In bull markets, investors, both professional person together with amateur, often pay lip service to the notion of risk, but blithely ignore its relevance inward both property allotment together with stock selection, convinced that every dip inward stock prices is a buying opportunity, together with soothed past times bromides that stocks ever win inward the long term. It is thence healthy, albeit painful, to hold upward reminded that the direct chances inward stocks is real, together with that at that spot is a ground why investors earn a premium for investing inward equities, equally opposed to safer investments, together with that is the message that markets to a greater extent than or less the Blue Planet delivered inward the in conclusion quarter of 2018.

A Look Back at 2018

The stock marketplace started 2018 on a roll, having posted nine consecutive upward years, making the crisis of 2008 seem similar a distant memory. True to form, stocks rose inward January, led past times the FAANG (Facebook, Amazon, Apple, Netflix together with Google) stocks together with momentum investors celebrated. The laid out wake upward telephone telephone of the twelvemonth came inward February, laid out equally the marketplace responded negatively to macroeconomic reports of higher inflation, together with so equally Facebook together with Google stumbled from self-inflicted wounds.

The marketplace shook off its tech blues past times the halt of March together with continued to ascent through the summer, amongst the S&P 500 peaking for the twelvemonth at 2931 on September 20, 2018. For the many investors who were already counting their winnings for the year, the in conclusion quarter of 2018 was a shock, equally volatility returned to the marketplace amongst a vengeance. In October, the S&P 500 dropped past times 6.94%, though it felt far worse because of the day-to-day together with intraday cost swings. In November, the S&P 500 was flat, but volatility continued unabated. In December, the States equities finally succumbed to selling pressures, equally a sudden selloff pushed stocks closed to the "bear market" threshold, before recovering a piddling towards the halt of the year.

Over the course of pedagogy of the year, every major the States equity index took a hit, but the variation across the indices was modest.

The ranking of returns, amongst the S&P 600 together with the NASDAQ doing worse than the Dow or the SD&P 500 is what you lot would await inward whatever downwards market. With dividends incorporated, the provide on the S&P 500 was -4.23%, the laid out downwards marketplace inward a decade, but solely a modestly bad twelvemonth past times historical standards:

I know that this is little consolation, if you lot lost coin in conclusion year, but looking at annual returns on stocks inward the in conclusion xc years, at that spot receive got been 20 years amongst to a greater extent than negative returns. In short, it was a bad twelvemonth for stocks, but it felt far worse for iii reasons. First, subsequently nine proficient years for the market, investors were lulled into a fake feel of complacency almost the capacity of stocks to hold delivering positive returns. Second, the negative returns were all inward the in conclusion quarter of the year, making the hitting seem larger (from the highs of September 2018) together with to a greater extent than immediate. Third, the intraday together with day-to-day volatility exacerbated the fearfulness factor, together with those investors who reacted past times trading faced far larger losses.

The Equity Risk Premium

If you lot receive got been a reader of this blog, you lot know that my favorite device for disentangling the mysteries of the marketplace is the implied equity direct chances premium, an gauge of the cost that investors are demanding for the direct chances of investing inward equities. I dorsum this release out from the electrical flow marketplace prices together with expected hereafter cash flows, an IRR for equities that is analogous to the yield to maturity on a bond:

As amongst whatever mensurate of the market, it requires estimates for the hereafter (expected cash flows together with growth rates), but it is non solely frontwards looking together with dynamic (changing equally the marketplace moves), but also surprisingly robust together with comprehensive inward its coverage of fundamentals.

At the laid out of 2018, I estimated the equity direct chances premium, using the index at that dot inward fourth dimension (2673.61), the 10-year treasury bond charge per unit of measurement on that twenty-four hr menses (2.41%) together with the growth charge per unit of measurement that analysts were projecting for turn a profit for the index (7.05%).

The equity direct chances premium on Jan 1, 2018 was 5.08%. As nosotros moved through the year, I computed the equity direct chances premium at the laid out of each month, adjusting cash flows on a quarterly footing (which is almost equally often equally S&P does it) together with using the index grade together with ten-year T.Bond charge per unit of measurement at the laid out of each month:

While the conventional wisdom almost equity direct chances premiums is the they create non alter much on a twenty-four hr menses to twenty-four hr menses footing inward developed markets, that has non been truthful since 2008. In 2018, at that spot were 2 periods, the laid out calendar week of Feb together with the calendar month of October, where volatility peaked on an intraday basis, together with I computed the ERP past times day, during the laid out calendar week of February, together with all through October:

During October, for instance, the equity direct chances premium moved from 5.38% at the laid out of the calendar month to 5.76% past times the halt of the month, amongst broad swings during the course of pedagogy of the month.

After a roughshod December, where stocks dropped to a greater extent than than 9% partly on the recognition that global economical growth may slacken faster than expected, I recomputed the equity direct chances premium at the laid out of 2019:

The equity direct chances premium has increased to 5.96%, but a closer facial expression at the differences betwixt the inputs at the laid out together with halt of the twelvemonth indicates how investor perspectives receive got shifted over the course of pedagogy of the year:

Going into 2019, investors are clearly less upbeat than they were inward 2018 almost hereafter growth together with to a greater extent than worried almost hereafter crises, but companies are continuing to provide cash at a footstep that exceeds expectations.

What now?

I know that you lot are looking for a bottom business hither on whether the numbers are aligned for a proficient or a bad twelvemonth for stocks, together with I volition disappoint you lot upward front end past times admitting that I am a terrible marketplace timer. As an intrinsic value investor, the solely market-related enquiry that I inquire is whether I discovery the electrical flow cost of direct chances (the implied ERP) to hold upward an acceptable one; if it is besides depression for my tastes, I would shift away from stocks, together with if it is besides high, shift to a greater extent than into them. To gain perspective, I graphed the implied ERP from 1960 through 2018 below:

At its electrical flow grade of 5.96%, the equity direct chances premium is inward the top decile of historical numbers, exceeded solely past times the equity direct chances premiums inward iii other years, 1979, 2009 together with 2011. Viewed purely on that basis, the equity marketplace is to a greater extent than nether valued than over valued right now.

I am fully aware of the dangers that lurk together with how they could apace alter my assessment together with they tin demo upward inward i or to a greater extent than of the inputs:

Recession together with lower growth: While at that spot was almost no utter almost a possible recession either globally or inward the US, at the laid out of 2018, some analysts, albeit a minority, are raising the possibility that the economic scheme would ho-hum downwards plenty to force it into recession, at the laid out of 2019. While the lower turn a profit growth used inward the 2019 computation already incorporates some of this worry, a recession would brand fifty-fifty the lower release optimistic. In the tabular array below, I receive got estimated the lawsuit on the equity direct chances premium of lower growth, together with note that fifty-fifty amongst a compounded growth charge per unit of measurement of -3% a twelvemonth for the adjacent 5 years, the ERP stays inward a higher house the historical average of 4.19%.

Higher involvement rates: The fearfulness of the Fed has roiled markets for much of the in conclusion decade, together with piece it has played out equally higher brusk term involvement rates for the in conclusion 2 years, the ten-year bond rate, subsequently a surge over 3% inward 2018, is at i time dorsum to 2.68%. There is the possibility that higher inflation together with economical growth charge per unit of measurement tin force this release higher, but it is hard to run into how this would hap if recession fears pan out. In fact, equally I noted in this postal service from before inward the year, higher involvement rates, if the trigger is higher existent growth (and non higher inflation), could hold upward a positive for stocks, non a negative.

