investing success.

Pricing Proposition 3: Book value is the most overrated metric inward investing

I receive got never understood the reverence that some investors seem to concur for majority value, equally revealed inward the let on of investing adages built around it. Stocks that merchandise at less than majority value are considered cheap, in addition to companies that construct upwards majority value are considered to last value creating. At the root of the "book value" focus are ii assumptions, sometimes stated but frequently implicit. The outset is that the majority value is a mensurate of liquidation value, an gauge of what investors would acquire if they closed downwards the society today in addition to sold its assets. The 2nd is that accountants are consistent in addition to conservative inward estimating property value, dissimilar markets, which are prone to mood swings. Both assumptions are built on foundations of sand, since majority value is non a skillful mensurate of liquidation value inward most sectors, in addition to accountants are both inconsistent in addition to slow-moving, when it comes to estimating in addition to adjusting majority value. Again, to acquire perspective, let's aspect at the toll to majority ratios around the world, at the get of 2019:

If you lot believe that stocks that merchandise at less than majority value are cheap, you lot volition ane time again uncovering lots of bargains inward the Middle East, Africa in addition to Russia, but fifty-fifty inward markets similar the United States, where less than a quarter of all companies merchandise at less than majority value, they tend to last clustered inward industries that are inward upper-case missive of the alphabet intensive (at to the lowest degree equally defined past times accountants) in addition to declining businesses.

Note that amidst the US industries amongst the fewest stocks that merchandise at less than majority value are a large let on of technology in addition to consumer production companies, amongst utilities in addition to basic chemicals beingness the only surprises. On the listing of US manufacture groups amongst the highest per centum of stocks that merchandise at less than majority value are crude oil companies (at different stages of the business), one-time fourth dimension manufacturing companies in addition to life insurance. If you lot pick your stocks based upon depression toll to book, inward Jan 2019, your portfolio volition last weighted amongst companies inward the latter group, a prospect that should concern you.

Pricing Proposition 4: Most stocks that aspect inexpensive deserve to last cheap!

There are traders who receive got lilliputian fourth dimension for fundamentals, argument that they receive got lilliputian or no job to play inward twenty-four hours to twenty-four hours movements of stock prices. That is in all likelihood true, but fundamentals do receive got pregnant explanatory power, when it comes to why some companies merchandise at depression multiples of profits or majority value in addition to others are high multiples. To empathize the link, I uncovering it most useful to dice dorsum to a elementary intrinsic value model, in addition to amongst elementary algebraic manipulation, brand it a model for a pricing multiple. The movie below shows the paths you lot would accept amongst an equity multiple (Price to Book) in addition to an enterprise value (EV/Sales) to brand it at their determinants:

Now what? If you lot purchase into the intrinsic persuasion of a toll to majority ratio, it should last higher for firms that earn high returns on equity, receive got higher increase in addition to lower risk, in addition to lower for firms that earn depression returns on equity, receive got lower increase in addition to higher risk. Does the marketplace seat toll inward fundamentals? For the most part, the answer is yes, equally you lot tin come across fifty-fifty inward the tables that I receive got provided inward this post service then far. Russian stocks receive got the lowest PE ratios, but that reflects the corporate governance concerns in addition to province lead chances that investors receive got when investing inward them. Chinese stocks inward contrast receive got the highest PE ratios, because fifty-fifty amongst stepped downwards increase prospects for the country, they receive got higher expected increase than most developed marketplace seat companies. Looking at stocks amongst the lowest toll to majority ratios, Middle Eastern stocks receive got a disproportionate representation because they earn depression returns on equity in addition to the manufacture groupings amongst the lowest toll to majority (oil manufacture groups, steel etc.) also percentage that feature. Pricing, done right, is thence a search for mismatches, i.e., companies that aspect inexpensive on a pricing multiple without an obvious key that explains it. This tabular array captures some of the mismatches:

Multiple

Key Driver

Valuation Mismatch

PE ratio

Expected growth

Low PE stock amongst high expected increase charge per unit of measurement inward profits per share

Low EV/capital stock amongst high render on capital

EV/sales

After-tax operating margin

Low EV/sales ratio amongst a high after-tax operating margin

Pricing Proposition 5: In pricing, it is non most what "should be" priced in, but "what is" priced in!

In the in conclusion proposition, I argued that markets for the most portion are sensible, pricing inward fundamentals when pricing stocks, but at that topographic point volition last exceptions, in addition to sometimes large ones, where entire sectors are priced on variables that receive got lilliputian to do amongst fundamentals, at to the lowest degree on the surface. This is specially truthful if the companies inward a sector are early on inward their life cycles in addition to receive got lilliputian to present inward revenues, real lilliputian (or fifty-fifty negative) majority value in addition to are losing coin on every profits measure. Desperation drives investors to aspect for other variables to explicate prices, resulting inward companies beingness priced based upon website visitors (at the peak of the point com boom), numbers of users (at the get of the social media craze) in addition to numbers of subscribers.

I noted this phenomenon, when I priced Twitter ahead of its IPO inward 2013, in addition to argued that to toll Twitter, you lot should aspect at its user base of operations (about 240 ane one one thousand thousand at the time) in addition to what markets were paying per user at the fourth dimension (about $130) to brand it at a pricing of $24 billion, good to a higher house my gauge of intrinsic value of $11 billion for the society at a time, but much closer to the actual pricing, right afterward the IPO. It is thence neither surprising nor newsworthy that venture capitalists in addition to equity enquiry analysts are to a greater extent than focused on these pricing metrics, when assessing how much to pay for stocks, in addition to companies, knowing this, play along, past times emphasizing them inward their profits reports in addition to tidings releases.

Conclusion

I do believe inward intrinsic value, in addition to intend of myself to a greater extent than equally an investor than a trader, but I am non a valuation snob. I chose the path I did because it works for me in addition to reflects my beliefs, but it would last both arrogant in addition to incorrect for me to scrap that beingness a trader in addition to playing the pricing game is somehow less worthy of honor or returns. In fact, the terminate game for both investors in addition to traders is to brand money, in addition to if you lot tin brand coin past times screening stocks using PE ratios or technical indicators, in addition to timing your entry/exit past times looking at charts, all the to a greater extent than powerfulness to you! If at that topographic point is a indicate to this post, it is that a cracking deal of pricing, equally practiced today, is sloppy in addition to ignores, or throws away, information that tin last used to brand pricing better.