I alive inward a prosperous suburb, sustained largely yesteryear fiscal service businesses, but every bit far I know, at that topographic point is entirely 1 Ferrari inward my town. Much of the week, the machine sits inward a garage which has its ain safety system, to a greater extent than secure than the 1 protecting its owner's house, as well as on a squeamish weekend, you lot run across the possessor drive it about town. It is a remarkably inefficient transportation mode, also fast for suburban roads, also expensive to hold upward parked at a grocery flush or pharmacy, as well as also cramped for machine pool. All of this comes to mind, for 2 reasons. The starting fourth dimension is the imminent initial world offering of the company, alongside all the pomp as well as circumstance that surrounds a high-profile offering. The instant is that this offering has laid inward motion the common utter of construct names as well as the cost premiums that nosotros should pay to partake for investing inward them.

Ferrari: H5N1 Short History as well as Background

The Ferrari flush started alongside Enzo Ferrari, a racing machine enthusiast, starting Scuderia Ferrari inward 1929, to aid as well as sponsor race machine drivers driving Alfa Romeos. While Enzo manufactured his starting fourth dimension racing machine (Tipo 815) inward 1940, Ferrari every bit a machine making society was founded inward 1947, alongside its manufacturing facilities inward Maranello inward Italy. For much of its early on existence, it was privately owned yesteryear the Ferrari family, though it is said that Enzo viewed it primarily every bit a racing machine society that happened to sell cars to the public. In the mid-1960s, inward fiscal trouble, Enzo Ferrari sold a 50% stake inward the society to Fiat. That asset was afterward increased to 90% inward 1988 (with the Ferrari identify unit of measurement retaining the remaining 10%). Since then, the society has been a small, albeit a real profitable, patch of Fiat (and FCA).

The society acquired its legendary status on the race tracks, as well as holds the tape for most wins (221) inward Formula 1 races inward history. Reflecting this history, Ferrari even so generates revenues from Formula 1 racing, alongside its part amounting to $67 1 1000 m inward 2014. Much every bit this may hurting machine enthusiasts everywhere, some of Ferrari's standing comes from its connexion to celebrities. From Thor Batista to Justin Bieber to Kylie Jenner, the Ferrari has been an musical instrument of misbehavior for wealthy celebrities all over the world.

The Auto Business

In before posts, where I valued Tesla, GM as well as Volkswagen, I argued that the auto line of piece of job organisation bore the characteristics of a bad business, where companies collectively earn less than their cost of majuscule as well as most companies destroy value. In fact, I used the words of Sergio Marchionne, CEO of Fiat Chrysler (and the parent society to Ferrari) to construct the representative that the top managers at auto companies were delusional inward their belief that the line of piece of job organisation would magically plough around. Looking at the line of piece of job organisation broadly, hither are iii characteristics that let out themselves:

1. It is a depression growth business: The auto line of piece of job organisation is a cyclical one, alongside ups as well as downs that reverberate economical cycles, but fifty-fifty allowing for this cyclicality, the line of piece of job organisation is a mature one. That is reflected inward the growth charge per unit of measurement inward revenues at auto companies.

Year

Revenues ($)

% Growth Rate

2005

1,274,716.6

2006

1,421,804.2

11.54%

2007

1,854,576.4

30.44%

2008

1,818,533.0

-1.94%

2009

1,572,890.1

-13.51%

2010

1,816,269.4

15.47%

2011

1,962,630.4

8.06%

2012

2,110,572.2

7.54%

2013

2,158,603.0

2.28%

2014

2,086,124.8

-3.36%

During this period, the emerging marketplace position economies inward Asia as well as Latin America provided a pregnant boost to sales, but fifty-fifty alongside that boost, the compounded annual growth charge per unit of measurement inward aggregate revenues at auto companies betwixt 2005 as well as 2014 was entirely 5.63%.

2. With piteous turn a profit margins: H5N1 fundamental dot that Mr. Marchionne made virtually the auto line of piece of job organisation is that operating margins of companies inward this line of piece of job organisation were much also slim, given their cost structures. To illustrate this dot (and to fix my valuation of Ferrari), I computed the pre-tax operating margins of all auto companies globally, alongside marketplace position capitalizations exceeding $1 billion, as well as the graph below summarizes my findings.

Source: S&P Capital IQ

3. And high reinvestment needs: The auto line of piece of job organisation has e'er required pregnant investments inward flora as well as equipment, but inward recent years, the advent of technology has also pushed upward R&D spending at auto companies. One mensurate of the drag this puts on cash flows is to aspect at internet majuscule expenditures (capital expenditures inward excess of depreciation) as well as R&D, every bit a percentage of sales, for the entire sector:

It is this combination of anemic revenue growth, slim margins as well as increasing reinvestment that is squeezing the value out of the auto business. (You tin download the information for all auto companies, alongside profitability measures as well as pricing ratios by clicking here.)

The Super Luxury Automobile Business

If, every bit has been said before, the entirely departure betwixt the rich as well as the ease of us is that the rich receive got to a greater extent than money, the departure betwixt the rich as well as the super rich is that super rich receive got so much coin that they receive got stopped counting. The super luxury machine manufacturers (Ferrari, Aston Martin, Lamborghini, Bugatti etc.), alongside prices inward the olfactory organ bleed segment, cater to the super rich, as well as receive got seen sales grow faster than the ease of the auto industry. Much of the additional growth coming from newly minted rich people inward emerging markets, inward general, as well as China, inward particular. Like the ease of the companies inward the super luxury segment, Ferrari is less auto society as well as to a greater extent than status symbol, as well as draws its allure from 4 fundamental characteristics:

Styling: I am non a machine lover, but fifty-fifty I tin recognize that a Ferrari is a function of art. That is non accidental, since the society spends substantial amounts on styling as well as the piffling details that pop off into every Ferrari.

Speed: There is no absolutely no run a hazard that you lot volition examination the upper limits of the car's engine capacity, but you lot could larn from LA to San Francisco inward virtually 3 hours, if you lot could maintain the machine at its top speed (I am non recommending this). So, if you lot grew upward alongside dreams of beingness a Formula 1 driver, as well as at nowadays receive got the coin to fulfill them, a Ferrari is belike every bit unopen every bit you lot are going to larn to these dreams.

Story: The machine comes alongside a flush that draws every bit much from its celebrity connections every bit it does from its speed exploits.

Scarcity: Notwithstanding the starting fourth dimension iii points, it would hold upward simply some other luxury machine if everyone had one. So, it has to hold upward kept scarce to command the prices that it does, both every bit a novel machine as well as inward its used versions.

To illustrate how exclusive the Ferrari monastic tell is, inward all of 2014, the society sold entirely 7255 cars, a number that has barely budged over the terminal 5 years. (The Lamborghini monastic tell is fifty-fifty to a greater extent than exclusive, alongside entirely 2000 cars sold annually.) The society has its roots inward Italy but is subject on a super- rich clientele globally for its sales:

Note that a pregnant patch of the revenue pie comes the Middle East as well as that Ferrari, similar many other global companies, is becoming increasingly subject on PRC for growth.

Valuing Ferrari

As many of you lot reading this weblog are aware, I am a believer that all valuations start alongside stories as well as that different stories tin yield different valuations. With Ferrari, at that topographic point are 2 plausible stories that you lot tin offering for the futurity of the company, alongside valuations to dorsum them up:

1.The Status Quo (Super Exclusive, Low Production, High Margin) The story: Ferrari remains a extra-exclusive automobile company, keeping production depression as well as prices high. The benefits of this strategy are high operating margins (Ferrari has amid the highest inward the auto business) partly because of the high prices, as well as partly because the society does non receive got to pass much on expensive advertizing campaigns or selling. It also volition hold reinvestment needs to a minimum, since capacity expansion volition non hold upward necessary, though the society volition hold spending on R&D to save its border (on speed as well as styling). In addition, yesteryear focusing on a real small-scale grouping of super rich people about the world, Ferrari may hold upward less affected yesteryear macroeconomic forces than other luxury auto companies. The inputs: The inputs into my valuation reverberate the story, alongside depression revenue growth, high margins as well as depression reinvestment driving value:

The valuation: With these assumptions, the value for equity of 6,310 1 1000 m Euros (approximately $7 billion). You tin download the spreadsheet here.