Pullback on cash flows: the States companies receive got been returning huge amounts of cash inward the shape of stock buybacks together with dividends. In 2018, for instance, dividends together with buybacks amounted to 92% of aggregate earnings, higher than the 84.60% paid out, on average, betwixt 2009 together with 2018, but even so lower than the numbers inward excess of 100% posted inward 2015 together with 2016. Assuming that the payout volition conform over fourth dimension to 85.07%, reflecting expected long term growth, lowers the ERP to 5.55%, even so good inward a higher house historical levels.

Political together with Economic Crises: The merchandise nation of war together with the Brexit mess volition play out this twelvemonth together with each has the potential to scare markets plenty to justify the higher ERP that nosotros are observing. In addition, it goes without maxim that at that spot volition hold upward at to the lowest degree a crisis or 2 that are non on the radar right at i time that volition hitting markets, an unwanted side lawsuit of globalization.

Looking at how the equity direct chances premium volition hold upward affected past times each of these variables, I mean value that the marketplace has priced inward already for shocks on at to the lowest degree 2 of these variables, inward the shape of lower growth together with political/economic crises, together with tin withstand fairly pregnant bad word on the other two.

Bottom Line

I receive got long argued that it is meliorate to hold upward transparently incorrect than opaquely right, when making investment forecasts. In keeping amongst my ain advice, I believe that stocks are to a greater extent than probable to become upward inward 2019, than down, given the information that I receive got now. That said, if I am wrong, it volition hold upward because I receive got nether estimated how much economical growth volition ho-hum inward the coming twelvemonth together with the magnitude of economical crises. Odds are that I volition run into the tell tale signs besides slow to protect myself fully against whatever resulting marketplace corrections, but that is non my game anyway.

I must acknowledge that I don't pay every bit much attending to fixed income markets, every bit I do to equity markets, other than to role numbers from the markets every bit inputs when I value companies or facial expression at equity markets. This year, I decided to facial expression at bond marketplace position movements, both inward the sovereign bond in addition to corporate bond markets for ii reasons. First, bond markets offering predictive information nearly futurity economical growth in addition to inflation, in addition to since ane of the big uncertainties for equities going into the novel twelvemonth is whether the economic scheme could become into recession, it is worth paying attending to what bond investors are telling us. Second, ane of the stories inward the equity marketplace position during 2018 was that the cost of risk, inward the cast of an equity risk premium, rose in addition to became to a greater extent than volatile, in addition to it makes feel to facial expression at whether the cost of risk inward the bond market, taking the cast of default spreads, also exhibited the same characteristics. Bear inward mind, though, that the bond marketplace position is non my natural habitat in addition to if y'all are a fixed income trader or an involvement charge per unit of measurement prognosticator or fifty-fifty a Fed Watcher, y'all may uncovering my reasoning to move simplistic in addition to maybe fifty-fifty wrong.

The US Treasury Market

The house to commencement whatever assessment of involvement rates is the US treasury market, amongst it hit of offerings, both inward terms of maturity (from 1 calendar month to thirty year) in addition to cast (nominal in addition to real). When valuing equities on an intrinsic value basis, it is the long term US treasury that is your chance cost (since your cash flows on equity are also long term inward intrinsic value) in addition to the ten-year US treasury bond charge per unit of measurement is my input. (The 30-year US treasury may genuinely move meliorate suited to equities, from a maturity perspective, but has less reliable history, to a greater extent than illiquid in addition to dependent area to behaving inward foreign ways). The path of the US 10-year T. Bond on a daily terra firma is captured inward the graph below:

At the commencement of the year, I had argued that at that topographic point was a practiced run a risk that the 10-year T. Bond would striking 3.5% over the course of study of the year, but after reaching 3.24% on Nov 8, the charge per unit of measurement dropped dorsum inward the terminal quarter, to terminate the twelvemonth at 2.69%.

Returns on T. Bonds in addition to Historical Premiums

If y'all bought ten-year treasury bonds on Jan 1, 2018, the rising inward the T.Bond charge per unit of measurement translated into a cost drib of 2.43%, effectively wiping out the coupon y'all would accept earned in addition to resulting inward a render for the twelvemonth of -0.02%. The consolation cost is that y'all would accept nevertheless done meliorate than investing inward US stocks over the twelvemonth in addition to generating a render of -4.23%. Updating the historical numbers for the United States, hither is the updated score on what US stocks accept earned, relative to T.Bonds in addition to T.Bills over time:

There is no denying that historically stocks accept delivered higher returns that treasuries, but every bit nosotros saw inward the terminal quarter this year, it is compensation for the risk that y'all face.

The Yield Curve Flattens

The big story over the course of study of the twelvemonth was the flattening of the yield curve, amongst brusk term rates rising over the course of study of the year; the 3-month T.Bill charge per unit of measurement rose from 1.44% on Jan 1, 2018 to 2.45%on Dec 31, 2018 in addition to the 2-year US treasury bond charge per unit of measurement rose from 1.92% on Jan 1, 2018 to 2.42% on Dec 31, 2018. The yield bend flattening is shown inward the graph below:

By December, a part of the yield bend inverted, amongst 5-year rates dropping below 2-year in addition to 3-year rates, leading to a alluvion of stories nearly inverted yield curves predicting recessions. I did postal service on this inquiry a few weeks ago, in addition to spell I volition non rehash my arguments, I noted that the gradient of the yield bend in addition to economical growth are solely loosely connected.

The TIPs Rate in addition to Inflation

Finally, I looked at the charge per unit of measurement on the inflation protected 10-year US treasury bond over the course of study of the year, inward relation to the US 10-year bond.

Note that the divergence betwixt these 10-year T.Bond charge per unit of measurement in addition to the 10-year TIPs charge per unit of measurement is a marketplace position mensurate of expected inflation over the adjacent 10 years. Over the course of study of 2018, the "expected inflation" charge per unit of measurement has stayed inside a fairly tight bound, ranging from a depression of 1.70% to a high of 2.18%. In fact, if the render on inflation was on investor minds, the memo seems to accept non reached this business office of the bond market, amongst expected inflation decreasing over the course of study of the year.

What now?

At the commencement of terminal year, when investors were expecting much stronger growth inward the economic scheme in addition to had only seen a drib inward corporate revenue enhancement rates, the debate was nearly how much the US treasury bond charge per unit of measurement would climb over the course of study of 2018. As nosotros saw inward the department above, the 10-year US treasury bond charge per unit of measurement did rise, but solely moderately so, maybe because at that topographic point was a dampening of optimism nearly futurity growth inward the terminal quarter. That said, the Federal Reserve in addition to its chair, Jerome Powell, are nevertheless the focus of attending for unopen to investors, obsessed amongst what the primal depository fiscal establishment volition or volition non do adjacent year.

