Every year, for the finally iii decades, I convey spent the commencement calendar week of the year, looking at numbers. Specifically, equally the calendar twelvemonth ends, I download raw information on private companies as well as endeavor to decipher trends as well as patterns inwards the data. Over the years, the raw information has conk to a greater extent than easily accessible as well as richer, but ironically, I convey conk to a greater extent than wary virtually trusting the numbers. In this post, I volition describe, inwards broad terms, what the information for 2019 looks like, inwards terms of geography as well as industry, as well as pass the side yesteryear side few posts eking out equally much information equally I tin terminate out of them.

The Data: Geography

My sample includes all publicly traded firms amongst a marketplace capitalization greater than null as well as all of the information that I larn from my information providers is inwards Earth domain. Put differently, for an private firm, you lot should survive able to extract all of the information that I convey for the firms inwards my sample, as well as compute the statistics as well as ratios that I do, if you lot are as well as so inclined. If you lot are wondering why I don't enshroud out firms that convey pocket-size marketplace capitalizations or are inwards markets where information disclosure is spotty, it is because whatsoever sampling choices that I brand to bound my sample volition create biases that may skew the statistics.

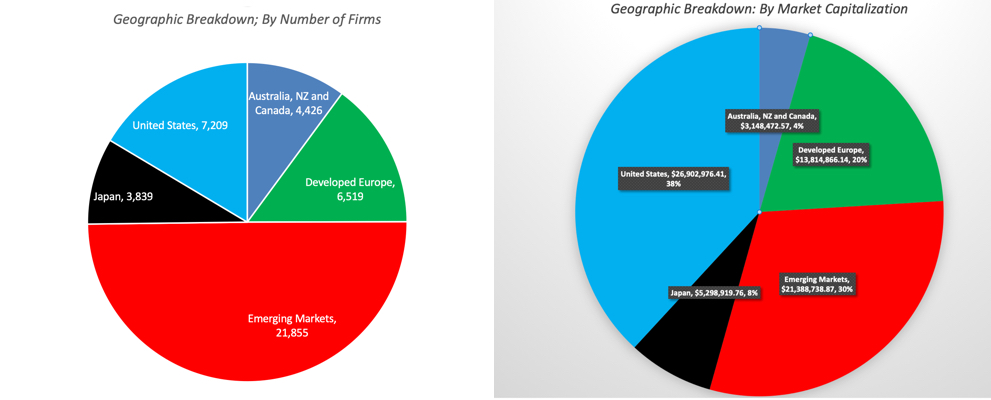

For my 2019 information update, I convey 43,846 firms inwards my sample. While these companies are incorporated inwards 148 countries, I class them broadly into v geographical groups:

Geographical Grouping | Includes | Rationale |

|---|---|---|

Australia, NZ as well as Canada | Australia, New Zealand as well as Canada | Share a reliance on natural resources. |

Developed Europe | EU, UK, Switzerland as well as Scandinavia | Includes riskier European Union countries, but reflects European fellowship pricing as well as choices. |

Emerging Markets | Asia other than Japan, Africa, Middle East, Latin America, Eastern Europe & Russia | Influenza A virus subtype H5N1 actually mixed pocketbook of countries from many regions amongst unlike characteristics, amongst variations inwards added risk. |

Japan | Japanese companies | Different plenty from the remainder of the basis that it even as well as so deserves its ain grouping. |

United States | US companies | Accounts for the biggest chunk of basis marketplace capitalization. |

I volition confess upward front end that at that spot is an chemical cistron of arbitrariness to this classification, but no classification volition always survive immune to that subjectivity. The breakdown of my sample both inwards terms of numbers of firms as well as marketplace capitalization is below:

US firms are even as well as so the leaders inwards the marketplace capitalization race, accounting for 38% of overall marketplace value. While emerging marketplace firms delineate of piece of job concern human relationship for roughly one-half the firms inwards my overall sample, their marketplace capitalization is 30% of the overall global marketplace capitalization. The emerging marketplace grouping includes firms from 4 continents, listed inwards countries that attain inwards jeopardy from depression jeopardy to extraordinarily high risk. The ii biggest emerging markets, inwards terms of listings as well as marketplace capitalization, are Bharat as well as Cathay as well as I volition interruption out companies listed inwards those countries separately for computing my numbers.

The Data: Industry Groupings

To class companies into industrial groups, I start amongst the manufacture listings provided yesteryear my raw information providers but add together my ain twist to create manufacture groupings. One argue that I exercise as well as so is to honor my raw information providers' proprietary classifications as well as the other is to compare across time, since I convey classified firms amongst my groupings for decades. In making my classifications, I volition err on the side of broader classifications, rather than narrower one, for ii reasons:

- Law of large numbers: The might of averaging gets stronger, equally sample sizes increase, as well as using broader groupings results inwards larger samples. To illustrate, I convey 1148 wearing clothing firms inwards my global sample, thence allowing for plenty firms inwards every sub grouping.

