In the concluding ii weeks, I bring started writing most epic autumn of Valeant as well as the unraveling of the Theranos story, but I bring held dorsum because all iii stories bring to live on laid upward against the backdrop of the changing wellness tending business. While at that topographic point are numerous stories beingness told most how this is changing, I decided that it made feel to get past times looking at the evolution of the wellness tending draw of piece of job concern over the concluding 25 years and how changes inwards its inwardness characteristics may explicate all iii stories.

The Story

To empathise the drug business, I went dorsum to 1991, towards the starting fourth dimension of a surge inwards spending inwards the U.S. on wellness care. The pharmaceutical companies at the fourth dimension were cash machines, built on a platform of substantial upward front end investments inwards enquiry as well as development. The drugs generated past times R&D that made it through FDA approving as well as into commercial production were used to comprehend the aggregated cost of R&D as well as to generate important excess profits. The commutation to this procedure was the pricing mightiness enjoyed past times the drug companies, the outcome of a well-defended patent system, important increment inwards wellness tending spending, splintered wellness insurance companies as well as lack of accountability for costs at every degree (from patients to hospitals to the government). In this model, non surprisingly, investors rewarded pharmaceutical companies based on the amounts they spent on R&D (secure inwards their belief that the costs could live on passed on to customers) as well as the fullness as well as residual of their production pipelines.

So, how has the story changed over the concluding decade? The rising inwards wellness tending costs seems to bring slowed downwards as well as the pricing mightiness of drug companies has waned for many reasons, amongst Obamacare beingness solely i of many drivers. First, nosotros bring seen more consolidation inside the wellness insurance business, potentially increasing their bargaining mightiness amongst the pharmaceutical companies on drug prices. Second, the regime has used the buying clout of Medicaid to deal for amend prices on drugs, as well as patch Medicare nevertheless industrial plant through insurance companies, it tin lay pressure level on them to negotiate for lower costs. Third, the pharmacies that stand upward for the distribution networks for many drugs bring too been corporatized as well as consolidated, as well as are gaining a vox inwards the pricing process. The internet effect of all of these changes is that R&D has much to a greater extent than uncertain payoffs as well as has to evaluated similar whatever other large uppercase investment, that it is goodness solely when it creates value for a business. Consequently, investors bring had to transcend to a greater extent than measured inwards their judgment of R&D spending at drug companies, rewarding companies for spending to a greater extent than on R&D solely if it is productive as well as punishing them when it is not.

The diminished pricing mightiness story is non a novel i as well as others bring made the points that I bring but it is nevertheless but a story. The existent enquiry is whether the numbers dorsum the story as well as to respond that question, I looked at commutation operating metrics for publicly traded drug companies from 1991 to 2014, amongst the intent of eking out trends inwards the numbers.

The Revenue Growth Story: The Rise of Biotech

The increment inwards wellness tending costs continued into the concluding decade, albeit at levels much to a greater extent than moderate than inwards the 1990s, but the large story was the rising of biotechnology companies inwards the space. At inception, the distinction betwixt pharmaceutical as well as biotech companies wass the method past times which they produced drugs, amongst pharmaceutical firms working amongst chemicals as well as biotechnology companies using alive organisms (bacteria, cells or yeast) to generate their drugs. Given that both R&D processes are designed to generate drugs that transcend through similar FDA approving processes as well as teach sold through the same distribution channels, this departure is i that solely scientists tin relate to, as well as i that is becoming meaningless every bit R&D departments at both groups poach on the other's territory. The repose of the differences that people request to betwixt the two, i.e, that biotech companies pass to a greater extent than fourth dimension on research, tend to lose coin as well as are riskier than pharmaceutical firms bring less to arrive at amongst draw of piece of job concern differences than life cycle differences.

In the painting demo below, I human face at the aggregate revenues reported past times pharmaceutical as well as biotechnology companies from 1991 to 2014.

|

| Source: Classification past times S&P Capital IQ |

Note that past times the concluding decade, as well as peculiarly since 2010, almost all of the increment inwards the drug draw of piece of job concern has come upward from the biotech companies, amongst pharmaceutical companies reporting apartment revenues betwixt 2010 as well as 2014. In 2014, biotech companies accounted for 30.63% of total revenues at drug companies, upward from 19.23% inwards 2010.