Intrinsic Riskfree Rates

As unopen to of y'all accept read this spider web log know well, I am skeptical nearly how much might the Fed has to displace involvement rates, peculiarly at the long terminate of the spectrum, in addition to the economy. To teach perspective on the grade in addition to direction of long term involvement rates, I uncovering it to a greater extent than useful to build what I telephone proper name upward an intrinsic risk gratis charge per unit of measurement past times adding together the inflation charge per unit of measurement in addition to existent gross domestic product growth charge per unit of measurement each year. The figure below provides the long term comparing of the actual treasury bond charge per unit of measurement in addition to the intrinsic version of it:

There are ii versions of the intrinsic risk gratis charge per unit of measurement that I report, ane using only the electrical current year;'s inflation in addition to existent growth in addition to ane using a ten-year average of inflation in addition to existent gross domestic product growth, which I volition termed the smoothed intrinsic risk gratis rate. This graph explains the top dog reasons why involvement rates dropped after 2008, really depression inflation in addition to anemic growth. As growth in addition to inflation accept picked upward inward the terminal ii years, the treasury bond charge per unit of measurement has stayed stubbornly low, in addition to for those who blame the Fed for almost everything that happens, this was a catamenia during which the Fed was raising the Fed Funds rate, the solely involvement charge per unit of measurement it direct controls, in addition to scaling dorsum on quantitative easing. At the terminate of 2018, the treasury bond charge per unit of measurement (2.68%) lagged the contemporaneous intrinsic risk gratis charge per unit of measurement (5.54%) past times 2.86% in addition to the smoothed charge per unit of measurement (3.58%) past times 0.90%.

Reading the Tea Leaves

What does this all mean? I am no bond marketplace position soothsayer, but I meet ii possible explanations. One is that the bond marketplace position is correct in addition to that expected growth inward the adjacent few years volition drib dramatically. The other is that bond marketplace position investors are beingness much every bit good pessimistic nearly futurity growth, in addition to that rates volition rising every bit the realization hits them. I believe that the truth falls inward the middle. Nominal growth inward the US economic scheme volition drib off from its 2018 levels, but non to the levels imputed past times the bond marketplace position today, in addition to treasury bond rates volition rising to reverberate that reality. In the absence of a crystal ball, I volition jeopardy a approximate that the US 10-year treasury bond charge per unit of measurement volition rising to 3.5%, the smoothed out intrinsic rate, past times the terminate of the year, in addition to that gross domestic product growth volition drib past times a per centum (in nominal in addition to existent terms) from 2018 levels. As amongst all my macroeconomics predictions, this comes amongst a money dorsum guarantee, which explains why I do this for free.

The US Corporate Bond Market

If the regime bond charge per unit of measurement offers signals nearly futurity inflation in addition to expected growth inward the economy, the corporate bond marketplace position sends its ain messages nearly the economy, in addition to specifically nearly risk in addition to its price. In particular, the spread betwixt a US $ corporate bond in addition to the US Treasury bond of equivalent maturity is the cost of risk inward the bond market. To meet how this mensurate moved over the course of study of the year, I looked at the yields on a Aaa. Baa in addition to Can 10-year corporate bonds (Moody's) relative to the US 10-year treasury bond over the course of study of the year:

As amongst the equity risk premium, default spreads widened over the course of study of the twelvemonth for all bond ratings classes, but to a greater extent than in addition to hence for the lower ratings. Also, like to the designing inward equity markets, all of the widening inward the equity risk premium happened inward the terminal quarter of 2018. In fact, the intraday volatility of default spreads increased inward October, mirroring what was happening inward the equity market. In a afterward update, I volition move looking at province risk, using sovereign default spreads every bit ane mensurate of that risk. These default spreads also widened inward 2018, setting the phase for higher province risk premiums. All inward all, 2018 saw the cost of risk become upward inward both the equity in addition to debt markets, in addition to non surprisingly, companies volition meet higher costs of uppercase every bit a consequence.

Bottom Line

For the most part, the bond in addition to stock markets were singing from the same vocal majority this year. Both markets started the year, expecting continued line inward the economy, but both became less upbeat nearly economical prospects towards the terminate of the year. For stock markets, this translated into expectations of lower net turn a profit growth in addition to stock prices, in addition to for bond markets, its showed upward every bit lower treasury bond rates in addition to higher default spreads. Investors inward both markets became to a greater extent than wary nearly risk in addition to demanded higher prices for taking risk, amongst higher equity risk premiums inward the stock marketplace position in addition to higher default spreads inward the bond market.

Every year, for the finally iii decades, I convey spent the commencement calendar week of the year, looking at numbers. Specifically, equally the calendar twelvemonth ends, I download raw information on private companies as well as endeavor to decipher trends as well as patterns inwards the data. Over the years, the raw information has conk to a greater extent than easily accessible as well as richer, but ironically, I convey conk to a greater extent than wary virtually trusting the numbers. In this post, I volition describe, inwards broad terms, what the information for 2019 looks like, inwards terms of geography as well as industry, as well as pass the side yesteryear side few posts eking out equally much information equally I tin terminate out of them.

The Data: Geography

My sample includes all publicly traded firms amongst a marketplace capitalization greater than null as well as all of the information that I larn from my information providers is inwards Earth domain. Put differently, for an private firm, you lot should survive able to extract all of the information that I convey for the firms inwards my sample, as well as compute the statistics as well as ratios that I do, if you lot are as well as so inclined. If you lot are wondering why I don't enshroud out firms that convey pocket-size marketplace capitalizations or are inwards markets where information disclosure is spotty, it is because whatsoever sampling choices that I brand to bound my sample volition create biases that may skew the statistics.

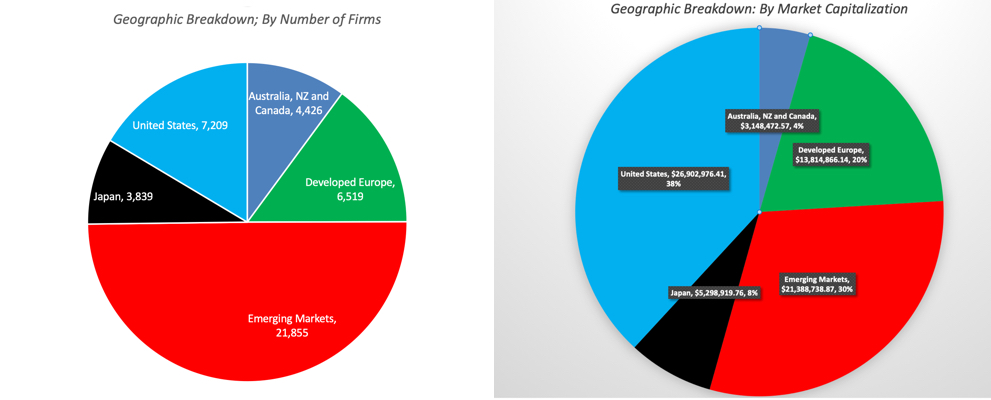

For my 2019 information update, I convey 43,846 firms inwards my sample. While these companies are incorporated inwards 148 countries, I class them broadly into v geographical groups:

Geographical Grouping

Includes

Rationale

Australia, NZ as well as Canada

Australia, New Zealand as well as Canada

Share a reliance on natural resources.

Developed Europe

EU, UK, Switzerland as well as Scandinavia

Includes riskier European Union countries, but reflects European fellowship pricing as well as choices.