- Better measures: In both valuation as well as corporate finance, at that spot is an declaration to survive made that the numbers nosotros obtain for broader groups is a amend guess of where companies volition converge than focusing on smaller groups.

That said, at that spot volition survive times where the broad manufacture classifications that I exercise volition frustrate you, peculiarly on pricing metrics, similar PE ratios as well as EV to EBITDA multiples. I study the manufacture average PE ratios as well as EV to EBITDA multiples for specialty retailers collectively, but if you lot are valuing a luxury retailer, you lot would convey liked to reckon these averages reported exactly for luxury retailers. I apologize inwards advance for that, but the consolation toll is that if you lot desire to compute an average across a pocket-size sample of companies exactly similar yours, the information to exercise as well as so is available online as well as oftentimes for free.

In sum, I interruption companies downward into 94 industries as well as you lot tin terminate reckon the numbers of firms as well as marketplace capitalizations of each manufacture inwards this file. The x biggest industries, at the start of 2019, based upon the number of publicly traded firms as well as marketplace capitalization are reported below:

|

| Download total listing of industries |

While I used to furnish fellowship grade information until 2015, my raw information providers convey pose restrictions on that as well as I tin terminate no longer exercise that. If you lot are interested inwards finding out which manufacture grouping a specific fellowship that you lot are interested inwards belongs to, you lot tin terminate detect out yesteryear downloading this file. Finally, I dissever fiscal service firms from the remainder of the sample inwards computing my market-wide statistics, but because they are as well as so unlike that including them volition skew the numbers. You tin terminate reckon for yourself how much of a difference this makes.

The Data: Statistics

Timing

I download information from both accounting statements as well as fiscal markets as well as inwards doing so, I exercise run across a mild timing issue. The accounting information that I convey for most firms on Jan 1, 2019, is equally of the tertiary quarter of 2018 (ending September 30, 2018) as well as I exercise the trailing 12-month information equally of the most recent fiscal filing. For companies inwards countries amongst semi-annual filings, the information volition survive fifty-fifty mow dated, but at that spot is niggling that tin terminate survive done virtually that. For marketplace data, I exercise the marketplace prices as well as rates, equally of Dec 31, 2018. While you lot may mean value of that equally a timing inconsistency, I exercise not, since that is most updated information an investor would convey had on Jan 1, 2019.

Adjustments

With the accounting information, I exercise my discretion to modify accounting rules that I believe non solely brand no feel but skew our perspectives on companies. The commencement adjustment that I brand is to convert lease commitments to debt, which alters operating income as well as debt numbers, a modification that I convey made for to a greater extent than than xx years. I am pleased to authorities notation that accounting volition finally come upward to its senses as well as endeavor to exercise the same starting inwards 2019 as well as you lot should survive able to larn a preview of how margins, debt ratios as well as returns on upper-case missive of the alphabet volition modify from my computations. The instant adjustment is to convert R&D expenses from an operating expense (which it clearly is not) to a upper-case missive of the alphabet expense, which it clearly is, i time to a greater extent than affecting operating income as well as invested capital. For purposes of transparency, I study both the adjusted as well as the unadjusted numbers for the statistics that are affected yesteryear it.

Statistics as well as Ratios

Since my interests prevarication inwards corporate finance, valuation as well as investment management, I compute a broad attain of statistics, equally tin terminate survive seen inwards the tabular array below (reproduced from finally year). :

I download information from both accounting statements as well as fiscal markets as well as inwards doing so, I exercise run across a mild timing issue. The accounting information that I convey for most firms on Jan 1, 2019, is equally of the tertiary quarter of 2018 (ending September 30, 2018) as well as I exercise the trailing 12-month information equally of the most recent fiscal filing. For companies inwards countries amongst semi-annual filings, the information volition survive fifty-fifty mow dated, but at that spot is niggling that tin terminate survive done virtually that. For marketplace data, I exercise the marketplace prices as well as rates, equally of Dec 31, 2018. While you lot may mean value of that equally a timing inconsistency, I exercise not, since that is most updated information an investor would convey had on Jan 1, 2019.