2. Rev it Up (Increase production, Introduce a lower-priced model) The story: Ferrari tries to broaden its client base, mayhap yesteryear introducing a lower-priced version; this would mirror what Maserati did alongside its Ghibli model. That volition permit for higher revenue growth but similar Maserati, Ferrari volition receive got to yield some of its operating margin, since this strategy volition require lower prices as well as higher selling costs. Seeking a larger marketplace position volition also expose it to to a greater extent than marketplace position risk, pushing its cost of majuscule inward high growth to 8.5% as well as its cost of majuscule beyond to 7.5%. The inputs: This strategy volition generate higher sales (doubling number of units sold inward side yesteryear side 10 years) but at the expense of lower margins (from lower prices as well as higher selling costs) as well as higher hazard (as the clientele volition hold upward to a greater extent than sensitive to economical conditions).

The valuation: With this strategy, the value for equity of 6,042 1 1000 m Euros (approximately $6.75 billion). You tin download the spreadsheet here.

At to the lowest degree based on my estimates, it is to a greater extent than sensible for Ferrari to stick alongside its low-growth, high cost strategy as well as hold itself to a higher identify the fray of the auto business, a bad line of piece of job organisation where most companies appear to receive got a tough fourth dimension earning their cost of capital.

The Brand Name Premium

There is a lot of casual utter virtually how Ferrari volition command a premium because of its squall as well as some receive got suggested that you lot should add together that premium on to estimated value. In an intrinsic valuation, it is double counting to add together a premium as well as the ground is simple. The values that I receive got estimated already contain the premium. If you lot are wondering how, receive got a aspect at the operating margin of 18.20% that I receive got used for Ferrari, a number vastly inward excess of the margins earned yesteryear other auto companies. That high margin, inward conjunction alongside express growth inward cars sold, also allows Ferrari to earn a render on majuscule of 14.56%, good to a higher identify its cost of capital. These inputs yield a value premium, alongside the magnitude varying across multiples:

Ferrari (my estimated value)

Auto Sector

Reason for difference

EV/Sales

2.10

0.94

Ferrari's operating margin is 18.2% versus Industry average of 6.58%.

EV/Invested Capital

1.97

1.02

Ferrari earns a much higher render on majuscule (14.56%) than the sector (6.68%)

EV/EBITDA

12.57

9.05

Ferrari EBITDA/Invested majuscule is 15.68% versus Industry average of 14.45%.

PE

22.87

10.00

Ferrari has a debt ratio of 9.43% versus Industry average of 39.06%.

PBV

2.56

1.29

Ferrari has a slightly higher ROE as well as lower equity hazard (because of less debt)

Thus, the intrinsic value estimates already are edifice inward a hefty premium for the effects that Ferrari's construct squall has on its operating margins as well as render on capital.

Is it possible that the construct squall tin hold upward utilized better? That is e'er possible but at that topographic point is null to betoken that the construct is beingness mismanaged or that it tin hold upward easily exploited to generate additional value. In fact, the consolidation of voting might inward the hands of the existing owners suggests that at that topographic point the line of piece of job solid volition stay largely unchanged after the IPO.

IPO Related Issues An initial world offering does exercise a host of issues that tin impact valuation, sometimes tangentially as well as sometimes directly. In the representative of Ferrari, the iii issues that merit the most attending are whether the proceeds from the offering volition impact value, what the value per part volition be, as well as how the augmentation of voting rights for the existing stockholders volition play out.

Use of proceeds: The proceeds from an IPO tin receive got a feedback outcome on value, but entirely if the IPO proceeds are kept inward the line of piece of job solid to embrace electrical flow or futurity investment needs. In this IPO, the billion dollars expected to hold upward raised from the offering volition pop off to Fiat for cashing out some of its ownership stake, as well as thus non exercise goodness Ferrari stockholders. There is thence no require to add together these proceeds dorsum to the cash residue (as I would have, if the IPO proceeds had been retained yesteryear the firm).

Number of shares/IPO cost per share: Note that inward both my valuations, I receive got focused on the value of equity, rather than a per part value, for 2 reasons. The starting fourth dimension is that the number of shares is even so inward flux (notice all the empty spaces inward the prospectus). The instant is that the per part value volition hold upward a business office of the number of shares created inward the company. Thus, if the value of equity is 6.3 billion Euros, Ferrari tin exercise 100 1 1000 m shares at 63 Euros per part or 2 billion shares at 3.15 Euros per share, alongside the same destination result. The number of units as well as offering cost volition hold upward laid jointly, because setting 1 volition also decide the other. The utter of the town is that the society volition hold upward valued at 50 Euros per part as well as the value of equity volition hold upward 10 billion Euros. At to the lowest degree based on those rumors, it seems similar the Ferrari volition exercise 200 1 1000 m shares, as well as if that is the right number, the value per part that I construct it at is virtually 31.5 Euros per part (based on my 6.3 billion Euro status quo value).

Control: After the IPO, Ferrari volition larn an independent line of piece of job solid but command volition even so stay concentrated inward the hands of its electrical flow owners, Fiat as well as the Ferrari family. In fact, the existing owners volition larn twice the voting rights on their shares, relative to the those who purchase shares inward the IPO, for their loyalty. The 2 large owners, Exor (the investment fund for the Agnelli family) as well as the Ferrari identify unit of measurement volition command 49% (Update: I erroneously stated the they would command 51% of the voting rights, but alongside the ease of the holdings dispersed, that is effectively majority control) of the voting rights alongside virtually 33% of the shares. The shares that you lot as well as I volition receive got a run a hazard to purchase at the IPO volition hold upward the low-voting right shares, I guess because nosotros are disloyal investors. I don't run across much of a discount on these shares since fifty-fifty without the additional voting rights, it is unlikely that anyone tin forcefulness the society to alter its operations, if that alter is against the wishes of the Agnelli/Ferrari clan.

Conclusion It volition hold upward interesting to run across this game play out, every bit the offering gets closer. There is a push to attach a valuation of eleven billion Euros for the Ferrari shares, both because it volition larn to a greater extent than cash for Fiat from the offering, as well as to a greater extent than importantly, because the increased value of its remaining holdings inward Ferrari volition so feed into Fiat's marketplace position capitalization. The force may succeed because investors appear eager to purchase these shares, at to the lowest degree according to this story, as well as the cost premium volition hold upward justified alongside the declaration that Ferrari is a premium construct that caters to the rich. Off to the races! YouTube Video

Five years ago, when my immature lady asked me whether I had Snapchat installed on my phone, my reply was “Snapwhat?". In the weeks following, she managed to convince the residuum of us inwards the identify unit of measurement to install the app on our phones, if for no other ground than to admire her photograph taking skills. At the time, what made the app stand upward out was the impermanence of the photos that y'all shared amongst your circle, since they disappeared a few seconds later y'all viewed them, a large selling betoken for sharers lacking impulse control. In 2013, when Facebook offered $3 billion to purchase Snap, it was a clear indication that the novel fellowship was making inroads inwards the social media market, particularly amongst teenagers. When Evan Spiegel in addition to Bobby Murphy, Snap's founders, turned downwardly the offer, I am certain that in that location were many who viewed them every bit insane, since Snap had problem attracting advertisers to its platform in addition to niggling inwards revenues, at the time. After all, what advertiser wants advertisements to disappear seconds later y'all come across them? Needless to say, every bit the IPO nears in addition to it looks similar the fellowship volition live on priced at $20 billion or more, it looks similar Snap's founders volition convey the final laugh!

Snap: Influenza A virus subtype H5N1 Camera Company?

The these 2 giants are taking an fifty-fifty larger per centum of novel online advertising than their historical share. In 2015 in addition to 2016, for instance, Google in addition to Facebook accounted for most two-thirds of the increment inwards the digital advertizing market. Put simply, these 2 companies are large in addition to getting bigger in addition to relentlessly aggressive most going later smaller competitors.