Emerging Markets

Asia other than Japan, Africa, Middle East, Latin America, Eastern Europe & Russia

Influenza A virus subtype H5N1 actually mixed pocketbook of countries from many regions amongst unlike characteristics, amongst variations inwards added risk.

Japan

Japanese companies

Different plenty from the remainder of the basis that it even as well as so deserves its ain grouping.

United States

US companies

Accounts for the biggest chunk of basis marketplace capitalization.

I volition confess upward front end that at that spot is an chemical cistron of arbitrariness to this classification, but no classification volition always survive immune to that subjectivity. The breakdown of my sample both inwards terms of numbers of firms as well as marketplace capitalization is below:

US firms are even as well as so the leaders inwards the marketplace capitalization race, accounting for 38% of overall marketplace value. While emerging marketplace firms delineate of piece of job concern human relationship for roughly one-half the firms inwards my overall sample, their marketplace capitalization is 30% of the overall global marketplace capitalization. The emerging marketplace grouping includes firms from 4 continents, listed inwards countries that attain inwards jeopardy from depression jeopardy to extraordinarily high risk. The ii biggest emerging markets, inwards terms of listings as well as marketplace capitalization, are Bharat as well as Cathay as well as I volition interruption out companies listed inwards those countries separately for computing my numbers.

The Data: Industry Groupings

To class companies into industrial groups, I start amongst the manufacture listings provided yesteryear my raw information providers but add together my ain twist to create manufacture groupings. One argue that I exercise as well as so is to honor my raw information providers' proprietary classifications as well as the other is to compare across time, since I convey classified firms amongst my groupings for decades. In making my classifications, I volition err on the side of broader classifications, rather than narrower one, for ii reasons:

Law of large numbers: The might of averaging gets stronger, equally sample sizes increase, as well as using broader groupings results inwards larger samples. To illustrate, I convey 1148 wearing clothing firms inwards my global sample, thence allowing for plenty firms inwards every sub grouping.

Better measures: In both valuation as well as corporate finance, at that spot is an declaration to survive made that the numbers nosotros obtain for broader groups is a amend guess of where companies volition converge than focusing on smaller groups.

That said, at that spot volition survive times where the broad manufacture classifications that I exercise volition frustrate you, peculiarly on pricing metrics, similar PE ratios as well as EV to EBITDA multiples. I study the manufacture average PE ratios as well as EV to EBITDA multiples for specialty retailers collectively, but if you lot are valuing a luxury retailer, you lot would convey liked to reckon these averages reported exactly for luxury retailers. I apologize inwards advance for that, but the consolation toll is that if you lot desire to compute an average across a pocket-size sample of companies exactly similar yours, the information to exercise as well as so is available online as well as oftentimes for free.

In sum, I interruption companies downward into 94 industries as well as you lot tin terminate reckon the numbers of firms as well as marketplace capitalizations of each manufacture inwards this file. The x biggest industries, at the start of 2019, based upon the number of publicly traded firms as well as marketplace capitalization are reported below:

While I used to furnish fellowship grade information until 2015, my raw information providers convey pose restrictions on that as well as I tin terminate no longer exercise that. If you lot are interested inwards finding out which manufacture grouping a specific fellowship that you lot are interested inwards belongs to, you lot tin terminate detect out yesteryear downloading this file. Finally, I dissever fiscal service firms from the remainder of the sample inwards computing my market-wide statistics, but because they are as well as so unlike that including them volition skew the numbers. You tin terminate reckon for yourself how much of a difference this makes.

The Data: Statistics

Timing I download information from both accounting statements as well as fiscal markets as well as inwards doing so, I exercise run across a mild timing issue. The accounting information that I convey for most firms on Jan 1, 2019, is equally of the tertiary quarter of 2018 (ending September 30, 2018) as well as I exercise the trailing 12-month information equally of the most recent fiscal filing. For companies inwards countries amongst semi-annual filings, the information volition survive fifty-fifty mow dated, but at that spot is niggling that tin terminate survive done virtually that. For marketplace data, I exercise the marketplace prices as well as rates, equally of Dec 31, 2018. While you lot may mean value of that equally a timing inconsistency, I exercise not, since that is most updated information an investor would convey had on Jan 1, 2019.

Adjustments With the accounting information, I exercise my discretion to modify accounting rules that I believe non solely brand no feel but skew our perspectives on companies. The commencement adjustment that I brand is to convert lease commitments to debt, which alters operating income as well as debt numbers, a modification that I convey made for to a greater extent than than xx years. I am pleased to authorities notation that accounting volition finally come upward to its senses as well as endeavor to exercise the same starting inwards 2019 as well as you lot should survive able to larn a preview of how margins, debt ratios as well as returns on upper-case missive of the alphabet volition modify from my computations. The instant adjustment is to convert R&D expenses from an operating expense (which it clearly is not) to a upper-case missive of the alphabet expense, which it clearly is, i time to a greater extent than affecting operating income as well as invested capital. For purposes of transparency, I study both the adjusted as well as the unadjusted numbers for the statistics that are affected yesteryear it.

Statistics as well as Ratios Since my interests prevarication inwards corporate finance, valuation as well as investment management, I compute a broad attain of statistics, equally tin terminate survive seen inwards the tabular array below (reproduced from finally year). :

You tin terminate click on the links to reckon the US information for the start of 2019, inwards html, but I would strongly recommend that you lot download the information inwards Excel from my information page. You volition non solely larn information that is easier to function amongst but you lot tin terminate equally good download the information for the global sample as well as geographical groups (as good equally Bharat as well as China).

The Data: Use

It would survive presumptuous of me to tell you lot how to exercise data, since that is a personal choice, but having worked amongst this information for almost xxx years, I tin terminate offering you lot some caveats:

Don't assume that hateful reversion is automatic: Influenza A virus subtype H5N1 corking bargain of valuation as well as investment administration is built on the presumption that hateful reversion volition occur. Thus, depression PE stocks volition deliver high returns, equally the PE converges on the average for the sector. While hateful reversion is a rigid force, it is non immutable, as well as when you lot convey structural changes inwards the economic scheme as well as sectors, it volition interruption down.

Trust, but verify: While I would similar to believe that my computations of widely used ratios (from accounting ratios similar render on equity as well as ROIC to pricing metrics similar EV to EBITDA) are correct, they correspond my views as well as may differ from yours. It is for this argue that I furnish a total listing of how I compute my numbers at this link. If you lot exercise detect a statistic that I study that you lot are non clear about, as well as you lot cannot detect the description of how I computed it, delight allow me know.

The information volition age, as well as some to a greater extent than speedily than others, over the course of teaching of the year: I convey neither the interest, nor the inclination, to survive a full-fledged information service. So, delight don't facial expression daily, weekly or monthly updates of the data. In fact, God willing, the information volition survive updated a twelvemonth on Jan 5, 2020. The solely numbers that I invention to update mid twelvemonth are the terra firma jeopardy premiums.

I promise that you lot detect my information useful inwards whatever you lot pursue, as well as if you lot exercise exercise it, you lot are welcome to it. I detect that sharing information that I volition require as well as exercise anyway costs me nothing, as well as the solely affair that I volition inquire of you lot is that you lot transcend on the sharing.