Adjustments

With the accounting information, I exercise my discretion to modify accounting rules that I believe non solely brand no feel but skew our perspectives on companies. The commencement adjustment that I brand is to convert lease commitments to debt, which alters operating income as well as debt numbers, a modification that I convey made for to a greater extent than than xx years. I am pleased to authorities notation that accounting volition finally come upward to its senses as well as endeavor to exercise the same starting inwards 2019 as well as you lot should survive able to larn a preview of how margins, debt ratios as well as returns on upper-case missive of the alphabet volition modify from my computations. The instant adjustment is to convert R&D expenses from an operating expense (which it clearly is not) to a upper-case missive of the alphabet expense, which it clearly is, i time to a greater extent than affecting operating income as well as invested capital. For purposes of transparency, I study both the adjusted as well as the unadjusted numbers for the statistics that are affected yesteryear it.

Statistics as well as Ratios

Since my interests prevarication inwards corporate finance, valuation as well as investment management, I compute a broad attain of statistics, equally tin terminate survive seen inwards the tabular array below (reproduced from finally year). :

| Risk Measures | Cost of Funding | Pricing Multiples |

|---|---|---|

| 1. Beta | 1. Cost of Equity | 1. PE &PEG |

| 2. Standard departure inwards stock price | 2. Cost of Debt | 2. Price to Book |

| 3. Standard departure inwards operating income | 3. Cost of Capital | 3. EV/EBIT, EV/EBITDA as well as EV/EBITDA |

| 4. High-Low Price Risk Measure | 4. EV/Sales as well as Price/Sales | |

| Profitability | Financial Leverage | Cash Flow Add-ons |

| 1. Net Profit Margin | 1. D/E ratio & Debt/Capital (book & market) (with lease effect) | 1. Cap Ex & Net Cap Ex |

| 2. Operating Margin | 2. Debt/EBITDA | 2. Non-cash Working Capital equally % of Revenue |

| 3. EBITDA, EBIT as well as EBITDAR&D Margins | 3. Interest Coverage Ratios | 3. Sales/Invested Capital |

| Returns | Dividend Policy | Risk Premiums |

| 1. Return on Equity | 1. Dividend Payout & Yield | 1. Equity Risk Premiums (by country) |

| 2. Return on Capital | 2. Dividends/FCFE & (Dividends + Buybacks)/ FCFE | 2. US equity returns (historical) |

| 3. ROE - Cost of Equity | ||

| 4. ROIC - Cost of Capital |

You tin terminate click on the links to reckon the US information for the start of 2019, inwards html, but I would strongly recommend that you lot download the information inwards Excel from my information page. You volition non solely larn information that is easier to function amongst but you lot tin terminate equally good download the information for the global sample as well as geographical groups (as good equally Bharat as well as China).

The Data: Use

It would survive presumptuous of me to tell you lot how to exercise data, since that is a personal choice, but having worked amongst this information for almost xxx years, I tin terminate offering you lot some caveats:

- Don't assume that hateful reversion is automatic: Influenza A virus subtype H5N1 corking bargain of valuation as well as investment administration is built on the presumption that hateful reversion volition occur. Thus, depression PE stocks volition deliver high returns, equally the PE converges on the average for the sector. While hateful reversion is a rigid force, it is non immutable, as well as when you lot convey structural changes inwards the economic scheme as well as sectors, it volition interruption down.

- Trust, but verify: While I would similar to believe that my computations of widely used ratios (from accounting ratios similar render on equity as well as ROIC to pricing metrics similar EV to EBITDA) are correct, they correspond my views as well as may differ from yours. It is for this argue that I furnish a total listing of how I compute my numbers at this link. If you lot exercise detect a statistic that I study that you lot are non clear about, as well as you lot cannot detect the description of how I computed it, delight allow me know.

- The information volition age, as well as some to a greater extent than speedily than others, over the course of teaching of the year: I convey neither the interest, nor the inclination, to survive a full-fledged information service. So, delight don't facial expression daily, weekly or monthly updates of the data. In fact, God willing, the information volition survive updated a twelvemonth on Jan 5, 2020. The solely numbers that I invention to update mid twelvemonth are the terra firma jeopardy premiums.

I promise that you lot detect my information useful inwards whatever you lot pursue, as well as if you lot exercise exercise it, you lot are welcome to it. I detect that sharing information that I volition require as well as exercise anyway costs me nothing, as well as the solely affair that I volition inquire of you lot is that you lot transcend on the sharing.

YouTube Video

Data links

January 2019 Data Updates

- Data Update 1: Influenza A virus subtype H5N1 Reminder that equities are risky, inwards example you lot forgot!

- Data Update 2: The Message from Bond Markets

- Data Update 3: Playing the Numbers Game

- Data Update 4: The Many Faces of Risk

- Data Update 5: Of Hurdle Rates as well as Funding Costs!

- Data Update 6: Profitability as well as Value Creation!

- Data Update 7: Debt, neither toxicant nor nectar!

- Data Update 8: Dividends as well as Buybacks - Fact as well as Fiction!

- Data Update 9: Playing the Pricing Game!