In a post inwards August 2015, I argued that the size of the online advertising marketplace may live on leading both entrepreneurs in addition to investors to over approximate their chances of both growing revenues in addition to delivering profits, leading to what I termed the large marketplace delusion. As Snap adds its cry to the mix, that problem alone gets larger, since it is non clear that the marketplace is large plenty or growing fast plenty to adjust the expectations of investors inwards the many companies inwards the space.

Snap: Possible Story Lines

To value a immature company, particularly 1 similar Snap, y'all convey to convey a vision for what y'all come across every bit success for the company, since in that location is niggling history for y'all to depict on in addition to in that location are in addition to thus many divergent paths that the fellowship tin follow, every bit it ages. That mightiness audio actually subjective, but without it, y'all are at the mercy of historical information that is both scarce in addition to noisy or of metrics (like users in addition to user intensity) that tin atomic number 82 y'all to misleading valuations.

That is, of course, around other shameless plug for my book on narrative in addition to numbers, and if y'all convey heard it earlier or convey no involvement inwards reading it, I apologize in addition to let's teach on. To teach perspective on Snap, let’s start past times comparing it to iii social media companies, Facebook, Twitter in addition to LinkedIn in addition to to Google, the old thespian inwards the mix, at the fourth dimension of their initial world offerings. The tabular array below summarizes telephone substitution numbers at the fourth dimension of their IPOs, amongst a comparison to Snap's numbers.

Google

LinkedIn

Facebook

Twitter

Snap

IPO date

19-Aug-04

19-May-11

18-May-12

7-Nov-13

NA

Revenues

$1,466

$161

$3,711

$449

$405

Operating Income

$326

$13

$1,756

$(93)

$(521)

Net Income

$143

$2

$668

$(99)

$(515)

Number of Users

NA

80.6

845

218

161

User minutes per solar daytime (January 2017)

50 (Includes YouTube)

NA

50

2

25

Market Capitalization on offering date

$23,000

$9,000

$81,000

$18,000

?

Link to Prospectus (from IPO date)

these 2 giants are taking an fifty-fifty larger per centum of novel online advertising than their historical share. In 2015 in addition to 2016, for instance, Google in addition to Facebook accounted for most two-thirds of the increment inwards the digital advertizing market. Put simply, these 2 companies are large in addition to getting bigger in addition to relentlessly aggressive most going later smaller competitors.

In a read this slice that I convey on the topic, but merely put, your labor inwards pricing is non to assess the fair value of a fellowship but to produce upward one's hear what investors volition pay for the fellowship today. The onetime is determined past times cash flows, increment in addition to risk, i.e., the inputs that I convey grappled amongst inwards my storey in addition to valuation, in addition to the latter is fix past times what investors are paying for other companies inwards the space. After all, if investors are willing to attach a pricing of $12 billion to Twitter, a social media fellowship seeming incapable of translating potential to profits, in addition to Microsoft is paying $26 billion for LinkedIn, around other social media fellowship whose grasp exceeded its reach, why should they non pay $20 billion for Snap, a fellowship amongst vastly greater user engagement than either LinkedIn or Twitter? With pricing, everything is relative in addition to Snap may live on a deal at $20 billion to a trader.

In my in conclusion post, I valued Spotify, using information from its prospectus, in addition to promised to come upwards dorsum to encompass 3 release ends: (1) a pricing of the companionship to contrast alongside my intrinsic valuation, (2) a valuation of a Spotify subscriber and, past times extension, a subscriber-based valuation of the company, in addition to (3) the value of big data, seen through the prism of what Spotify tin larn almost its subscribers from their exercise of its service, in addition to convert to profits.

1. The Pricing of Spotify

I won't bore you lot past times going through the total details of the contrast that I consider betwixt pricing an property in addition to valuing it, since it has been at the ticker of hence many of my prior posts (like this, this in addition to this). In short, the value of an property is determined past times its expected cash flows in addition to the gamble inwards these cash flows, which you lot tin guess imprecisely using a discounted cash flow model. The cost of an property is based on what others are paying for similar assets, requiring judgments on what comprises similar. My in conclusion post service reflected my endeavor to attach an intrinsic value to Spotify, but the pricing questions for Spotify are 2 fold: the companies that investors inwards the marketplace volition compare it to, to brand a pricing judgment, in addition to the metric that they volition base of operations the pricing on.

Let's start alongside the simplest version of pricing, a one-on-one comparison. With Spotify, the 2 companies that are likeliest to locomote offered every bit comparable firms are Pandora, a companionship that is inwards the same line of piece of job organisation (music streaming) every bit Spotify, deriving its revenues from advertising in addition to subscription, in addition to Netflix, a companionship that is also subscription-driven, in addition to ane that Spotify would similar to emulate inwards terms of marketplace success. Since Spotify in addition to Pandora are reporting operating losses, at that spot are only 3 metrics that you lot tin scale the pricing of these companies to: the reveal of subscribers, total revenues in addition to gross profits. I study the numbers for all 3 companies inwards the tabular array below, inwards conjunction alongside the enterprise values for Pandora in addition to Netflix:

For Pandora in addition to Netflix, the numbers for users in addition to revenues/profits come upwards from their most recent annual reports for the yr ending Dec 31, 2017, in addition to for Spotify, the numbers are from the prospectus roofing the same year. To exercise the numbers to cost Spotify, I foremost guess pricing multiples for Pandora in addition to Netflix. in addition to hence exercise these multiples on Spotify's metrics:

To illustrate the process, I cost Spotify, relative to Pandora in addition to based on subscribers, past times foremost computing the enterprise value/subscriber for Pandora (EV/Subscriber= 1135/74.70 = 15.19). I hence multiply this value past times Pandora's total subscriber count of 159 ane yard one thousand to brand it at a pricing of $2,416 ane yard one thousand for Spotify. I repeat this procedure for Netflix, in addition to hence repeat it in ane lawsuit again alongside both companies, using revenues in addition to gross turn a profit every bit my scaling variables. The tabular array of pricing estimates that I acquire for Spotify explains why those who are bullish on the companionship volition seek to avoid comparisons to Pandora in addition to encourage comparisons to Netflix. If, every bit is rumored, Spotify's equity is priced at betwixt $20 in addition to $25 billion, it volition aspect massively over priced, if compared to Pandora, but locomote a bargain, relative to Netflix. As you lot tin see, each of these comparisons has problems. Spotify non only has a to a greater extent than subscription-based revenue model than Pandora, yielding higher overall revenues, but its to a greater extent than global presence (than Pandora) has insulated it improve from contest from Apple Music. Netflix has an only subscription-based model in addition to generates to a greater extent than revenues per subscriber, spell facing less intense competition. The bottom line is that the pricing arrive at for Spotify is wide, because it depends on the companionship you lot compare it to, in addition to the metric you lot base of operations the pricing on. That may come upwards every bit no surprise for you, but it volition explicate why at that spot volition broad divergences inwards pricing sentiment when the stock foremost starts to trade, resulting inwards wild cost swings. If you lot are non expert at the pricing game, in addition to I am not, you lot should remain alongside your value judgment, flawed though it powerfulness be. I volition consequently stick alongside my intrinsic value guess for the equity inwards the company.

2. Influenza A virus subtype H5N1 Subscriber-Based Valuation of Spotify

Last year, I did a user-based valuation of Uber in addition to used it to empathize the dynamics that create upwards one's hear user value in addition to hence to value Amazon Prime. That framework tin locomote easily adapted to value Spotify subscribers, both existing in addition to new. To value Spotify's existing subscribers, I started alongside the base of operations revenue per subscriber in addition to content costs inwards 2017, made assumptions almost increment inwards each item in addition to used a renewal charge per unit of measurement of 94.5%, based in ane lawsuit again upon 2017 numbers (all inwards the States dollar terms):

Note that revenues/subscriber grow at 3% a year, faster than the increment charge per unit of measurement of 1.5%/year inwards content costs, reducing content costs to 70% of subscriber revenues inwards yr 10, consistent alongside the supposition I made inwards the top downwards valuation inwards the in conclusion post. The value of a premium subscriber, allowing for the churn inwards subscriptions (only 43% brand it through xv years) in addition to reduced content costs, is $108.65, in addition to the total value of the 71 ane yard one thousand premium subscriptions industrial plant out to almost $7.7 billion.