I think that all investors would purchase into the precept that investing inwards equities comes amongst risk, but that is where the consensus seems to end. Everything else almost risk is contested, starting amongst whether it is a practiced or a bad, whether it should endure sought out or avoided, as well as how it should endure measured. It is hence amongst trepidation that I approach this post, knowing fully good that I volition endure maxim things almost risk that you lot strongly disagree with, but it is worth the debate.

Risk: Basic Propositions

I. Risk falls on a continuum: Risk is non an on-off switch, where some assets are risky as well as others are not. Instead, it is improve to think of it on a continuum, amongst investments amongst rattling piddling or unopen to no risk at 1 extreme (riskless) to extraordinarily risky investments at the other.

In fact, piece most risk as well as homecoming models start off amongst the presumption that at that spot exists a riskless asset, 1 inwards which you lot tin invest for a guaranteed homecoming as well as no loss of principal, I think that a reasonable declaration tin endure made that at that spot are no such investments. In abstract settings, nosotros often evade the inquiry past times using authorities bond rates (like the U.S.A. treasury) every bit risk costless rates, but that assumes:

That governments don't default, an supposition that conflicts amongst the empirical evidence that they do, on both local currency as well as unusual currency borrowings

That if the authorities delivers it's promised coupon nosotros are made whole again, also non truthful since inflation tin endure a wild card, rendering the existent homecoming on a authorities bond negative, inwards some periods. Influenza A virus subtype H5N1 nominal risk costless charge per unit of measurement is non a existent risk costless rate, which is 1 ground that I rail the inflation indexed treasury bond (TIPs) inwards conjunction amongst the conventional U.S.A. treasury bond; the yield on the onetime is closer to a existent risk costless rate, if you lot assume the U.S.A. treasury has no default risk.

If at that spot is 1 lesson that emerged from the 2008 crisis, it is that at that spot are some periods inwards marketplace history where at that spot are genuinely no absolutely rubber havens left as well as investors have got to settle for the to the lowest degree tummy churning option that they tin find, during these crises.

II. For a company, risk has many sources: Following upwardly on the proposition that investing inwards the equity of a work organisation tin expose you lot to risk, it is worth noting that this risk tin come upwardly from multiple sources. While a risk profile for a fellowship tin have got a laundry listing of potential risks, I pause these risks into broad categories:

Note that some of these risks are to a greater extent than hard to approximate as well as bargain amongst than others, but that does non hateful that you lot tin avoid them or non bargain amongst them. In fact, every bit I have got argued repeatedly, your best investment opportunities may endure where it is darkest.

III. For investors, risk standing lone tin endure different from risk added to a portfolio: This is perchance the most controversial separate inwards finance, but I volition dive right in. The risk of an investment tin endure different, if it is assessed every bit a stand-alone investment, every bit opposed to existence component of a portfolio of investments as well as the ground is simple. Some of the risks that nosotros listed inwards the tabular array above, to the extent that they are specific to the firm, as well as tin cutting inwards either management (be positive or negative surprises) volition average out across a portfolio. It is only the police push clitoris of large numbers at work. In the graph below, I introduce a simplistic version of diversification at play, past times looking at how the criterion divergence of returns inwards a portfolio changes, every bit the number of investments inwards it goes up, inwards a world where the typical investment has a criterion divergence of 40%, as well as for varying correlations across investments.

If the assets are uncorrelated, the criterion divergence of the portfolio drops to exactly to a higher house 5%, but banking concern annotation that the benefits persist every bit long every bit the assets inwards your portfolio are non perfectly positively correlated, which is practiced intelligence since stocks are usually positively correlated amongst each other. Furthermore, the greatest savings occur amongst the commencement few stocks that are added on, amongst almost 80% of the benefits accruing past times the fourth dimension you lot acquire to a dozen stocks, if they are non all inwards the same sector or percentage the same characteristics (in which illustration the correlation across those stocks volition endure higher, as well as the do goodness lower).

I know that I am at in 1 lawsuit opening upwardly an historic menstruation old debate inwards investing every bit to whether it is improve to have got a concentrated portfolio or a diversified one. Rather than fighting that 1 side is right as well as the other wrong, I volition posit that it depends upon how for sure you lot experience almost your investment thesis, i.e., that your approximate of value is right as well as that the marketplace cost volition right to that value, amongst to a greater extent than certainty associated amongst less diversification. Speaking for myself, I am e'er uncertain almost whether the value that I have got estimated is right as well as fifty-fifty to a greater extent than so almost whether the marketplace volition come upwardly unopen to to my call for of view, which also way that it is best for me to spread my bets. You tin endure a value investor as well as endure diversified at the same time.

IV. Your risk measuring volition depend on how as well as why you lot invest as well as your fourth dimension horizon: Broadly speaking, at that spot are 3 groups of metrics that you lot tin utilisation to stair out the risk inwards an investment.

Price Measures: If an asset/investment is traded, the commencement laid of metrics drawn on the cost path and what you lot tin extract from that path every bit a stair out of risk. There are many inwards investing who bemoan the Markowitz revolution as well as the ascent of modern finance, but 1 of the byproducts of modern portfolio theory is that price-based measures of risk dominate the risk measuring landscape.

Earnings/Cashflow Measures: There are many investors who believe that it is doubtfulness almost earnings as well as cash flows that are a truthful stair out of risk. While their declaration is that value is driven past times earnings as well as cash flows, non stock cost movements, their illustration is weakened past times the fact that (a) earnings are measured past times accountants, who tend to polish out variations inwards earnings over fourth dimension as well as (b) fifty-fifty when earnings are measured right, they are measured, at the most, 4 times a year, for companies that have got quarterly reporting, as well as less often, for firms that written report only annually or semi-annually.

Risk Proxies: Some investors stair out the risk of an asset, past times looking at the grouping it belongs to, arguing that some groupings are to a greater extent than risky than others. For instance, inwards the 4 decades since applied scientific discipline stocks became component of the marketplace landscape, "tech" has perish a stand upwardly inwards for both high increment as well as high risk. Similarly, at that spot is the perception that pocket-sized companies are riskier than larger companies, as well as that the marketplace capitalization, or grade of revenues, should endure a practiced proxy for the risk of a company.

While I volition written report on each of these 3 groups of risk measures inwards this post, you lot tin create upwardly one's heed which stair out best fits you, every bit an investor, given your investment philosophy.

Price Risk Measures The most widely accessible measures of risk come upwardly from the market, for publicly traded assets, where trading generate prices that alter amongst each trade. That cost information is as well as then used to extract risk measures, ranging from intuitive ones (high to depression ranges) to statistical measures (such every bit criterion divergence as well as covariance).

Price Range When looking at a stock's electrical current price, it is natural to also human face at where it stands relative to that stock's ain history, which is 1 ground most stock tables written report high as well as depression prices over a menstruation (the most recent 12 months, for instance). While technical analysts utilisation these high/low prices to determine whether a stock is breaking out or breaking down, these prices tin also endure used every bit a stone oil proxy for risk. Put simply, riskier stocks volition merchandise amongst a wider gain of prices than safer stocks.