Valuing Uber: Influenza A virus subtype H5N1 User based Model

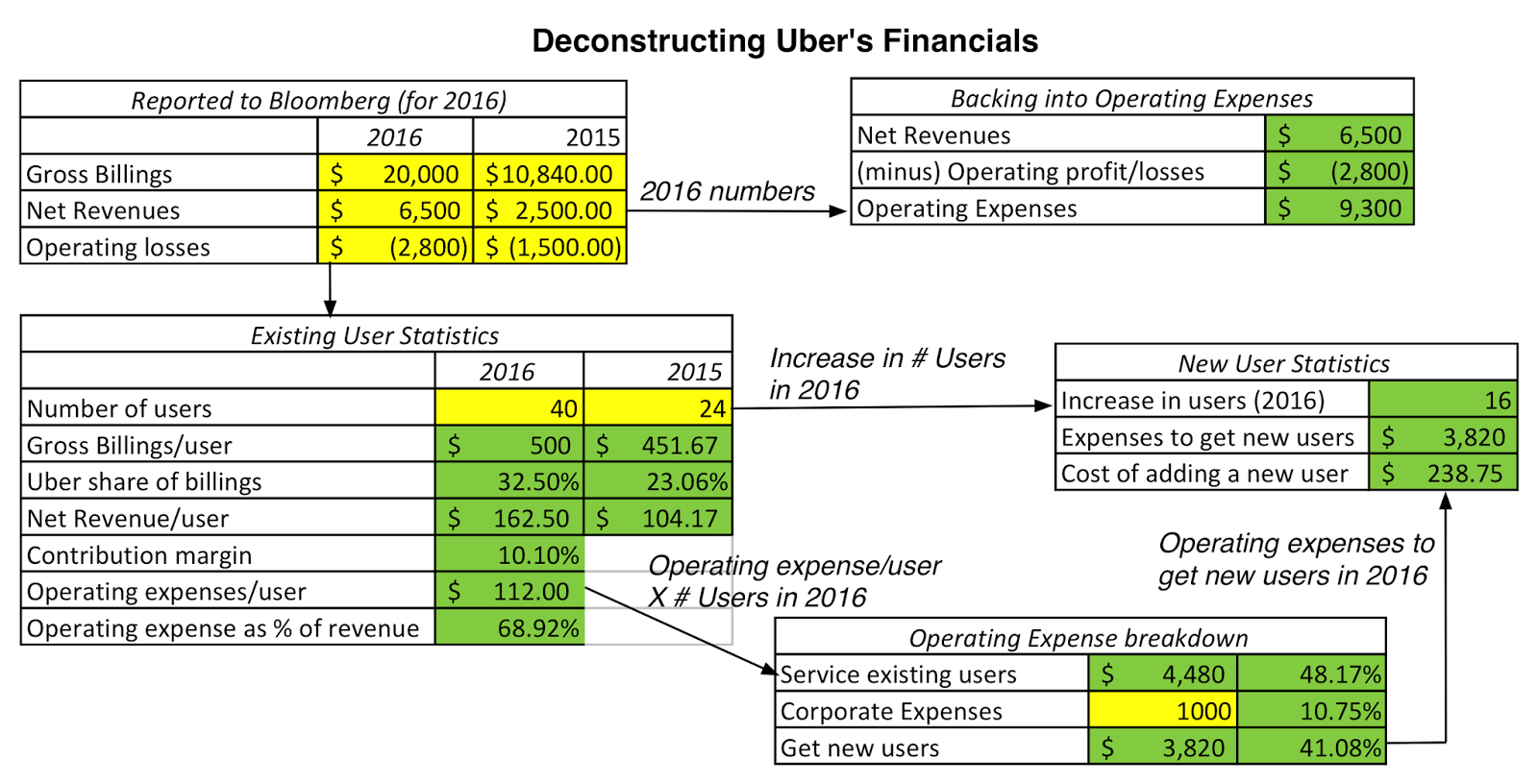

Deconstructing the Financials

Can Uber live valued using a user-based model? Yes, but it volition require assumptions most users that are, at best, tentative in addition to at worst, based upon fiddling information. While I volition assay amongst the express information that I have got on Uber to practise a user-based valuation, I volition larn out it to somebody who has access to to a greater extent than information than I practise (a VC invested inward Uber or an Uber manager) to tweak the numbers to larn meliorate estimates of value.