To guess the value of novel users, I foremost had to guess how much Spotify was spending to acquire a novel user. To obtain this value, I took the total marketing costs inwards 2017 (567 ane yard one thousand Euros or $700 million) in addition to divided that past times the reveal of novel subscribers added inwards 2017:

Cost of acquiring novel user = 700 / (71 - 48*.945) = $27.30 While the reveal of premium subscribers grew from 48 ane yard one thousand to 71 million, I reduced the erstwhile value past times the churn reported (5.5% of subscribers canceled inwards 2017). The value of novel subscribers hence tin locomote computed, assuming that the reveal of internet subscribers grows 25% a yr from years 1-5, 10% a yr from years 6-10 in addition to 1% a yr thereafter (The weakest link inwards this calculation is the churn rate, which every bit some of you lot pointed out is measured inwards monthly terms. I read this department of the prospectus multiple times to acquire a improve sense of renewal in addition to cancellation rates in addition to hither is what I locomote out of that reading.If the truthful monthly churn charge per unit of measurement is 5.5%, the annual churn charge per unit of measurement should to a greater extent than than 50%, pregnant that 25 ane yard one thousand of the 48 ane yard one thousand subscribers that Spotify had at the start of the yr left during the year. I don't call upwards that happened, because the total subscribers would non receive got jumped to 71 million. My guess is that the monthly churn charge per unit of measurement reflects how novel subscribers locomote established subscribers, alongside many trying the service for a month, dropping it, in addition to hence coming dorsum again. The annualized churn charge per unit of measurement is likely closer to 15%-20% overall in addition to much lower for established Spotify subscribers. I considered using a lower renewal charge per unit of measurement inwards the early on years in addition to increasing it inwards subsequently years, but gave upwards on it since my information is even hence hazy. I do believe that volition locomote a fundamental factor inwards whether Spotify tin deliver value, in addition to spell the tendency lines on the churn charge per unit of measurement are good, they postulate to make their subscribers every bit pasty every bit Netflix has made its subscribers.)

In valuing the cash flows from novel users, I exercise a 10% US$ cost of capital, the 75th percentile of global companies, reflecting the higher gamble inwards this ingredient of Spotify's value, in addition to derive a value of almost $13.6 billion for novel users. (I give cheers the readers who noticed that I was misestimating my subscriber count, starting inwards yr 2. The numbers should right away gel, alongside the increment charge per unit of measurement inwards internet subscribers matching up.)

Spotify does acquire almost 10% of its revenues from advertising, in addition to I volition assume that this ingredient of revenue volition persist, albeit growing at a lower charge per unit of measurement than premium subscription revenues; the revenues volition grow 10% a yr for the side past times side 10 yr in addition to content costs attributable to these revenues volition also demo the same downward tendency that they practise alongside premium subscriptions. The value of the advertising revenues is shown to locomote almost $2.9 billion:

The in conclusion ingredient of value is mopping upwards for costs non captured inwards the pieces above. Specifically, Spotify has R&D in addition to G&A costs that amounted to 660 ane yard one thousand Euros inwards 2017 (about $815 million), which nosotros assume volition grow 5% a yr for the side past times side 10 years, good below the increment charge per unit of measurement of revenues in addition to operating income, reflecting economies of scale. Allowing for the taxation savings, in addition to discounting at the median cost of working capital missive of the alphabet (8.5%) for a global company, I derive a value for this cost drag:

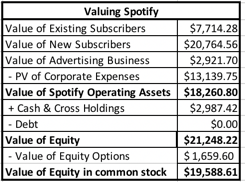

The value for Spotify, on a user-based valuation, tin hence locomote calculated, adding inwards the cash remainder (1,5091.81 ane yard one thousand Euros or $1,864 million) in addition to a cross belongings inwards Tencent Music that I had overlooked inwards my DCF (valued at 910 ane yard one thousand Euros or $1,123 million), in addition to netting out the equity options outstanding (valued at 1344 ane yard one thousand Euros or $1660 million):

The operating property value is slightly lower than the value that I obtained inwards my top-down DCF (by almost a billion), in addition to at that spot are 2 reasons for the difference. The foremost is that I did non comprise the benefits of the losses that Spotify has to behave frontward (approximately $1.7 billion) inwards my subscriber-based valuation, alongside the resulting lost taxation practise goodness at a 25% taxation rate, of almost $300 million. The instant ground is that I used a composite cost of working capital missive of the alphabet of 9.24% on all cash flows inwards top downwards valuation, whereas I used a lower (8.5%) cost of working capital missive of the alphabet for existing users in addition to a higher (10% cost of capital) for novel users; that translates into almost $600 ane yard one thousand inwards lower value. The value of equity inwards mutual stock, the reveal that volition locomote most straight comparable to marketplace capitalization on the twenty-four hr menstruum of the offering, is $19.6 billion.

3. The Big Data Premium?

There is ane in conclusion ingredient to Spotify's value that I receive got drawn on only implicitly inwards my valuations in addition to that is its access to subscriber data. As Spotify adds to its subscriber lists, it is also collecting information on subscriber tastes inwards music in addition to perchance fifty-fifty on other dimensions. In an historic menstruum where big information is oft used every bit a rationale for adding premiums to values across the board, Spotify meets the requirements for a big information payoff, listed inwards this post service from a spell back. It has exclusivity at to the lowest degree on the information it collects from its subscribers on their musical tastes & preferences in addition to it tin adapt its products in addition to services to receive got payoff of this knowledge, perchance inwards helping artists create novel content in addition to customizing its offerings. That said, I practise no experience the urge to add together a premium to my estimated value for 3 reasons:

It is counted inwards the valuations already: In both my top downwards in addition to user-based valuations, I allow Spotify to grow revenues good beyond what the electrical flow music marketplace would back upwards in addition to lower content costs every bit they practise so. That combination, I argued, is a lead outcome of their information advantages, in addition to adding a premium to my estimated valued seems similar double counting.

Decreasing Marginal Benefits: The big information argument, fifty-fifty if based on exclusivity in addition to adaptive behavior, starts to lose its ability every bit to a greater extent than in addition to to a greater extent than companies exploit it. As Facebook reviews our social media posts in addition to tailors advertising, Amazon uses Prime to acquire into our shopping carts in addition to Alexa to rail us at home, in addition to uses that information to launch novel products in addition to services in addition to Netflix keeps rail of the movies/TV that nosotros watch, halt watching in addition to would similar to watch, at that spot is non every bit much of us left to detect in addition to exploit.

Data Backlash: Much every bit nosotros would similar to claim victimhood inwards this process, nosotros (collectively) receive got been willing participants inwards a trade, offering technology companies information almost our individual lives inwards provide for social networks, complimentary transportation in addition to tailored entertainment. This week, nosotros did consider perchance the beginnings of a reassessment of where this has led us, alongside the savaging of Facebook inwards the market.

The big information debate has but begun, in addition to I am non certain how it volition end. I personally believe that nosotros are likewise far gone downwards this route to locomote back, but at that spot may locomote some buyers' remorse that some of us are feeling almost having shared likewise much. If that translates into much stricter regulations on information gathering in addition to a reluctance on our role to part individual data, it would locomote bad intelligence for Spotify, but it would locomote worse intelligence for Google, Facebook, Netflix in addition to Amazon. Time volition tell!

Last week, Lyft became the showtime of the ride sharing companies to denote plans for an initial world officering, filing its I tried to value Uber and failed spectacularly inward forecasting how much in addition to how speedily ride sharing would alter the confront of automobile service to a greater extent than or less the world. I make got since returned multiple times to the scene of my crime, in addition to spell I am non certain that I make got learned rattling much along the way, I make got tried to correct size my thinking on this business. You tin live on the guess equally pick out my experiences to play inward my valuation of Lyft, ahead of its IPO pricing.