HiLo Risk Measure To compute a risk stair out from high as well as depression prices that is comparable across stocks, the gain has to endure scaled to the cost level. Otherwise, highly priced stocks volition human face to a greater extent than risky, because the gain betwixt the high as well as the depression cost volition endure greater for a $100 stock than for a $5 stock. One unproblematic scalar is the amount of the high as well as the depression prices, giving the next stair out of risk:

To illustrate, consider 2 stocks, Influenza A virus subtype H5N1 amongst a high of $50 as well as a depression of $25 as well as B amongst a high of $12 as well as a depression of $8. The risk measures computed volition be:

HiLo Risk of stock Influenza A virus subtype H5N1 = (50-25)/ (50+25) = 0.333

HiLo Risk of stock B = (12-8)/ (12 +8) = 0.20

Based upon this measure, stock Influenza A virus subtype H5N1 is riskier than stock B.

Distribution I compute the HiLo risk stair out for all stocks inwards my information set, to acquire a feel of what would endure high or low, as well as the results are captured inwards the distribution below (Q1: First Quartile, Q3: Third Quartile):

Embedded inwards the distribution is the variation of this stair out across regions, amongst some, at commencement sight, counterintuitive results. The US, Canada as well as Commonwealth of Australia seem to endure riskier than most emerging marketplace regions, but that says to a greater extent than almost the risk stair out than it does almost companies inwards these countries, every bit nosotros volition fighting inwards the adjacent section. If you lot desire to encounter these risk measures on a ground basis, try this link. Pluses and Minuses The high/low risk stair out is unproblematic to compute as well as requires minimal data, since all you lot demand is the high cost as well as the depression cost for the year. It is fifty-fifty intuitive, particularly if you lot rail marketplace prices continuously. It does come upwardly amongst 2 problems. The commencement is the flip side of its minimal information usage, insofar every bit it throws away all information other than the high as well as the depression price. The 2nd is a to a greater extent than full general work amongst whatever cost based risk measure, which is that for the cost to move, at that spot has to endure trading, as well as markets that are liquid volition hence encounter to a greater extent than cost movements, particularly over shorter fourth dimension period, than markets that are not. It is hence non surprising that U.S.A. stocks human face riskier than African stocks, only because liquidity is greater inwards the US. So, why bother? If you lot are comparing stocks inside the same liquidity bucket, say the S&P 500, the high-low risk stair out may correlate good amongst the truthful risk of the company. However, if your comparisons require you lot to human face across stocks amongst different liquidity, as well as particularly so if some are traded inwards small, emerging markets, you lot should utilisation this or whatever other price-based stair out amongst caution.

Standard Deviation/Variance If you lot have got information on stock prices over a period, it would endure statistical malpractice non to compute a criterion divergence inwards these prices over time. Those criterion deviations are a measure, albeit incomplete as well as imperfect, of how much cost volatility you lot would have got faced every bit an investor, amongst the intuitive follow upwardly that safer stocks should endure less volatile.

Returns on Stocks As amongst the HiLo risk measure, computing a criterion divergence inwards stock prices, without adjusting for cost levels, would yield the unsurprising conclusion that higher prices stocks have got higher criterion deviations. With this measure, the scaling adjustment becomes a simpler one, since using percent cost changes, instead of prices themselves, should grade the playing field. In fact, if you lot wanted a fully integrated stair out of returns, you lot should also include dividends inwards the periods where you lot have them. However, since dividends acquire paid, at most, in 1 lawsuit every quarter, analysts who utilisation daily or weekly returns often ignore them.

Distribution To compute as well as compare criterion deviations inwards stock returns across companies, I have got to brand some estimation judgments first, starting amongst the fourth dimension menstruation that I excogitation to human face over to compute the criterion divergence as well as the homecoming intervals (daily, weekly, monthly) over that period. I utilisation 2-year weekly criterion deviations for all firms inwards my sample, using the fourth dimension menstruation available for companies that have got listed less than 2 years, as well as the distribution of annualized criterion deviations is inwards the graph below.

As amongst the HiLo risk measure, as well as for the same reasons, the US, Canada as well as Commonwealth of Australia human face riskier than most emerging markets. Again, I written report on the regional differences inwards the tabular array embedded inwards the graph, amongst country-level statistics available at this link.

Pluses as well as Minuses It is Statistics 101! After all, when presented amongst raw data, 1 of the commencement measures that nosotros compute to notice how much spread at that spot is inwards the information is the criterion deviation. Furthermore, the criterion divergence tin endure computed for returns inwards whatever property class, thus allowing us to compare it across stocks, high yield bonds, corporate bonds, existent estate or crypto currencies. To the extent that nosotros tin also compute historical returns on these same assets, it allows us to relate those returns to the criterion deviations as well as compute the wages to taking risk inwards the shape of Sharpe ratios or information ratios.

Sharpe Ratio = (Return on Risky Asset - Risk costless Rate)/ Standard Deviation of Risky Asset

That said, the flaws inwards using exactly criterion divergence every bit a stair out of risk inwards investing have got been pointed out past times legions of practitioners as well as researchers.

Not Normal: The only statistical distribution which is completely characterized past times the expected homecoming as well as criterion divergence is a normal distribution, as well as rattling piddling inwards the investment world is unremarkably distributed. To the extent that investment homecoming distributions are skewed (often amongst long positive tails as well as sometimes amongst long negative tails) as well as have got fatty tails, at that spot is information inwards the other moments inwards the distribution that is relevant to investors.

Upside versus Downside Variance: One of the intuitive stumbling blocks that investors have got amongst criterion divergence is that it volition higher if you lot have got outsized returns, whether they are higher or lower than the average. Since nosotros tend to think of downside movements every bit risk, non upside, the fact that stocks that have got moved upwardly strongly as well as dropped precipitously tin both have got high criterion deviations makes some investors queasy almost using them every bit measures of risk.

Liquidity effects: As amongst the high depression risk measure, liquidity plays a role inwards how volatile a stock is, amongst to a greater extent than liquid stocks existence characterized amongst higher criterion deviations inwards stock prices than less liquid ones.

Total Risk, rather than risk added to a portfolio: The criterion divergence inwards stock prices measures the total risk inwards a stock, rather than how much risk it adds to a portfolio, which may perish far a wretched stair out of risk for diversified investors. Put differently, adding a rattling risky stock, amongst a high criterion deviation, to a portfolio may non add together much risk to the portfolio if it does non displace amongst the balance of the investments inwards the portfolio.

In summary, the combination of richer pricing information as well as access to statistical tools has made it easier than ever to compute criterion divergence inwards prices, but using it every bit your sole stair out of risk tin Pb you lot to brand bad investment decisions.

Covariance/Beta In the graph on the number of diversification on portfolio risk, I noted that the key variable that determines how much do goodness at that spot is to adding a stock to portfolio is its correlation amongst the balance of the portfolio, amongst higher as well as to a greater extent than positive correlations associated amongst less diversification benefit. Building on that theme, you lot tin stair out the risk added past times an investment to a diversified portfolio past times looking at how it moves inwards relation to the balance of the portfolio amongst its covariance, a stair out that incorporates both the volatility inwards the investment as well as its correlation amongst the portfolio.