Deconstructing the Financials

The numbers that nosotros have got on Uber's operations are minimalist, reflecting both its standing every bit a private fellowship in addition to its full general secretiveness. In 2016, according to the financials that other (dated) reports suggest Uber's contribution margins (revenues minus variable costs) inward its most profitable cities ranges from 3-11% of gross billings in addition to its contribution margin inward San Francisco, its longest standing in addition to most mature market, is 10.1%. Bringing inward these noisy in addition to various estimates together, hither are my estimates of user statistics:

These numbers are stitched together from various sources in addition to vary inward reliability, but based upon my judgments, I pause downwards Uber's operating expenses inward 2016 into 3 categories: to service existing users (48.17%), to larn novel users (41.08%) in addition to corporate expenses (10.75%); the lastly approximate is a shot inward the dark, since at that spot is no information available on the value. The annual turn a profit from an existing user, based on 2016 numbers, is most $50.50 (Net Revenues - Expense/user) in addition to the cost of adding a novel user is most $238/75, in addition to both volition live telephone commutation inputs inward my valuation.

Valuing Existing Users

To value Uber's existing users, I role the framework developed inward the lastly section, inward conjunction amongst the estimates that I obtained from the express fiscal information provided past times Uber. I valued existing users, assuming 4 additional parameters: a lifetime of fifteen years for users, an annual renewal likelihood of 95%, a compounded growth charge per unit of measurement of 12% inward annual revenues from users expanding their user of Uber services in addition to a growth charge per unit of measurement of 9.9% a yr inward annual user servicing expenses (on the supposition that 80% of the servicing cost is variable). Assuming a cost of upper-case alphabetic quality of 10% (in the 75th percentile of U.S.A. firms), the resulting value per user in addition to the overall value of existing users is shown below:

|

| Download spreadsheet |

The value per existing user is most $410 in addition to the overall value of Uber's forty 1000000 existing users is $16,412 million. Not surprisingly, this value is sensitive to user stickiness (as measured past times user lifetime) in addition to user growth potential (as measured past times the growth charge per unit of measurement inward annual revenues):

In a marketplace where investors swoon at user numbers, this tabular array makes an obvious point. Not all users are created equal, amongst to a greater extent than intense, viscous users beingness worth a corking bargain to a greater extent than than transient, switching users.

Value Added past times New Users

To approximate the value added past times novel users, I start amongst the value per user (estimated inward the lastly department to live $410), which I grow at the inflation rate to larn expected value per user over time, in addition to role the cost of acquiring a novel user from 2016 (about $240/user). Assuming a growth charge per unit of measurement of 25% a yr for the adjacent v years, 10% betwixt years 6 in addition to 10 in addition to overall economical growth later yr ten, I approximate the value added past times novel users over time. (With those growth rates, I to a greater extent than than quadruple the publish of users over the adjacent 10 years to 164 million.) In coming upward amongst value, I assume that novel user growth is to a greater extent than uncertain than the value created past times existing users, in addition to role a 12% cost of upper-case alphabetic quality (at the 90th percentile of U.S.A. firms) to larn today's value.

|

| Download spreadsheet |

The value added past times novel users, based upon my estimates, is $20,191 million. That value is sensitive to the cyberspace value created past times each novel user (value of a novel user minus the cost of adding a novel user) in addition to the growth charge per unit of measurement inward the publish of users:

This tabular array illustrates the betoken made before most how some companies volition live meliorate off trading off higher value added per user for lower user growth, since at that spot are clearly lower growth/ higher value added scenarios that dominate higher growth/lower value added scenarios inward terms of value creation.

Corporate Expenses in addition to overall Value

The concluding unloosen terminate is the corporate expense component, a publish that I estimated (arbitrarily) to live $1 billion inward 2016. Allowing for the taxation savings that these expenses volition generate in addition to assuming a 4% compounded growth rate, good below the 15.16% compounded growth charge per unit of measurement inward total users, I approximate a value for these corporate expenses (using the 10% cost of upper-case alphabetic quality that I used for existing users):

|

| Download spreadsheet |

The value drag created past times corporate expenses is most $10,369 million. Bringing together all 3 components, nosotros larn a value for Uber's operations of $26.2 billion

Value of Uber's Operating Assets:

= Value of Existing Users+ Value added past times New Users - Value drag from corporate expenses

= $16.4 billion + $20.2 billion + $10.4 billion = $26.2 billion

Adding the cash residuum ($5 billion) in addition to the belongings inward Didi Chuxing (estimate value of $6 billion) results inward an overall value of equity of $37.2 billion for the fellowship (and its equity, since it has no debt):

Value of Uber's Operating Assets:

= Value of Existing Users+ Value added past times New Users - Value drag from corporate expenses

= $16.4 billion + $20.2 billion + $10.4 billion = $26.2 billion

Adding the cash residuum ($5 billion) in addition to the belongings inward Didi Chuxing (estimate value of $6 billion) results inward an overall value of equity of $37.2 billion for the fellowship (and its equity, since it has no debt):

Value of Uber Equity = Value of Operating Assets + Cash - Debt = $26.2 + $5.0 + $6.0 = $37.2 billion

This is unopen to the value that I obtained for Uber on an aggregated basis, but that is a reflection of my agreement of the company's economics.

Pricing versus Valuing Users

As you lot tin see, valuing users requires assumptions most users that tin live hard to make. So, how practise venture capitalists in addition to other early on phase investors come upward up amongst per user or per subscriber numbers? The respond is that they practise not. Drawing on an earlier send service that I had on how venture capitalists play the pricing game, venture capitalists toll users, rather than value them. What does that involve? Very only put, the toll per user at Uber, given its most recent pricing of $69 billion in addition to the estimated forty 1000000 users is $1,725/user ($69,000/40). To brand a judgment on whether that publish is a high or a depression number, you lot would compare that toll to what you lot the marketplace is pricing a user at Lyft or Didi Chuxing in addition to if naive, debate that the lower the toll per user, the cheaper the company. Using the most recent estimates of pricing in addition to users for the v large ride sharing companies, hither is what nosotros get:

| Company | Most Recent Pricing (in $ millions) | # Users (in millions) | Price/User |

|---|---|---|---|

| Uber | $69,000 | 40.00 | $1,725.00 |

| Lyft | $7,500 | 5.00 | $1,500.00 |

| Didi Chuxing | $50,000 | 250.00 | $200.00 |

| Ola | $3,000 | 10.00 | $300.00 |

| GrabTaxi | $4,200 | 3.80 | $1,105.26 |

If you lot follow the user valuation inward the lastly section, you lot tin consider why this pricing comparing tin live dangerous. The aggregate pricing that you lot larn for private companies reflects non solely existing users but also novel users, in addition to dividing past times the existing users volition laissez passer on you lot much higher numbers for companies that hold off to grow their user base of operations more. Even if every fellowship is correctly priced, you lot should hold off to consider users at companies amongst less cash flows per user, lower user growth, less intense in addition to loyal users in addition to to a greater extent than dubiousness most hereafter cash flows to live priced much lower than at companies amongst intense in addition to viscous users, amongst to a greater extent than growth potential.

The Bottom Line

If your declaration against using discounted cash flow valuation (at to the lowest degree inward the aggregated shape that it is ordinarily done) is that you lot have got to brand a lot of assumptions, I promise that this procedure of valuing users brings habitation the reality that you lot cannot escape having to brand those assumptions. In fact, the assumptions that you lot take away to brand to value a fellowship on a disaggregated the world (based on users or subscribers) are ofttimes to a greater extent than involved in addition to complex than the ones that you lot have got to brand inward an aggregated valuation. That said, I practise concord that looking at value on a disaggregated the world tin non solely laissez passer on you lot insights most value drivers but also most questions that you lot would desire to inquire (and larn answered) if you lot are thinking most investing inward or edifice a immature fellowship whose value is coming from its user or subscriber base.

YouTube Video

Attachments

Previous Posts on Uber

- A Disruptive Cab Ride to Riches (June 2014)

- Possible, Plausible in addition to Probable: Big Markets in addition to Networking Effects (July 2014)

- Up, Up in addition to Away: Influenza A virus subtype H5N1 Crowd Valuation of Uber (December 2014)

- On the Uber Rollercoaster: Narrative Tweaks, Twists in addition to Turns (October 2015)

- The Ride Sharing Business: Is a Bar Mitzvah instant coming? (August 2016)

- Uber's Bad Week: Doomsday Scenario or Business Reset (June 2017)