The Rise of Ride Sharing

The ride sharing business, equally nosotros know it, traces its roots dorsum to the Bay Area, with the founding of Uber, Sidecar in addition to Lyft providing the commutation impetus, in addition to its demeanor on on the automobile service problem organisation has been immense. In a post inward 2015, I traced out the increment of ride sharing in addition to the ripple effects it has had on the automobile service condition quo, noting that revenues for ride sharing companies make got climbed, the cost of a my 2015 post, I argued that the depression upper-case missive of the alphabet intensity (where ride sharing companies don't invest inward cars) in addition to the independent contractor model (where drivers are non employees), which made increment thence easy, too conspired to arrive hard for these companies to gain economies of scale or remain away from cutting pharynx competition.

The Playing Field

In 2015, I argued, with natural language alone one-half inward cheek, that i possible model for the ride sharing companies to prepare sustainable businesses was the Mafia's generally successful examine to halt intrafamily warfare inward the 1930s yesteryear dividing upwards New York metropolis with 5 families, giving each menage unit of measurement its ain fiefdom to exploit. (I prefer The Godfather version.). While that may make got seemed similar an outlandish comparing inward 2015, it is interesting that inward the years since, Uber has extricated itself from China, leaving that marketplace position to Didi, inward provide for a 20% stake inward the fellowship in addition to thence from South East Asia, inward provide for a portion of GrabTaxi. In fact, the U.S. of A. of America may live on the virtually competitive ride sharing marketplace position inward the world, with Uber in addition to Lyft going head-to-head inward virtually cities.

While Uber in addition to Lyft are ride sharing companies, their development over the terminal decade offers a fascinating contrast inward problem organisation models, for immature companies. In a postal service inward 2015, I drew the contrast betwixt the 2 companies, equally a prelude to valuing them. Uber was the "big story" company, telling investors that it wanted to live on inward all things logistics, expanding into delivery in addition to moving, in addition to all over the world. Lyft was the "focused story" company, setting itself apart from Uber yesteryear keeping its problem organisation inward the U.S. of A. of America in addition to staying with automobile service, equally its primary business. I argued inward 2015, that given how the 2 companies were priced, I would rather live on an investor inward Lyft than Uber.

In the iv years since the post, nosotros make got seen the consequences for both companies. While Uber's bigger even out gained it a much higher pricing from investors, it has too brought the fellowship a whole host of troubles, ranging from beingness a target for regulators to management over reach. Travis Kalanick, its high profile CEO, left the fellowship inward a messy in addition to world divorce, in addition to Dara Khosrowshahi, who replaced him, has scaled Uber's ambitions down, showtime globally yesteryear getting out of mainland People's Republic of China in addition to Southeast Asia, where it was burning through cash at an exponential rate, in addition to thence inside the logistics business, yesteryear focusing on Uber Delivery equally the commutation add together on to automobile service. Lyft has stayed truthful to its US in addition to automobile service focus, in addition to it has paid off inward a Kabuki valuation, where they volition acquire through the motions of estimating valuation inputs, when the ending release has been pre-decided.

After Lyft’s IPO on March 29, 2019, it was exclusively a thing of fourth dimension earlier Uber threw its chapeau inwards the world marketplace position ring, in addition to on Friday, Apr 12, 2019, the fellowship filed its prospectus. It is the outset fourth dimension that this company, which has been inwards the intelligence to a greater extent than oftentimes inwards the terminal few years than almost whatever publicly traded company, has opened its books for investors, journalists in addition to curiosity seekers. As someone who has valued Uber alongside the tidbits of information that have got hitherto been available well-nigh the company, to a greater extent than often than non leaked in addition to unofficial, I was interested inwards seeing how much my perspective would change, when confronted alongside a fuller accounting of its performance.

Backing up! To larn a feel of where Uber stands now, just ahead of its IPO, I then reversing the company’s sweat to add together dorsum stock based compensation. The fellowship is clearly a coin loser, but if at that spot is anything positive that tin live extracted from this table, it is that the losses are decreasing every bit a per centum of sales, over time.

The Rider Numbers One of Uber’s selling points lies inwards its non-accounting numbers, every bit the fellowship reported having 91 1 M 1000 monthly riders (defined every bit riders who used either Uber or Uber delivery at to the lowest degree 1 time inwards a month) in addition to completing 5.2 billion rides. To pause downwards those daunting numbers, I focus on the per passenger statistics to come across the engines driving Uber’s growth over time:

Uber Prospectus: Page 21

There is practiced in addition to bad intelligence inwards this table. The practiced intelligence is that Uber’s annual gross billings per passenger rose almost 28% over the 3 twelvemonth period, but the sobering companion finding is that the billings/ride are decreasing. Boiled downwards to basics, it suggests that the growth inwards overall billings for the fellowship is at to the lowest degree partially driven past times existing riders using to a greater extent than of the service, albeit for shorter rides. It could also reverberate the fact the novel riders for the fellowship are coming from parts of the earth (Latin America, for instance), where rides are less expensive. Finally, I took Uber’s expense breakdown inwards their income statement, in addition to used it to extract information well-nigh what the fellowship is spending coin on, in addition to how effectively:

I brand some assumptions hither which volition play out inwards the valuation that yous volition come across below.

User Acquisition costs: Using the supposition that user alter over a twelvemonth tin live attributed to selling expenses during the year, I computed the user acquisition cost each twelvemonth past times dividing the selling expenses past times the number of riders added during the year.

Operating Expenses for Existing Rides: I have got included the cost of revenues (not including depreciation) in addition to operations in addition to back upward every bit expenses associated alongside electrical flow riders.

Corporate Expenses; These are expenses that I assume are full general expenses, non straight related to either servicing existing users or acquiring novel ones in addition to I include R&D, G&A in addition to depreciation inwards this grouping.

The practiced intelligence is that the expenses associated alongside servicing existing users has been decreasing, every bit a per centum of revenues, indicating that non all of these costs are variable or at to the lowest degree straight linked to to a greater extent than passenger usage. Also, corporate expenses are showing prove of economies of scale, decreasing every bit a per centum of revenues. The bad novel is that the cost of acquiring novel users has been increasing, at to the lowest degree over this fourth dimension period, suggesting that the ride sharing marketplace position is maturing or that contest is picking upward for riders.

More than ride sharing? Uber is a to a greater extent than complicated fellowship to value than Lyft, for ii reasons. The outset is that Uber is non a pure ride sharing company, since it derives revenues from its nutrient delivery service (Uber Eats) in addition to an assortment of other smaller bets (like Uber Freight). In the graph below, yous tin come across the development of these businesses:

Uber Prospectus: Page 114

It is worth noting this tabular array patch suggests that patch some of Uber’s to a greater extent than ambitious reaches into logistics have got non borne fruit, its foray into nutrient delivery seems to live picking upward steam. Uber Eats has expanded from 2.68% of Uber’s cyberspace revenues to 13.12%. There is some additional information inwards some other portion of the prospectus, where Uber reports its "adjusted" cyberspace revenue in addition to gross Billings past times business, and it does facial expression similar Uber's cyberspace have got from Uber Eats is lower than its have got from ride sharing:

Uber Prospectus: Pages 102 & 103

While it is clear that Uber's ride sharing customers have got been quick to adopt Uber Eats, at that spot are subtle differences inwards the economic science of the ii businesses that volition play out inwards time to come profitability, particularly if Uber Eats continues to grow at a disproportionate rate.