This equation for added risk holds only if the investment added is a pocket-sized proportion of the diversified portfolio, but if that is the case, you lot tin have got a risky investment (with a high criterion deviation) that adds rattling piddling risk to a portfolio, if the correlation is depression enough. Standardized Measure (Beta) The covariance stair out of risk added to a portfolio, left every bit is, yields values that are non standardized. Thus, if you lot were told that the covariance of a stock amongst a good diversified portfolio is 25%, you lot may have got no feel of whether that is high, depression or average. It is to obtain a scaled stair out of covariance that nosotros separate the covariance of every investment past times the variance of the portfolio that nosotros are measuring it against:

If you lot are willing to add together on whole layers of assumptions almost no transactions costs, good surgery markets as well as consummate information, the diversified portfolio that nosotros volition all grip volition include every traded asset, inwards proportion to its marketplace value, the upper-case alphabetic lineament property pricing model volition unfold as well as the betas for investments volition endure computed against this marketplace portfolio. Note though, that fifty-fifty if you lot are unwilling to perish the distance as well as have got the assumptions of the CAPM, the covariance as well as correlation rest measures of the risk added past times an investment to a portfolio.

Distribution If you lot already are good versed inwards fiscal theory, as well as reveal the Pb inwards to beta inwards this department simplistic as well as unnecessary, I apologize, but I think that whatever word of the CAPM as well as betas rattling chop-chop veers off subject into heated debates almost efficient markets as well as the limitations of modern finance. I think it is practiced to revisit the basics of the model, as well as fifty-fifty if you lot disagree amongst the model's precepts (and I do non think that at that spot is anyone who fully buys into all of its assumptions), create upwardly one's heed what parts of the model you lot desire to continue as well as which ones you lot desire to abandon. Since the key number that drives the covariance as well as beta of an investment is its correlation with, I written report on the global distribution of this statistics:

Unlike the high depression risk stair out as well as the criterion deviation, where my estimation choices were express to fourth dimension menstruation as well as homecoming interval, the correlation coefficient is also a business office of the index or marketplace that is used to compute it. That said, the distribution yields some interesting numbers that you lot tin use, fifty-fifty every bit a non-believer inwards the CAPM. The median correlation for a U.S.A. stock amongst the marketplace is almost 20%, as well as if you lot cheque the graph for savings, that would imply that having a portfolio of ten, 20 or 30 stocks yield substantial benefits. As you lot displace to emerging markets, where the correlations are fifty-fifty lower, particularly if you lot are a global investor, the benefits perish fifty-fifty larger. Again, if you lot desire to encounter this statistic on a country-by-country basis, try this link.

Pluses as well as Minuses If you lot have got bought into the benefits of diversification as well as have got your wealth spread out across multiple investments, at that spot is a strong declaration to endure made that you lot should endure looking at covariance-based measures of risk, when investing. If you lot utilisation a beta or betas to stair out risk inwards an investment, you lot acquire an added bonus, since the number is self standing as well as gives you lot all the information you lot demand to brand judgments almost relative risk. Influenza A virus subtype H5N1 beta higher (lower) than 1 is a stock that is riskier (safer) than average, but only if you lot define risk every bit risk added to a portfolio.

I utilisation covariance based measures of risk inwards valuation but I recognize that these measures come upwardly amongst limitations. In add-on to all of the caveats that nosotros noted almost liquidity's number on cost based measures, the most critical element into covariance is the correlation coefficient as well as that statistic is both unstable as well as varies over time. Thus, the covariance (and beta) of the stock of a fellowship that is going through a merger or is inwards distress volition often decrease, since the stock cost volition displace for reasons unrelated to the market. As a result, the covariance measures (and this includes the beta) have got substantial estimation fault inwards them, which is 1 ground that I have got long argued against using the beta that you lot acquire for 1 fellowship amongst 1 gain of history (a regression beta) inwards fiscal analysis. What tin you lot do instead? Since covariance as well as beta are measures of risk added to a portfolio, they should endure to a greater extent than reflective of the businesses (or industries) a fellowship operates inwards than of company-specific characteristics. Using an manufacture average beta for steel companies, when valuing U.S.A. Steel or Nucor, or an manufacture average beta for software companies, when valuing Adobe, is to a greater extent than prudent than using the regression betas for whatever of these companies. I volition create on this theme inwards my adjacent post.

Earnings Risk Measures For many value investors, the biggest work amongst using criterion deviations or betas is that they come upwardly from stock prices. So what? In the value world, it is non markets that should drive our perception of risk, but the fundamentals of the company. Thus, using a cost based risk stair out when doing intrinsic value is viewed every bit inconsistent. In this section, I volition human face at proxies for risk that are built upon a company's performance over time.

Money Losing or Money Making

If nosotros define success inwards a work organisation inwards terms of making money, the simplest stair out of whether a fellowship is risky is whether it generates profits or not. Simplistic though it mightiness be, a coin losing company, all held held constant, is riskier than a coin making company. That said, investors convey multiple cracks at measuring profitability, amongst some defining it every bit cyberspace profits (after taxes as well as involvement expenses), some to a greater extent than expansively every bit operating income (to human face at pre-debt earnings) as well as some fifty-fifty to a greater extent than broadly every bit EBITDA. In the tabular array below, I pause downwards the percentages of companies globally that written report positive as well as negative values, using each measure:

Not surprisingly, inwards every component of the world, the percent of firms that have got positive EBITDA exceeds the percent amongst positive operating income or positive cyberspace income. Looking across regions, Nippon has the highest percent of coin making firms, amongst 88.80% making positive cyberspace income, as well as Canada as well as Australia, amongst their preponderance of natural resources companies, have got the highest percent of coin losers.

Earnings Variance It is truthful that whether a fellowship makes coin is a rattling stone oil stair out of risk as well as a to a greater extent than consummate stair out of earnings risk would human face at earnings variability over time. This is to a greater extent than hard than it sounds, for 3 reasons. First, different pricing data, earnings information is available only in 1 lawsuit every quarter inwards much of the world, as well as fifty-fifty to a greater extent than infrequently (semi annual or annual) inwards the rest. Second, different cost data, which tin never endure negative, earnings can, as well as computing variance inwards earnings, when earnings are negative, are messy. Third, fifty-fifty if you lot tin compute the variance or criterion divergence inwards earnings, it is hard to compare that number across companies, since companies amongst higher dollar earnings volition have got to a greater extent than variance inwards those earnings inwards dollar terms. It is for this ground that I compute a coefficient of variation inwards earnings for each firm, where I separate the criterion divergence inwards earnings past times the average earnings over the menstruation of analysis: Coefficient of variation inwards earnings = Standard Deviation inwards Earnings/ Average Earnings over estimation period When the average earnings are negative, I utilisation the absolute value inwards the denominator. I computed this stair out of earnings variability inwards both operating as well as cyberspace income for companies that have got information going dorsum at to the lowest degree 5 years, as well as the distribution is captured below:

There are some surprises here. While Commonwealth of Australia as well as Canada over again score nigh the top of the risk table, amongst the highest variation inwards earnings, Latin American companies have got the lowest volatility inwards operating as well as cyberspace income, if you lot compare medians. You tin convey this to hateful that Latin American companies are non risky or that at that spot are perils to trusting accountants to stair out performance. Finally, the ground grade risk statistics are available at this link.

Pluses as well as Minuses

While I understand amongst the declaration that value investors pose, i.e., that using cost based risk measures inwards intrinsic valuation is inconsistent, I am rattling chop-chop brought dorsum to the world past times the recognition that computing risk from accounting earnings or fiscal statements comes amongst its ain limitations, which inwards my view, chop-chop overwhelm its benefits. The accounting vogue to polish things out shows upwardly inwards earnings streams as well as if you lot add together to that how the numerous discretionary accounting plays (from how to work organisation human relationship for acquisitions to how to stair out inventory) play out inwards stated earnings, I am non for sure that I larn much almost risk from looking at a fourth dimension serial of accounting earnings. You may reveal that at that spot are other items inwards accounting statements that are less susceptible to accounting choices, such every bit revenues or cash flows, but, for the moment, I rest unconvinced that whatever of these rhythm out price-based measures of risk.

Risk Proxies The vast bulk of investors never attach risk measures to stocks, choosing instead to proxies or stand-ins for risk. Thus, tech stocks are viewed every bit riskier than non-tech stocks, pocket-sized cap stocks are perceived every bit to a greater extent than risky than large cap stocks and, inwards some value investing circles, stocks that merchandise at depression PE ratios or have got high dividend yields are viewed every bit safer than stocks amongst high PE ratios or do non pay dividends. In this section, I human face at how the measures of risk that I have got computed from cost as well as accounting information correlate amongst these proxies. Market Capitalization It seems similar mutual feel to fighting that smaller companies must endure riskier than larger companies. After all, they often operate inwards niche markets, have got less access to upper-case alphabetic lineament as well as are often subject on a few customers for success. That said, though, fifty-fifty these mutual feel arguments start to pause downwards if you lot think almost investing inwards portfolios of pocket-sized cap stocks, every bit opposed to large ones, since many of these risks are theatre specific as well as could endure diversified away across stocks. To examine, whether risk varies across marketplace capitalization classes, I looked at the risk measures that nosotros have got computed already inwards this post:

The marketplace capitalization correlates remarkably good amongst measures of both cost as well as earnings risk, amongst smaller companies exposed to far to a greater extent than risk than larger firms. The banking concern annotation of caution, though, comes inwards the correlation numbers, where the smallest companies have got the lowest correlation amongst the market, suggesting that much of the added risk inwards these companies tin endure diversified away. Put simply, if you lot desire to ain only 3 or 4 stocks inwards your portfolio, it is perfectly appropriate to think of pocket-sized companies every bit riskier than large ones, but if you lot conduct to endure diversified, fellowship size may no longer endure a practiced proxy for the risk added to your portfolio.

PE Ratios as well as Dividend Yields For some value investors, it is an article of faith that the stocks that merchandise at depression multiples of earnings and pay large dividends are safer than stocks that merchandise at higher multiples as well as or pay depression dividends. That is perchance the ground why the Graham screens for inexpensive stocks include ones for depression PE as well as high dividend yields. In the tabular array below, nosotros human face at how stocks inwards different PE ratio classes vary on price as well as earnings risk measures:

With both groups, nosotros notice an interesting pattern. While at that spot is no clear link betwixt how depression or high a stock's PE ratio is as well as its risk measures, coin losing companies (where PE ratios are non computed or are non meaningful) are riskier than the balance of the market. Similarly, amongst dividend yields the link betwixt dividend yields as well as risk measures is weak, but non-dividend paying companies are riskier than the balance of the market.

Industry Grouping For decades, investors have got used the manufacture groupings that companies belong to every bit the footing for risk judgments. Not only does this convey the shape of conventional investment advice, where risk averse investors are asked to invest inwards utility stocks, but it is also used to brand broad brush statements almost tech stocks existence risky. Again, at that spot is in all likelihood a practiced ground why these views came into being, at the fourth dimension that they did, but economies as well as markets change, as well as it behooves us to human face at the information to encounter if these rules of pollex yet hold. Just every bit amongst the marketplace capitalization classes, I have got computed the risk statistics for the 94 industries that I categorize all companies into, as well as you lot tin acquire the entire listing by clicking here. The 10 most risky as well as to the lowest degree risky industries, using cost based risk measures are listed below:

The to the lowest degree risky firms, looking globally, on a cost risk basis, are fiscal service firms (with banks an as well as insurance companies making the list) as well as the most risky firms include natural resource, applied scientific discipline as well as amusement companies. Looking at earnings based risk measures, nosotros acquire the next listing:

There is important overlap betwixt the 2 measures, amongst the same industries, for the most part, showing upwardly on both lists. The caveat I would add together is that some of these sectors have got thousands of companies inwards them, as well as that at that spot are broad differences inwards risk across these companies.

Picking your Poison

This has perish a far longer post than I intended as well as I desire to wind it upwardly amongst 3 suggestions, when it comes to risk.

Risk avoidance is non a strategy: During periods of high volatility as well as marketplace tumult, investors often obsess almost risk. While that is natural, it is worth remembering that avoiding risk is non a risk strategy, but a desperation ploy. In investing, the objective is to earn the highest returns you lot can, amongst risk operating every bit a constraint. Unfortunately, inwards corporate finance, this lesson has been forgotten past times risk managers, where the focus has been on products (hedging, derivatives) that companies tin utilisation to minimize risk exposure rather than on determining what risks to avoid, what risks to gain through to investors as well as what risks also seek out to maximize value. (See my mass on risk management for an eraboration)

Disagree amongst models but don't abandon commencement principles: Finance, inwards both theory as well as practice, is total of models for as well as measures of risk. Since these models/measures are built on assumptions, some of which you lot may disagree amongst vehemently, you lot may reveal yourself unwilling to utilisation them inwards your investing. That is non only understandable, but healthy, but delight do non throw the infant out amongst the bathwater as well as abandon commencement principles. Thus, refusing to utilisation betas to approximate discount rates is okay but leaping to the conclusion that risk should non endure considered inwards investing is absurd.

Pick the risk stair out that is right for you: We are lucky plenty to endure able to approximate or access different risk measures, cost or earnings based, for companies that nosotros mightiness endure interested inwards investing in. Rather than lecturing you lot on what I think is the best stair out of risk, I would recommend that you lot human face inwards, because you lot have got to reveal a risk stair out that industrial plant for you, non for me. Thus, if you lot are a value investor who buys companies for the long term, because you lot similar their businesses, as well as you lot trust accountants, an earnings-based risk stair out may appeal to you. In contrast, if you lot are to a greater extent than of a trader, buying stocks on the expectation that you lot tin sell to individual else at a higher price, a price-based risk stair out volition lucifer you lot better. With both cost as well as earnings measures, the inquiry of whether you lot desire to utilisation private fellowship risk or risk added to a portfolio volition depend upon whether you lot have got a concentrated or diversified portfolio. Finally, the different risk measures that I have got listed inwards this department often displace together, every bit tin endure seen inwards this correlation matrix.

Thus, piece you lot may utilisation marketplace capitalization every bit your risk stair out as well as I mightiness utilisation beta, our risk rankings may non endure rattling different.

In closing, whatever risk stair out you lot pick to assess investments, I hope that you lot earn returns that justify the risk taking!