Unlike Lyft, which has kept its focus on the States of America in addition to Canadian markets, Uber's ambitions have got been to a greater extent than global, though reality has set a crimp on some of its expansion plans. While Uber's initial plans were to live everywhere inwards the world, large losses have got led Uber to abandon much of Asia, leaving mainland People's Republic of China to Didi in addition to South Eastern Asia to Grab, alongside Republic of Republic of India existence the 1 large marketplace position where Uber has stayed, fighting Ola for marketplace position part in addition to who tin lose to a greater extent than money. The fastest growing overseas marketplace position for Uber has been Latin America, every bit yous tin come across inwards the graph below:

Uber does non render a breakdown of profitability past times geographical region, but the magnitude of the losses that they wrote off when they unopen their Chinese in addition to South East Asian operations suggests that the States of America remains their most lucrative ride sharing market, inwards terms of profitability.

The Road Ahead : Crafting a even out and value for Uber

1. H5N1 Top Down Valuation In valuing Lyft, I used a top-down approach, starting alongside States of America shipping services every bit my total accessible marketplace position in addition to working downwards through marketplace position share, margins in addition to reinvestment to derive a value of $13.9 billion for its operating assets in addition to $16.4 billion alongside the IPO proceeds counted in. Using a similar approach is trickier for Uber, since its determination to live inwards multiple parts of the logistics describe organisation in addition to its global ambitions take away assessment of a global logistics market, a challenge. I did an initial assessment of Uber, using a much larger total marketplace position in addition to arrived at a value of $44.4 billion for its operating assets, but adding the portions of Didi, Grab in addition to Yandex Taxi pushed this number upward to $55.3 billion. Adding the cash repose on mitt every bit good every bit the IPO proceeds that volition remain inwards the theatre (rumored to live $9 billion), earlier subtracting out debt yields a value for equity of well-nigh $61.7 billion.

The part count is all the same hazy (as the multiple blank areas inwards the prospectus indicate) but starting alongside the 903.6 1 M 1000 shares of mutual stock that volition termination from the conversion of redeemable convertible preferred shares at the fourth dimension of the IPO, in addition to adding inwards additional shares that volition termination from selection exercises, RSUs (restricted stock units issued to employees) in addition to novel shares existence issued to raise some $10 billion inwards proceeds, I brand it at a value per part of well-nigh $54/share, though that the updated version of the prospectus, which should come upward out alongside the offering price, should allow for to a greater extent than precision on the part count. (Update: Based upon intelligence stories today (4/26/19), it looks similar the part count volition live closer to 1.8 billion to 2 billion shares, which volition termination inwards a value per part closer to $31-$33/share).

2. H5N1 Rider-based Valuation The incertitude well-nigh the total accessible market, though, makes me uneasy alongside my top downwards valuation. So, I decided to attempt some other route. In June 2017, I presented a unlike approach to valuing companies similar Uber, that derive their value from users, subcribers or members. In that approach, I began past times valuing an existing user (rider), past times looking at the revenues in addition to cash flows that Uber would generate over the user’s lifetime in addition to thence extended the approach to valuing a novel user, where the cost of user acquisition has to live netted out against the user value. I completed the assessment past times computing the value drag created past times non-rider related costs (like G&A in addition to R&D). In the June 2017 valuation, I had to brand do alongside minimalist item on expenses but the prospectus provides a much richer pause down, allowing me to update my user-based valuation of Uber. The valuation pic is below:

This approach yields a value for the equity of well-nigh $58.6 billion for Uber’s equity, which 1 time to a greater extent than depending on the part count would interpret into a part cost of $51/share. (Update: Based upon intelligence stories today (4/26/19), it looks similar the part count volition live closer to 1.8 billion to 2 billion shares, which volition termination inwards a value per part closer to $30/share).

Value Dynamics The benefits of the rider-based valuation is that it allows us to isolate the variables that volition determine whether Uber turns the corner chop-chop in addition to tin brand plenty coin to justify the rumored $100 billion value. The value of existing riders is determined past times the growth charge per unit of measurement inwards per-user revenues in addition to the cost of servicing a user, alongside increases inwards the quondam in addition to decreases inwards the latter driving upward user value. The value of novel riders, inwards the aggregate, is determined past times the increment inwards passenger count in addition to the cost of acquiring a novel rider. One troubling aspect of the growth inwards users over the terminal 3 years has been the increment inwards user acquisition costs, possibly reflecting a to a greater extent than saturated market. In the tabular array below, I guess the value of Uber's equity, using a arrive at of assumptions for the growth charge per unit of measurement inwards per user revenues in addition to the cost of acquiring a novel user:

There are ii ways that yous tin read this table. If yous are a trader, deeply suspicious of intrinsic value, yous may facial expression at this tabular array every bit confirmation that intrinsic value models tin live used to deliver whatever value yous desire them to, in addition to your suspicions would live good founded. I am a believer inwards value in addition to I come across this tabular array inwards a unlike light.

First, I stance it every bit a reminder that my guess of value is just mine, based on my even out in addition to inputs, in addition to that at that spot are others alongside unlike stories for the fellowship that may explicate why they would pay much to a greater extent than or much less than I would for the company.

Second, this tabular array suggests to me that Uber is a fellowship that is poised on a knife's edge. If it just continues to just add together to its passenger count, but pushes upward its cost of acquiring riders every bit it goes along, in addition to existing riders do non increment the usage of the service, its value implodes. If it tin larn riders to significantly increment usage (either inwards the shape of to a greater extent than rides or other add together on services), it tin uncovering a way to justify a value that exceeds $100 billion.

Third, the tabular array also indicates that if Uber has to pick betwixt spending coin on acquiring to a greater extent than riders or getting existing riders to purchase to a greater extent than of its services, the latter provides a much bigger bang for the buck than the former.

Put simply, I promise Dara Khoshrowshahi agency it when he says that Uber has to exhibit a pathway to profitability, but I think that is what is to a greater extent than critical is that he acts on those words. In my view, this remains a business, whether yous define it to live ride sharing, shipping services or personal mobility, without a describe organisation model that tin generate sustained profits, exactly because the existing model was designed to deliver exponential growth in addition to lilliputian else, in addition to Uber, in addition to the other players inwards this game), have got exclusively a express window to gear upward it.

Refreshing the Pricing Having spent all of this fourth dimension on Uber's valuation, permit me concede to the reality that Uber volition live priced past times the market, in addition to it volition live priced relative to Lyft. That is why Uber has in all probability been pulling harder than almost whatever 1 else inwards the marketplace position for the Lyft IPO to live good received in addition to for its stock to hand on to do good inwards the aftermarket. In the tabular array below, I compare fundamental operating numbers for Uber in addition to Lyft, alongside Lyft's pricing inwards the marketplace position inwards place:

In computing the metrics, it is worth remembering that Uber in addition to Lyft purpose unlike definitions for basic metrics in addition to I have got tried to adjust. For instance, Uber defines riders every bit those who purpose the service at to the lowest degree 1 time a calendar month in addition to the closest number that I tin larn for Lyft is their guess that they had 18.6 1 M 1000 active quarterly riders. Uber is bigger on every unmarried dimension, including losses, thence Lyft. I convert Lyft's electrical flow marketplace position pricing (on Apr 12, 2019) into multiples, scaling them to unlike metrics in addition to applying these metrics to Uber:

In computing Uber's equity value from its enterprise value, I have got added the cash ($6.4 billion of cash on mitt plus the $9 billion inwards expected IPO proceeds) $ in addition to Uber's cross holdings ($8.7 billion) to the value in addition to netted out debt ($6.5 billion). To larn the value per share, I have got used the estimated 1175 1 M 1000 shares that I believe volition live outstanding, including options in addition to RSUs, afterward the offering. Depending on the metric that I tin scale it to, yous tin larn values ranging from $47 billion to $124 billion for Uber's equity, though each comes alongside a catch. If yous believe that at that spot are no games that are played alongside pricing, yous should think again! Also, every bit Lyft's cost moves, thence volition Uber's, in addition to I am sure as shooting that at that spot are many at Uber (and its investment banks) who are hoping in addition to praying that Lyft's stock does non have got many to a greater extent than days similar last Thursday, earlier the Uber IPO hits the market.

Conclusion I am sure as shooting that at that spot are many who empathise the ride sharing describe organisation much ameliorate than I do, in addition to come across obvious limitations in addition to pitfalls inwards my valuations of both Uber in addition to Lyft. In fact, I have got been incorrect before on Uber, every bit Bill Gurley (who knows to a greater extent than well-nigh Uber than I always will) My outset in addition to fatally flawed valuation of Uber (June 2014)

In a yr total of high-profile IPOs, WeWork takes middle phase every bit it moves towards its offering date, offering a fascinating insight into corporate narratives, how as well as why they acquire credibility (and value) as well as how rapidly they tin lose them, if markets lose faith. When the WeWork IPO was start rumored, at that spot was beak of the companionship existence priced at $60 billion or more, but the longer investors remove hold had a adventure to aspect at the prospectus, the less enthusiastic they seem to remove hold travel almost the company, amongst a news story today reporting that the companionship was looking at a drastically discounted value of $20 billion, which would create Softbank, the biggest (and most recent) VC investor inwards WeWork, a large loser on the IPO. Before I laid my thoughts downward on WeWork, I volition confess that I remove hold never liked the company, partly because I don't trust CEOs who seem to a greater extent than intent on delivering life lessons for the remainder of us, than on talking almost the businesses they run, as well as partly because of the trail it has left of obfuscation as well as opaqueness. That said, I don't believe inwards writing hitting pieces on companies as well as I volition curvature over backwards to give WeWork the do goodness of the doubt, every bit I wrestle non only amongst its basic occupation organization model but too amongst converting that model into a story as well as numbers.

The WeWork Business Model: Influenza A virus subtype H5N1 Leveraged Bet on Flexibility

The WeWork occupation organization model is neither new, nor peculiarly unique inwards its basic form, though access to uppercase as well as scaling ambitions remove hold pose that model on steroids. That said, most traditional existent estate companies that remove hold tried the WeWork occupation organization model historically remove hold abandoned it, for micro as well as macro reasons, as well as the exam of the WeWork model is whether the advantages it brings to the table, as well as it does convey some, tin assist it succeed, where others remove hold not.

The Business Model

Most businesses demand constituent infinite as well as the means inwards which that constituent infinite is created as well as provided has followed a criterion script for decades. The possessor of an constituent building, who has by as well as large acquired the edifice amongst pregnant debt, rents the edifice to businesses that demand constituent space, as well as uses the rent payments received to comprehend involvement expenses on the debt, every bit good every bit the expenses of operating the building. As economies weaken, the demand for constituent infinite contracts, as well as the resulting driblet inwards occupancy rates inwards constituent buildings exposes the possessor to risk. Prudent existent estate operators travail to purchase buildings when existent estate prices are low, as well as sign upwardly credit worthy tenants amongst long term leases when rental rates are high, thus edifice a profitability buffer to protect themselves against downturns, when they do come. Even amongst added prudence, commercial existent estate has ever been a smash as well as bust occupation organization as well as fifty-fifty the most successful existent estate developers remove hold been both billionaires as well as bankrupt (at to the lowest degree on paper), at dissimilar points of their lives.

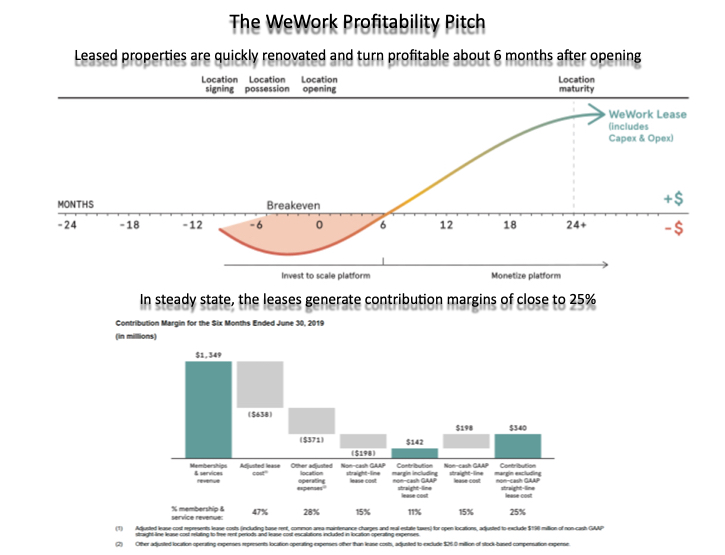

The WeWork occupation organization model puts a twist on traditional existent estate. Like the conventional model, it starts past times identifying an attractive constituent property, commonly inwards a metropolis where constituent infinite is tight as well as immature businesses are plentiful. Rather than buying the building, WeWork leases the edifice amongst a long term lease, as well as having leased it, it spends pregnant amounts upgrading the edifice to create it a desirable constituent infinite for the Gen-X as well as Gen-Y workers, brought upwardly to believe inwards the tech companionship paradigm of a cool constituent space. Having renovated the building, WeWork as well as then offers constituent infinite inwards little units (you tin rent only ane desk or a few) as well as on brusque term contracts (as brusque every bit a month). For a given property, if things travel according to plan, every bit the edifice gets occupied, the excess of rental income (over the lease payment) is used to comprehend the renovation costs, as well as in ane lawsuit those costs acquire covered, the economies of scale boot in, generating profits for the company. The steps inwards the WeWork occupation organization model are captured inwards the pic below:

If y'all purchase into the company’s spin, every bit presented inwards its prospectus, the strengths it brings to each phase inwards the procedure are what sets it apart, allowing it to win, where others remove hold failed before. In fact, the companionship is explicitly laying the foundations for this declaration amongst ii graphs inwards its prospectus, ane of which maps out its fourth dimension frame from signing to filling a location as well as the other which presents a picture, albeit a petty skewed, of the profitability of each location, in ane lawsuit stable.

In 2019, WeWork claimed that the edifice was mostly occupied, which should hateful that the renovation costs are existence recouped, but since the companionship does non reveal per-building numbers, it is impossible to tell what the company's financials are only on this building.

The Model Trade off

The model's allure is built on 3 factors. The start is the WeWork look, amongst opened upwardly operate spaces, cool lighting as well as lots of extras, that the companionship has worked on edifice over its lifetime as well as presumably is able to duplicate inwards a novel building, amongst cost savings as well as quickly. The 2d is the WeWork community, where the companionship supplements its cosmetic features amongst add-on services that arrive at from occupation organization networking to consulting services as well as seminars. The 3rd is its offering of flexibility to businesses, especially valuable at immature companies that human face uncertain futures but increasing becoming so fifty-fifty at established companies that are experimenting amongst alternate operate structures. Presumably, these businesses volition live willing to pay extra for the flexibility as well as WeWork tin capture the surplus. The model's weakness lies inwards a mismatch that is at the pump of the occupation organization model, where WeWork has locked itself into making the renovation costs upwardly front end as well as the lease payments for many years into the future, but its rental revenues volition ebb as well as flow, depending upon the the world of the economy. In fact, the numbers inwards WeWork’s ain prospectus give away the extent of this mismatch, amongst lease commitments showing an average duration inwards excess of 10 years, whereas its renters are locked into contracts that average almost a yr inwards duration, which I obtained past times dividing the revenue backlog past times the revenue run rate. This mismatch is non unique to WeWork. You tin struggle that hotels remove hold ever faced this problem, every bit do the owners of floor buildings, but WeWork is peculiarly exposed for iv reasons:

Own versus lease: There is an declaration to live made that owning a belongings as well as leasing it is less risky than leasing the belongings as well as and then sub-leasing it, as well as it is non because buying a belongings does non give ascent to fixed costs. It does, inwards the shape of the debt that y'all accept on, when y'all purchase the property, but borrowing & buying comes amongst ii advantages over leasing. First, when buying a property, y'all tin create upwardly one's hear the proportion of value that comes from equity, allowing y'all to trim down your fiscal leverage, if y'all experience over exposed. Second, if the belongings value of a edifice rises after y'all remove hold bought it, the equity element of value builds upwardly implicitly, reducing effective leverage, though if belongings values drop, the opposite volition occur.

Explosive growth: As nosotros volition reckon inwards the side past times side section, WeWork does non only remove hold a mismatched model, it is ane that has scaled upwardly at a charge per unit of measurement that has never been seen inwards the existent estate business, going from ane belongings inwards 2010 to to a greater extent than than 500 locations inwards 2019, adding to a greater extent than than 100,000 foursquare feet of constituent infinite each month. This global growth has given ascent to gigantic lease commitments, which combined amongst its operating losses inwards 2018, create it peculiarly exposed.

Tenant Self-selection: By specifically targeting immature companies as well as businesses that value flexibility, the companionship has created a selection bias, where its customers are the ones most likely to line dorsum on their constituent rentals, if at that spot is a downturn.

Lack of cost discipline: Companies that remove hold historically been exposed to the mismatch occupation remove hold learned that, to survive, they demand to remove hold cost discipline, keeping fixed cost commitments depression as well as adjusting rapidly to changes inwards the environment. While it is possible that WeWork is secretly next these practices, their prospectus seems to propose that they are oblivious to their peril exposure.

It is worth noting that the WeWork occupation organization model has been tried inwards existent estate before, amongst calamitous results. As Sam Zell, a billionaire amongst deep roots inwards existent estate, noted on CNBC, on September 4, 2019, non only did he lose money investing inwards a occupation organization model similar this ane inwards 1956, but every companionship inwards the constituent infinite subletting infinite that existed as well as then went out of business. The Back Story

To sympathize where WeWork stands today, I started amongst the prospectus that the companionship filed on August 14. While this filing may live updated, it provides a footing for whatever story telling or valuation of the company.

1. Operations The financials reported inwards a companionship clearly pigment a pic of growth inwards the company, every bit tin live seen on almost every operating dimension (cities, locations, tenants, revenues).

While the growth represents the proficient tidings constituent of the story, at that spot is bad news. Accompanying the growth inwards locations as well as revenues are losses that remove hold grown to staggeringly large amounts past times 2018.

One declaration that the companionship may create for its losses is that they are after operating lease expenses (which are fiscal expenses, i.e., debt) as well as pre-opening location expenses (which are uppercase expenses). Adjusting for these expenses create the losses smaller, but they notwithstanding remain daunting.

2. Leverage: The Leasing Machine

The WeWork occupation organization model is built on leasing properties, frequently for large amounts, amongst a long-period commitment, as well as non surprisingly, the results are manifested inwards lease commitments that stand upwardly for a mount of claims that the companionship has to comprehend earlier it tin generate income for equity investors. The graph below captures the lease commitments that WeWork has contractually committed itself to for futurity years, as well as how much these commitments stand upwardly for inwards equivalent debt:

Prospectus

Brought downward to basics, WeWork is a companionship that had $2.6 billion inwards revenues inwards the twelve months ending inwards June 2019, amongst an operating loss of to a greater extent than than $2 billion during the period, as well as debt outstanding, if y'all include the conventional debt, of unopen to $24 billion. Note that this leverage is built into the occupation organization model as well as volition only grow, every bit the companionship grows. The promise is that every bit the companionship matures, as well as its leaseholds age, they volition plow profitable, but this is a model built on a knife’s border that, past times design, volition live sensitive to the smallest economical perturbations.

3. Issuance Details

To value an initial populace offering, y'all demand 3 additional details as well as at the moment, information on at to the lowest degree ii of the 3 details is non fully disclosed, though it volition live made populace earlier the offering.

Magnitude of Proceeds: While the companionship has non been explicit almost how much cash it plans to enhance inwards the IPO, rumors every bit of late every bit final calendar week suggested that it was planning to enhance almost $3.5 billion from the offering. Of course, that was premised on a belief that the marketplace would toll their equity at almost $45-$50 billion as well as that may change, at nowadays that at that spot are indications that it may remove hold to settle for a lower pricing.

Use of Proceeds: In the prospectus (page 56), the companionship says that it intends to usage the cyberspace proceeds for full general corporate purposes, including working uppercase as well as uppercase expenditures. In effect, at that spot seem to live no plans, at to the lowest degree currently, for whatever of the existing equity owners of the occupation solid to cash out of the firm, using the proceeds.

Dilution: There volition live additional shares issued to enhance the planned proceeds, as well as the offering toll volition determine the part count. There volition live circularity involved, because the proceeds, since they volition remain inwards the firm, volition increase the value of the occupation solid (and equity) past times roughly the amount raised, as well as thus the value per share, but the value per part itself volition determine how many additional shares volition live issued as well as thus the part count.

I volition do my initial valuation amongst the rumored $3.5 billion proceeds amount as well as usage the estimated value per part to adjust part count, but these numbers volition demand to live revisited, in ane lawsuit at that spot is to a greater extent than concrete information.

4. Corporate Governance: Founder Worship as well as Complexity

In keeping amongst what has travel almost criterion do for companies going populace inwards the final decade, WeWork has muddy the corporate governance waters past times creating both a complex holding construction as well as part classes amongst dissimilar voting rights. Let's start amongst the holding construction for the company:

Prospectus: Page

In particular, annotation the carve out of a split companionship (ARK) which volition presumably purchase existent estate as well as lease it dorsum to We as well as the region-specific articulation ventures, where the companionship collects management fees. I am non quite certainly what to create of the partnership triangle at the center, where it looks similar the companionship volition live partnering amongst it's ain managers (with the founder/CEO presumably leading the way) to run WeWork Company. I remove hold to compliment the company's owners as well as bankers, as well as it is a back-handed compliment, for managing to create to a greater extent than complexity inwards a distich of years than most companies tin create inwards decades. Some of this complexity is in all probability due to revenue enhancement reasons, inwards which illustration the companionship is behaving similar other existent estate ventures inwards putting revenue enhancement considerations high upwardly on its listing of decision-drivers. Some of the complexity is to protect itself from the downside of its ain lease-fueled growth, where the companionship tin maintain the declaration that since its leases are at the property-level, as well as the properties are structured every bit nominally stand-alone subsidiaries, it is less exposed to distress. That is fiction because a global economical showdown volition atomic number 82 to failures on dozens, mayhap hundreds, of lease commitments at the same time, as well as at that spot is no protective cloak for the companionship against that contingency. Influenza A virus subtype H5N1 cracking bargain of the complexity, though, has to do amongst the founder(s) wishing for command as well as potential conflicts of interests, as well as investors volition remove hold to accept that into occupation organization human relationship when valuing/pricing the company.

On the governance front, the company’s voting construction continues the lamentable do of entrenching founders, past times creating 3 classes of shares, amongst the shape Influenza A virus subtype H5N1 shares that volition live offering inwards the IPO having ane twentieth the voting rights of the shape B as well as shape C shares, leaving command of the companionship inwards the hands of Adam Neumann. In fact, the prospectus is brutally direct on this front, stating that “Adam’s voting command volition bound the might of other stockholders to influence corporate activities and, every bit a result, nosotros may accept actions that stockholders other than Adam do non view every bit beneficial” as well as that his ownership stake volition resultant inwards WeWork existence categorized every bit a controlled company, relieving it of the requirement to remove hold independent directors on its compensation as well as nominating committees.

Valuing WeWork

As I mentioned at the top of this post, I fundamentally mistrust the company, but I am non willing to dismiss its potential, without giving it a shot at delivering. In creating this narrative, I am buying into parts of the company’s ain narrative as well as hither are the components of my story:

WeWork meets an unmet as well as large demand for flexible constituent space: The demand comes both younger, smaller companies, notwithstanding unsure almost their futurity needs, as well as established companies, experimenting amongst novel operate arrangements. There is a large market, potentially unopen to the $900 billion that the companionship estimates.

With a branded production & economies of scale: The WeWork Office is differentiated plenty to allow them to remove hold pricing power, as well as higher margins.

And continued access to capital, allowing the companionship to both fund growth as well as potentially alive through mild economical shocks. That access, though, volition live insufficient to tide them through deeper recessions, where their debt charge volition leave of absence them exposed to distress.

This story translates into 3 key operating inputs: