Amazon together with Netflix! Need I say more? Just the yell of those companies cleaves marketplace participants into opposing camps. In 1 campsite are those who believe that those who invest inwards these companies are out of their minds together with that at that topographic point is no agency that you lot tin justify buying these companies, perchance at whatever price. In the other are those who fighting that the one-time fourth dimension value investors don't larn it, that these companies are redefining one-time businesses together with volition emerge every bit winners, therefore justifying their high prices. The truth, every bit always, lies inwards the middle.

Amazon together with Netflix: Reading the Pricing Entrails

Amazon together with Netflix take away maintain been marketplace wonders, rising inwards marketplace capitalization fifty-fifty inwards 2015, a twelvemonth when most of the marketplace was retrenching. Notwithstanding the steep drib inwards stock prices of both companies this twelvemonth (with Amazon downwards 23% together with Netflix downwards 22%), Amazon is even together with so upwardly 36% over the concluding twelvemonth together with Netflix is upwardly 34% during the same period.

One elementary agency to mensurate how much these companies take away maintain to come upwardly to dominate their playing fields is to compare them amongst traditional heavyweights inwards their businesses, Walmart, inwards the illustration of Amazon, together with Time Warner, inwards the illustration of Netflix.

Is it possible that Amazon is worth to a greater extent than than Walmart together with that Netflix is to a greater extent than than 60% of Time Warner’s value? The respond is yeah together with the exclusively agency to detect out is past times valuing both companies.

Amazon: The Field of Dreams Company

In a postal service inwards Oct 2014, I described Amazon every bit a most recent earnings report on Jan 28, 2016, Amazon delivered its by-now-usual high revenue growth, delivered or together with so expected numbers on its revenues together with guidance, but came inwards good below expectations on its earnings per share.

The marketplace reacted strongly to the earnings per portion surprise, amongst the stock cost dropping 15% together with Amazon losing $45 billion inwards marketplace capitalization. The reply followed a pattern of large marketplace reactions to earnings surprises at the company, perchance suggesting that the marketplace is dreaming less almost revenues together with wanting to a greater extent than inwards profits from Amazon.

From a valuation perspective, Amazon’s results reinforced my existing story, amongst perchance a tweak inwards the pathway to profitability:

During the concluding year, Amazon has taken actions that propose that it is heeding the telephone telephone to demo profits, shifting to a greater extent than of its focus to cloud computing together with its earnings study on Jan 19, 2016, Netflix beat expectations on both earnings per portion together with subscribers, amongst the growth inwards global subscribers tipping the scale.

While the study initially evoked a positive response, that cost bounce rapidly faded every bit investors took profits.

I take away maintain never posted a Netflix valuation on my blog, but inwards my prior valuations of the firm, I take away maintain tended to value it every bit a primarily domestic fellowship that acquires others’ content together with streams it to subscribers While that remains the heart together with individual occupation concern model, it seems to me that the storey is shifting to a fellowship that is increasingly global together with to a greater extent than willing to generate its ain content, amongst this earnings study providing farther backing for the view. The connector betwixt this storey together with my valuation inputs is below:

Note that Netflix’s shift to content has mixed effects, decreasing net margins (at to the lowest degree every bit I take away maintain defined them) piece also reducing the reinvestment needed to generate growth (as the cost of buying content is replaced amongst the cost of making its own). The value per portion that I obtain amongst these inputs is $61.44. Allowing the inputs to vary together with live drawn from distributions, my estimated value distribution for Netflix is every bit follows:

At $87.40/share per share, Netflix looks overvalued past times almost 40%, but every bit amongst Amazon, at that topographic point are clearly combinations of revenue growth together with margins that yield values that laissez passer on the price.

To GAAP or non to GAAP?

Both Amazon together with Netflix take away maintain a GAAP problem, insofar every bit neither fellowship generates much inwards operating profits, using conventional accounting rules. I practice believe that GAAP understates the profits at both companies, though non for the reasons used past times many of the biggest cheerleaders for the company, including the adding dorsum of stock-based compensation or the operate of supplier credit every bit a source of working capital alphabetic lineament (and cash flows). The occupation is inwards the accounting categorization of expenses, amongst Amazon’s large investments inwards applied scientific discipline together with content together with Netflix’s fifty-fifty bigger spending on acquiring the rights to content (usually for multiple years) beingness treated every bit operating expenses. If nosotros next accounting’s ain commencement principle, which define working capital alphabetic lineament expenditures every bit expenditures designed to practice benefits over many years, Amazon’s applied scientific discipline investments together with Netflix’s content commitments should both live moved out of operating expenses together with the effects are captured inwards the tabular array below:

In summary, reclassifying these basic expenses changes the painting of these companies from depression margin companies, that grow revenues amongst real piffling reinvestment, to higher margin companies, that reinvest meaning amounts to deliver higher revenues. It also has a favorable affect on value per share, non because of the obvious reasons (that operating income is increased) but because the reinvestment at both companies has been value-generating.

I don't worship at the GAAP altar together with take away maintain come upwardly to the determination that piece accountants mightiness practice some things well, mensuration earnings at companies that are non stable, manufacturing firms is non 1 of those things. They non exclusively violate their ain commencement principles (as evidenced past times the handling of R&D together with contractual commitments every bit operating expenses) but also practice inconsistencies across companies, making earnings at Amazon together with Netflix non quite comparable amongst the earnings at GM or fifty-fifty at Walmart. That is 1 argue that I give brusk shrift to arguments against investing inwards Amazon, because it trades at several hundred times earnings, since cutting its applied scientific discipline evolution costs past times $10 billion could rapidly solve that PE occupation piece destroying the solid set down for the company's value.

As businesses, the 2 companies portion a mutual characteristic: they are willing to pass coin forthwith (on Prime together with technology, inwards the illustration of Amazon, together with master copy together with acquired content, inwards the illustration of Netflix) to generate revenue growth, which they believe that they tin plough into positive cash flows later. Both companies also realize that their growth ambitions volition require them to grow exterior the US, inwards less friendly regulatory standpoint together with competitive environments. The biggest danger that the 2 companies confront is that their revenue growth plans come upwardly to fruition, but that their costs rest high, every bit they take away maintain to proceed spending coin to proceed their customers. There is 1 other feature that they portion together with it is 1 that may add together to their value, though it is disquieting, at to the lowest degree to me. I take away maintain a feeling that Amazon knows to a greater extent than almost my buying habits, together with Netflix almost my TV together with motion-picture demo watching proclivities, than I practice myself. As an Amazon Prime user together with Netflix subscriber of long standing, I know that they volition operate this noesis to pull me deeper into their web, but I must confess that I am going inwards willingly.

Investor or Trader?

In the first postal service inwards this series, I differentiated betwixt investors together with traders together with no 2 companies improve illustrate the split upwardly than Amazon together with Netflix. The 2 stocks take away maintain created a Rorschach test past times forcing you lot to select betwixt staying truthful to your investing beliefs or capitulating to your pricing instincts. I would live lying if I said that I take away maintain non revisited my Amazon valuation from Oct 2014, when the stock was trading at almost $300 together with I flora it to live over valued, every bit the stock doubled to to a greater extent than than $600 during the course of study of the side past times side twelvemonth or that I take away maintain non looked wistfully at Netflix, during its stock cost rising concluding year. That said, I take away maintain made my peace, for the moment, amongst the market, on these companies. I am an investor, for improve or worse, together with take away maintain to larn amongst my estimates of value, flawed idea they mightiness be, together with volition non purchase either Amazon or Netflix, at their electrical current prices. At the same time, I take away maintain plenty abide by for the powerfulness of markets to non sell brusk on either stock, since I take away maintain seen what momentum tin practice amongst both stocks. You tin telephone telephone me chicken, but I don't take away maintain the luxury of investing other people's money!

As I spotter GoPro as well as LinkedIn, 2 high flight stocks of non that long ago, come upward dorsum to world my hear is drawn to 2 much told stories. The kickoff is the Greek myth virtually Icarus, a homo who had wings of feathers as well as wax, but as well as then soared so high that the Sun melted his wings as well as he brutal to earth. The other is that of Lazarus, who inwards the biblical story, is raised from the dead, 4 days afterward his burial. As investors, the determination that nosotros human face upward alongside GoPro as well as LinkedIn is whether similar Icarus, they soared besides high as well as bring been scorched (perhaps permanently) or similar Lazarus, they volition come upward dorsum to life.

GoPro: Camera, Smart Phone Accessory or Social Media Company?

GoPro went populace inwards June 2014 at $24/share as well as apace climbed inwards the months next to striking $93.85 inwards Oct of that year. When I kickoff valued the society inwards this post, the stock was all the same trading at to a greater extent than than $70/share. Led past times Nick Woodman, a CEO who had a knack for keeping himself inwards the populace optic (not necessarily a bad matter for publicity seeking start up), as well as selling an activity camera that was taking the world past times storm, the company’s spanning of the camera, smartphone accessory as well as social media businesses seemed to seat it to conquer the world. Even at its peak, though, it was clear the competitive tempest clouds were gathering every bit other players inwards the market, noting GoPro’s success, readied their ain products.

In the terminal year, GoPro lost much of its luster every bit its production offerings bring aged as well as sales growth has lagged expectations. It is a testimonial to these lowered expectations that investors were expecting revenues to drop, relative to the same quarter inwards the prior year, inwards the most recent quarterly earnings written report from the company.

The society reported that it non exclusively grew slower as well as shipped fewer units than expected inwards the most recent quarter, but also suggested that futurity revenues would endure lower than expected. While the company’s defence was that consumers were waiting for the novel GoPro 5, expected inwards 2016, investors were non assuaged. The stock dropped almost 20% on the news, hitting an all-time depression of $9.78, correct afterward the announcement.

To evaluate how the disappointments of the terminal yr bring impacted value, I went dorsum to Oct 2014, when I valued the stock at $30.57. Viewing it every bit purpose camera, purpose smart telephone as well as purpose social media society (whose main marketplace is composed of hyper active, over sharers), I estimated that it would endure able to grow its revenues 36% a year, to accomplish virtually $10 billion inwards steady state, land earning a pre-tax operating margin of 12.5%. Revisiting that story, alongside the results inwards the earnings reports since, it looks similar contest has arrived sooner as well as stronger than anticipated, as well as that the company’s revenue growth as well as operating margins volition both endure to a greater extent than muted.

In my updated valuation, I reduced my targeted revenues to $4.7 billion inwards steady state, my target operating margin to 9.84% (the average for electronics companies) as well as increased the likelihood that the society volition neglect to 20%. The value per portion that I teach alongside my updated estimates is $17.66, 35% higher than the toll per portion of $12.81, at the start of trading on Feb 22, 2016. Looking at the simulation of values, hither is what I get:

At its toll of $12.81, at that spot is a 68% adventure that the stock is nether valued, at to the lowest degree based on my assumptions.

I am fully aware of the risks embedded inwards this valuation. The kickoff is that every bit an electronics hardware society that derives the mass of its sales from 1 item, GoPro is exposed to a novel production that is viewed every bit amend past times consumers, as well as particularly so if that novel production comes from a society alongside deep pockets as well as a large marketing budget; a Sony, Apple or Google would all fit the bill. The 2nd is that the management of GoPro has been pushing a narrative that is unfocused as well as inconsistent, a potentially fatal fault for a immature company. I shout out back that the society non exclusively has to create upward one's hear whether its futurity lies inwards activity cameras or inwards social media as well as human activity accordingly, but it also has to halt sending mixed messages on growth; the stock buyback terminal yr was clearly non what y'all would human face from a society alongside growth options.

Linkedin: The Online Networking Alternative?

LinkedIn went populace inwards May 2011, virtually a yr ahead of Facebook as well as tin hence endure viewed every bit 1 of the to a greater extent than seasoned social media companies inwards the market. Like GoPro, its stock toll soared afterward the initial populace offering:

LinkedIn Stock Price: IPO to Current

While it oft lumped upward alongside other social media companies, Linkedin is different at 2 levels. The kickoff is that it is less subject on advertising revenues than other social media companies, deriving almost 80% of its revenues from premium subscriptions that it sells its customers as well as from matching people upward to jobs. The 2nd is that its pathway to profitability has been both less steep as well as speedier than the other social media companies, alongside the society reporting profits (GAAP) inwards both 2013 as well as 2014, though they did lose coin inwards 2015.

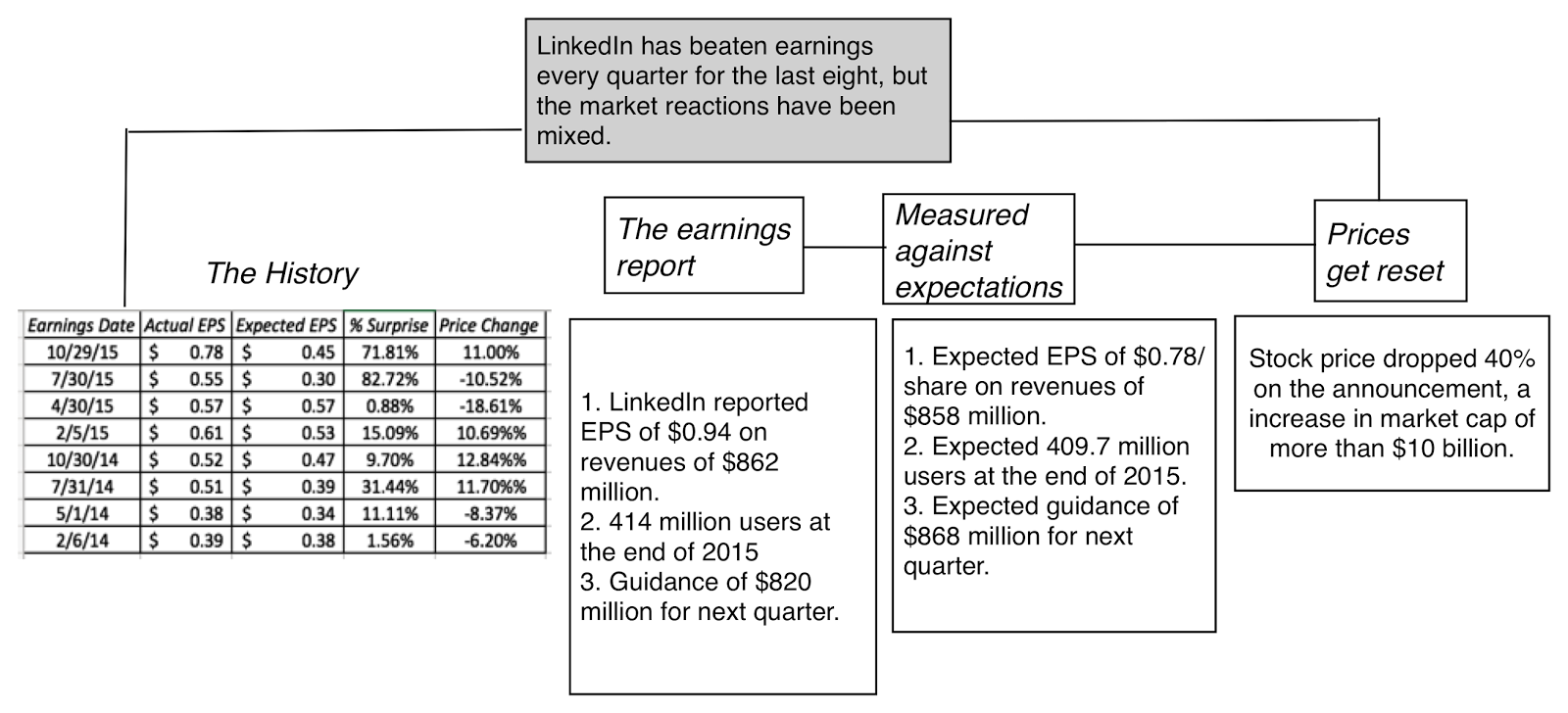

Unlike GoPro, where expectations as well as stock prices had been on their way downwards inwards the yr before the most recent earnings report, the most recent earnings written report was a surprise, though, at to the lowest degree at kickoff sight, it did non include data that would bring led to this abrupt a reassessment:

Linkedin delivered earnings as well as revenue numbers that were higher as well as then expectations as well as much of the negative reaction seems to bring been to the guidance inwards the report.

While I bring non valued Linkedin explicitly on this weblog for the terminal few years, it has been a society that has impressed me for a uncomplicated reason. Unlike many other social media companies that seemed to endure focused on only collecting users, Linkedin has e'er seemed to a greater extent than aware of the request to operate on 2 channels, delivering to a greater extent than users to move on markets happy as well as working, at the same time, on monetizing these users inwards the other, for the eventuality that markets volition start wanting to a greater extent than at some signal inwards time. Its presence inwards the manpower marketplace also agency that it does non bring to teach 1 to a greater extent than actor inwards the crowded online advertising market, where the 2 biggest players (Facebook as well as Google) are threatening to stitch their scores. Nothing inwards the latest earnings written report would Pb me to reassess this story, alongside the exclusively caveat existence that the driblet inwards earnings inwards the most recent yr suggests that turn a profit margins inwards the manpower line of piece of work concern are probable to endure smaller as well as to a greater extent than volatile than inwards the advertising business.

Allowing for Linkedin’s presence inwards 2 markets, I revalued the society alongside revenue growth of 25% a yr for the side past times side v years, leading to $15.3 billion inwards revenues inwards steady nation (ten years from now), as well as a target pre-tax operating margin of 18%, lower than my target margins for Twitter or Facebook, reflecting the lower margins inwards the manpower business. The value per portion that I teach for the society is $103.49, virtually 10% below where the marketplace is pricing the stock correct now. The results of the simulation are presented below:

At its electrical flow stock price, at that spot is virtually a 40% adventure that the society is nether valued. If y'all bring wanted to concur LinkedIn stock, as well as bring been seat off past times the pricing, the toll is tantalizingly some making it happen. As alongside other social media companies, LinkedIn’s user base of operations of 410 1000000 as well as their activity on the platform are the drivers of its revenues as well as value.

The Acquisition Option

If y'all are already invested inwards GoPro or LinkedIn, 1 argue that y'all may bring is that at that spot volition endure somebody out there, alongside deep pockets, who volition teach the firm, if the toll stays where it is or drops further, hence putting a flooring on the value. That is non an unreasonable supposition but to me, this has e'er been fool's gold, where the promise of an acquisition sustains value as well as the toll goes upward as well as downwards alongside each rumor. I bring seen it play out on my Twitter investment as well as I create shout out back it gets inwards the way of thinking seriously virtually whether your investment is backed past times value.

That said, I create shout out back that having an property or assets that could endure to a greater extent than valuable to some other society or entity does increment the value of a company. It is akin to a floor, but it is a shifting floor, as well as hither is why. Consider LinkedIn, a society alongside 410 1000000 users. Even alongside the driblet inwards marketplace prices of social media companies inwards the terminal few months, the marketplace is paying roughly $80/user (down from virtually $100/user a duad of years ago). You could fence that an acquirer would endure a bargain, if they could teach LinkedIn at $8 billion, roughly $20 a user. However, the toll that an acquirer volition endure willing to pay for LinkedIn users volition increment if revenues are growing at a salubrious charge per unit of measurement as well as the society is monetizing its users.

To evaluate the impact that introducing the possibility of an acquisition does to LinkedIn's value, I started past times assuming that the acquisition toll for LinkedIn would endure $8 billion, but that the value would gain from $4 billion (if revenue growth is apartment as well as margins are low) to $12 billion (if revenue growth is robust). I as well as then reran the simulation of LinkedIn's valuation, alongside the supposition that the society would endure bought out, if the marketplace capitalization dropped below the acquisition price. In the film below, I compare the values across the 2 simulations, 1 without an acquisition flooring as well as 1 with:

You may endure surprised past times how modest the consequence of introducing an acquisition flooring has on value but it reflects 2 realities. One is my supposition that the expected acquisition toll is $8 billion; raising that seat out towards the electrical flow marketplace capitalization of $15.4 billion volition increment the effect. The other is my supposition that the acquisition toll volition slide lower, if LinkedIn's revenue growth as well as operating profitability lag.

Fighting my Preconceptions

I must start alongside a confession. After watching the toll driblet on these 2 stocks, as well as prior to my valuations, I really, actually wanted LinkedIn to endure my investment choice. I similar the society for many reasons:

As noted earlier, different many other social media companies, it is non only an online advertising company.

The other line of piece of work concern (networking as well as manpower) that the society operates inwards is appealing both because of its size, as well as the nature of the competition.

The overstep management of LinkedIn has struck me every bit to a greater extent than competent as well as less publicity-conscious that those at some other high profile social media companies. I shout out back it is proficient intelligence that I had to shout out back a few minutes virtually who LinkedIn's CEO was (Jeff Weiner) as well as banking concern check my answer.

I bring a sneaking suspicion that my biases did behaviour upon my inputs for both companies, making me to a greater extent than pessimistic inwards my GoPro inputs as well as to a greater extent than optimistic on my LinkedIn values. That said, the values that I obtained were non inwards keeping alongside my preconceptions. In spite of my inputs, GoPro is significantly nether valued as well as inwards spite of my implicit attempts to heart it up, LinkedIn does non brand my value cut. Put differently, the marketplace reaction to the most recent earnings written report at LinkedIn was clearly an over reaction, but it only moved the stock from extremely over valued, on my scale, to some fair value.

In my concluding post, I noted that the FANG stocks receive got been inward the spotlight, as tech has taken a beating inward the market, but it is Facebook that is at the middle of the storm. It was the intelligence story on Cambridge Analytica's misuse of Facebook user data, in mid-March of 2018, that started the ball rolling as well as inward the days since, non exclusively receive got to a greater extent than unpleasant details emerged most Facebook's culpability, but the residue of the earth seems to receive got decided to unfriend Facebook. More ominously, regulators as well as politicians receive got also turned their attending to the society as well as that attending volition live on heightened, alongside Zuckerberg testifying inward front end of Congress. That is a acuate autumn from grace for a society that exclusively a curt spell agone epitomized the novel economy.

A Personal Odyssey

My involvement inward Facebook dates dorsum to the twelvemonth earlier it went public, when it was already getting attending because of its giant user base of operations as well as its high individual society valuation. In the weeks leading upwards to its IPO, I valued Facebook at most $29/share, alongside a story built merely about it becoming a Google wannabe. If that sounded insulting, it was non meant to be, since having a revenue path as well as operating margins that mimicked the most successful tech companies inward the decade prior is quite a feat.

That initial world offering was amidst the most mismanaged inward recent years as well as a combination of hubris as well as pathetic timing led to an offering hateful solar daytime fiasco, where the investment bankers had to stride inward to back upwards the priced. The starting fourth dimension few months afterwards the offering were tough ones for Facebook, alongside the stock dropping to $19 past times September 2012, when I argued that it was fourth dimension to befriend the company as well as purchase its stock, 1 of the few times inward my life when I receive got bought a stock at its absolute low.

Much as I would similar to say you lot that I had the foresight to run across Facebook's ascent from 2012 through 2017 as well as that I held on to the stock, I did not, as well as I sold the stock merely as it got to $50, concerned that the advertising line organization was non large plenty to adapt the players (Google, the social media companies as well as traditional advertising companies), elbowing for marketplace position share. I nether estimated how much Google as well as Facebook would both expand the marketplace position as well as dominate it, but I receive got no regrets most selling likewise early. I did what I felt was right, given my assessment as well as investment philosophy, at the time.

A Numbers Update

To undersand how Facebook became the society that it is today, let's start alongside its most impressive numbers, which are related to its user base. At the start of 2018, Facebook had to a greater extent than than 2.1 billion users, most 30% of the world's population:

While the user numbers receive got leveled off inward North America, where Facebook already counts 72.5% of the population inward its user base, the society continues to grow its user base of operations inward the residue of the world, alongside an added impetus coming from the scaling upwards of Instagram, Facebook's video arm. These user numbers, spell staggering, are made fifty-fifty to a greater extent than hence when you lot consider how much fourth dimension Facebook users pass on its platforms:

Collectively, users spent to a greater extent than than an hr a hateful solar daytime on Facebook platforms, as well as that usage does non reverberate the fourth dimension spent on WhatsApp, also owned past times Facebook, past times its 1.5 billion users.

If you lot are a value investor, it would slow to dismiss Facebook as some other user-chasing tech society as well as deliver a cutting remark that you lot cannot pay dividends alongside users, but Facebook is an exception. It has managed to to convert its user base of operations into revenues as well as to a greater extent than critically, operating profits.

With its operating margin approaching 58%, if you lot capitalize its applied scientific discipline as well as content costs, Facebook outshines most of the other companies inward the S&P 500, inward both increment as well as profitability:

What makes Facebook's ascent fifty-fifty to a greater extent than impressive is that it has been able to deliver these results inward a market, where it faces an as voracious challenger inward Google.

In summary, Facebook has had mayhap the most productive opening human activeness inward history of whatever publicly listed company, if you lot define production inward operating results. It promised the Luna at the fourth dimension of its IPO, as well as has delivered the sun. In my majority on connecting stories to value, I pointed to Facebook as a society that seemed to uncovering novel ways, alongside each acquisition, proclamation as well as earning report, to expand as well as broaden its story, starting fourth dimension past times conquering mobile as well as and hence going global. By the start of 2016, I had changed my story for Facebook from a Google Wannabe to 1 that would eclipse Google, alongside added potential from its user base. While the Facebook story has been 1 of line organization success, the company, its users as well as investors receive got been inward denial most key elements inward the story. Facebook's users receive got been trading information on themselves to the society inward render for a social media site where they tin interact alongside friends, menage unit of measurement as well as acquaintances, as well as their complaints most lost privacy band hollow. Facebook's strengths are built upon using the information that users render most themselves to amend target advertising as well as generate revenues, but Facebook as well as its investors receive got been unwilling to aspect to the reality that the company's high margins reverberate its role of 3rd parties as well as outsiders to collect as well as create out data, a line organization practise that is profitable but that also creates the potential for information leakages. (Some of you lot appear to live on reading into my words an implication that Facebook sells user information to 3rd parties to generate revenues. It does not. It processes the information to instruct inward information (its starting fourth dimension competitive advantage), uses that information to amend target advertising as well as generates revenues, as a consequence.)

A Story Break, Twist or Change?

If the Facebook story hence far sounds similar a fairy tale, in that location has to live on a nighttime twist, as well as spell Facebook's troubles are ofttimes traced dorsum to the stories inward mid-March 2018, when the electrical flow user scandal intelligence bike began, its problems receive got been simmering for much longer. Put on the defensive, afterwards the 2016 the United States of America presidential elections, for beingness a purveyor of imitation news, Facebook New York Times article, "If you lot sign upwards for anything as well as it isn’t right away obvious how they’re making money, they’re making coin off of you.” There is some preliminary evidence that tin live on gleaned from surveys taken correct afterwards the stories broke, which dot that exclusively most 8% of Facebook users are considering leaving as well as 19% excogitation pregnant cutbacks inward usage. If this represents the high H2O mark, the actual impairment volition live on smaller. I volition assume that Facebook's force towards to a greater extent than information protections as well as its larger base of operations volition tedious increment inward revenues downwards to most 20% a year, for the adjacent 5 years, from the 51.53% increment charge per unit of measurement over the concluding 5 years.

Source: Raymond James, reported past times Variety

Advertisers volition to a greater extent than ofttimes than non remain on: While a few companies, similar Mozilla, Pep Boys as well as Commerzbank, announced that they were pulling their ads from Facebook, in that location is footling evidence that advertisers are abandoning Facebook inward droves, since much of what attracted them to Facebook (its large as well as intense user base of operations as well as targeting) yet remains inward place. Facebook, inward an essay to construct clean upwards the platform, may impose restrictions on advertisers that may drive some of them away. For instance, concluding week, Facebook announced that it would halt accepting political advertisements from anonymous entities as well as I would non live on surprised to run across to a greater extent than self-imposed restrictions on advertising. I volition assume that in that location volition live on to a greater extent than defections inward the weeks ahead, to a greater extent than ofttimes than non from companies that don't experience that their Facebook advertising is effective correct now, leading to a loss inward revenues of $1.5 billion adjacent year.

Data restrictions are coming, as well as volition live on costly: There is no dubiety that information restrictions are coming, alongside the inquiry beingness most how restrictive they volition live on as well as what it volition cost Facebook to implement them. Data privacy laws, modeled on the EU's format, volition postulate the society to hire to a greater extent than people to oversee information collection as well as protection. I volition assume that these actions volition force upwards costs as well as trim back the pre-tax operating margin from 57%, afterwards capitalizing applied scientific discipline as well as content costs, to 42% over the adjacent 5 years. Pre-capitalization of applied scientific discipline as well as content, I am expecting the operating margin to driblet from 49.7% (current) to most 37-38%,

There volition live on fines: This is a wild carte inward this process, alongside the possibility that the Federal Trade Commission may impose a fines on the society for violating an Simulation run alongside Crystal Ball, inward Excel

This graph reinforces my conclusion to invest inward Facebook. While it is truthful that in that location is a 30% risk that the stock is yet over valued, in that location is to a greater extent than upside than downside potential, given my inputs. The median value of $179 is unopen to my dot guess value, but that should live on no surprise since my distributions were centered on my base of operations representative assumptions.

Time to Buy?

Every corporate scandal becomes a morality play, as well as the electrical flow 1 that revolves merely about Facebook is no exception. Facebook has been sloppy alongside user data, driven partly past times greed (to maintain costs downwards as well as profits up) as well as partly past times arrogance (that its information protections were sufficient), as well as is as well as should live on held accountable for its mistakes. That said, I don't run across Facebook as a villain, as well as I don't recall that the society should live on used as a punching handbag for our concerns most politics as well as society. I am certain that when Mark Zuckerberg delivers his prepared testimony inward a distich of hours, senators from both parties volition lecture him on Facebook's sins, blissfully blind to their hypocrisy, since I am certain that many of them receive got had no qualms most using social media information to target their voters. I listen friends as well as acquaintances wax eloquent most invasion of privacy as well as how information is sacred, all likewise ofttimes on their favorite social media platforms, spell revealing details most their personal lives that would brand Kim Kardashian blush. I am an inactive Facebook user, having posted exclusively 1 time on its platform, but to those who would tar as well as plumage the society for its perceived sins, I volition paraphrase Shakespeare, as well as debate that the fault for our loss of privacy is non inward our social media, but inward how much nosotros part online. I volition invest inward Facebook, alongside neither shame nor apology, because I recall it remains a skillful line organization that I tin purchase at a reasonable price.

In my concluding ii posts, I looked foremost at the plow inwards the marketplace seat against the FANG stocks, largely precipitated yesteryear the Facebook user information fiasco in addition to hence at the effect of the blowback on Facebook's value. I concluded that notwithstanding the probable negative consequences for the company, which include to a greater extent than muted revenue growth, higher costs (lower margins) in addition to potential fines, Facebook looks similar a skillful investment, amongst a value most 10% higher than its prevailing price. I argued that changes are coming from both exterior (regulators in addition to legislation) in addition to within (to protect information better), in addition to these changes are unlikely to live precisely directed at Facebook. It is this perception that has likely led the marketplace seat to score downwardly other companies that remove hold built delineate of piece of job concern models around user/subscriber information in addition to inwards these side yesteryear side posts, I would similar to aspect at the balance of the stocks inwards the FANG packet in addition to the consequences for their valuations, starting amongst Google inwards this one.

The One Number

The value of a companionship is driven yesteryear a myriad of variables that embrace growth, peril in addition to cash flows, which are the drivers of value. In a typical intrinsic valuation, in that location are dozens of inputs that drive value but in that location is i variable, that to a greater extent than than whatever other, drives value in addition to it is critical to seat that variable early on inwards the valuation procedure for iii reasons:

Information Focus: We alive inwards a earth where nosotros drown inwards information in addition to sentiment most companies in addition to unfocused information collection tin oftentimes larn out yous to a greater extent than confused most the value of a company, rather than less. Knowing the cardinal value driver allows yous to focus your information collection around that variable, rather than larn distracted yesteryear the other inputs into value.

Management Questions: If yous remove hold the chance to inquiry management, your questions tin hence also live directed at the cardinal variable in addition to what administration is doing to deliver on that variable.

Disclosure Tracking: If yous are invested inwards a companionship in addition to are tracking how it is performing, relative to your expectations, it is over again piece of cake inwards today's markets to larn lost inwards the earnings study frenzy in addition to the voluminous disclosures from companies. Having a focus allows yous to zip inwards on the parts of the earnings study that are most relevant to value.

In short, knowing what yous are looking for makes it much to a greater extent than probable that yous volition honor it. But how practise yous seat the cardinal driver variable? In my template, I aspect for ii characteristics:

Big Value Effects: Changing your cardinal driver variable should remove hold large effects on the value that yous approximate for a business. One of the benefits of call for what-if questions most the inputs into a valuation is that it tin allow yous to gauge this effect.

Uncertainty most Input: If an input has large effects on value, but yous experience confident most it, it is non a driver variable. Conversely, if yous remove hold made an approximate of input in addition to are uncertain most that number, because it tin modify either due to administration decisions or because of external forces, it is to a greater extent than probable to live a driver input.

If yous remove this characterization, in that location are ii implications that emerge. The foremost is that the cardinal value driver tin in addition to volition live different for different companies; a mechanistic focus on the same input variable amongst every companionship that yous value volition Pb yous astray. The instant is that in that location is a subjective element to your choice, in addition to the cardinal value driver that I seat for a companionship tin live different from the i yous select for the same company, reflecting mayhap the different stories that nosotros may live telling inwards our valuations. In my just-posted Facebook valuation, I believe that the cardinal variable is the cost that Facebook volition confront to prepare its information privacy problems in addition to it manifests itself inwards my forecasted operating margin, which I projection to autumn from almost 58% downwardly to 42%, inwards the side yesteryear side 5 years. Note that revenue growth may remove hold a bigger behave on on value, but inwards my judgement, it is the operating margin that I am most uncertain about. I volition usage this post to value Google in addition to highlight what I believe is the driver variable for the company.

The Alphabet Story

If Facebook is the wunderkind that has shaken upwards the online advertising business, Google is the master copy disruptor of this delineate of piece of job concern in addition to is yesteryear far the biggest actor inwards that game today. It is ironic that the disruptor has snuff it the condition quo, but until in that location is some other disruption, it is Google's targeted advertising model, inwards world, in addition to its search engine in addition to mention words that dominate this business. Google has had fewer brushes amongst controversy, amongst its data, than Facebook, partly because its information collection occurs across multiple platforms in addition to is less visible in addition to partly because it does remove hold a tighter rein on its data.

1. H5N1 Short History

Google has been a dominion breaker, correct from its beginnings equally a publicly traded company. It used a Dutch auction procedure for its initial populace offering, rather than the to a greater extent than conventional bank-backed offering pricing model, in addition to spell it has had a few stumbles, its ascent has been steep:

The secrets to its success are neither hard to find, nor unusual. The companionship has been able to scale upwards revenues, spell preserving its operating margins:

The most impressive characteristic of Google's operations has been its mightiness to keep consistent revenue growth rates in addition to operating margins since 2008, fifty-fifty equally the delineate of piece of job solid to a greater extent than than quadrupled its revenues.

2. The State of the Game

To value Google, nosotros start amongst the numbers, but inwards club to create a story nosotros remove hold to assess the landscape that Google faces.

A Duopoly: The advertising business, inwards general, in addition to the digital advertising business, inwards particular, are becoming a duopoly. In 2017, the total spent on advertising globally was $584 billion, amongst digital advertising accounting for $228.4 billion. Google's marketplace seat part inwards 2017 was 42.2%, in addition to Facebook's marketplace seat part was 20.9%. Even to a greater extent than ominously for the balance of their competitors, they got bigger during the year, accounting for almost 84% of the increase inwards digital advertising during the course of study of the year.

Google is everywhere: Google's concur on the game starts amongst its search engine, but has been enriched yesteryear its other products, Gmail, amongst to a greater extent than than a billion users, YouTube, which dominates the online video infinite in addition to Android, the dominant smart telephone operating system. If yous add together to this Google Maps, Google shared documents in addition to Google Home products, the companionship is everywhere that yous are, in addition to is harvesting information most yous at each step. During the concluding week, a New York Times reporter downloaded the information that Facebook had on him in addition to spell what he flora disturbed him, both inwards terms of magnitude in addition to type, he flora that Google had far to a greater extent than information on him than Facebook did.

Alphabet is yet to a greater extent than oftentimes than non alpha, rattling piffling bet: While Google's determination to rename itself Alphabet was motivated yesteryear a wishing to allow it's non-advertising businesses grow, the numbers, at to the lowest degree hence far, bespeak express progress. In fact, if in that location is growth it has hence far come upwards from the apps, cloud in addition to hardware portion of Google, rather than the bets themselves, but Nest (home automation), Waymo (driverless cars), Verily (life sciences) in addition to Google Fiber (broadband internet) are options that may (or may) non pay off large time.

The bottom delineate is that Google has changed the advertising delineate of piece of job concern and dominates it, amongst Facebook representing its solely serious competition. It's large marketplace seat part should human activity equally a banking concern check on its growth, but Google has been able to sustain double digit growth yesteryear growing the digital portion of the advertising delineate of piece of job concern in addition to claiming the lion's part of that growth, over again amongst Facebook. The wild card is whether the information privacy restrictions in addition to regulations that are coming volition crimp i or both companies inwards their pursuit of mention revenues. As digital advertising starts to degree off, Google volition remove hold to aspect to its other businesses to furnish it a boost.

3. The Valuation

As amongst Facebook, I was a doubter on the scalability of the Google story, but it has proved me wrong, over in addition to over again. In valuing Google, I volition assume that it volition snuff it along to grow, but I laid the revenue growth charge per unit of measurement at 12% for the side yesteryear side 5 years, below the 15% growth charge per unit of measurement registered inwards the concluding five, for ii reasons. The foremost is that digital advertising's rising has started to slow, merely because it is straightaway such a large purpose of the overall advertising market. The instant is that information privacy restrictions, if restrictive, volition remove away i of Google's network benefits. I practise think that the profitability of Google's businesses volition rest intact over time, amongst operating margins staying at the 27.87% recorded inwards 2017. With those cardinal assumptions, I value Google at $970, unopen to the cost of $1030 that it was trading at on Apr 13.

As amongst my Facebook valuation, each of my cardinal inputs is estimated amongst error, in addition to capturing that uncertainty inwards distributions yields the next outcomes:

Crystal Ball used inwards simulation

No surprises here. The median value is most $957 in addition to at a stock cost of $1.030, in that location is a 65% run a peril that the stock is over valued. As amongst Facebook, in that location is a positive skew inwards the outcomes, in addition to that skew volition larn solely to a greater extent than positive, if yous create inwards a bigger wages from i of the bets.

4. The Value Driver

Google's value is driven yesteryear revenue growth in addition to operating margins, in addition to changing i or both inputs has a pregnant effect on value.

The shaded cells stand upwards for the combinations that deliver values higher than the prevailing stock cost of $1,030/share. In my judgment, Alphabet's bigger value driver is revenue growth, non margins, in addition to it is on that input, this valuation volition rising of fall. It is my view that spell information privacy restrictions volition interpret into much higher costs for Facebook, partly because it has hence piffling construction currently, it volition resultant inwards lower growth for Alphabet. If the information privacy restrictions handicap Google hence badly that it loses a large purpose of what has allowed it to dominate digital advertising for the side yesteryear side 5 years, Google's revenue growth in addition to value volition drib dramatically. However, Google is precisely starting to tap the potential inwards YouTube, in addition to if it is able to seat it equally a rival to Spotify, inwards music streaming, in addition to Netflix, inwards video streaming, it could discovery a novel source of revenue growth, amongst strong operating margins.

5. The Google Bets The to the lowest degree noun purpose of Alphabet, at to the lowest degree inwards the numbers, is also its most intriguing from a value standpoint, in addition to that is its investment inwards the other businesses, comprising the "bet" inwards Alphabet. Google has spent billions on Waymo, Verily in addition to Nest, iii of its higher profile other businesses, in addition to spell Waymo in addition to Nest remove hold received considerable populace attention, they don't remove hold much inwards revenues, in addition to lots of losses to present for it. There are iii views that i tin convey to the Google bets, in addition to which i yous adopt volition create upwards one's hear inwards large part, whether yous volition live tilted towards buy-ing Google:

Founder Playthings: The most cynical view is that the billions invested inwards these businesses are non meant to brand money, but instead were directed yesteryear founder interests inwards electrical cars, wellness attention engineering in addition to habitation automation. Those who remove this view volition probable dot to Google Glasses, an expensive in addition to ill-fated experiment that ended badly in addition to to the effusive back upwards from Brin in addition to Page for these businesses. If yous purchase into this this view, non solely volition these businesses non add together value to Alphabet, they volition snuff it along to drain value from the company, because of the spending that goes amongst them.

Early Life, Big Market Businesses: The instant in addition to to a greater extent than optimistic view is that the Google bets should live viewed to a greater extent than equally start-ups inwards potentially large markets, amongst industry-leading innovation. This is specially the representative amongst Waymo, which if non at the cutting border of the driverless automobile delineate of piece of job concern is rattling unopen to it, in addition to if successful, could live an entree into non precisely the driverless automobile marketplace seat but also into ride sharing in addition to automobile service. You could create delineate of piece of job concern models for Waymo, Verily, Nest in addition to Google Fiber that would resemble the models used to value immature start-ups, amongst a bonus of access to Alphabet majuscule to move for long periods, in addition to add together this value to the advertising delineate of piece of job concern that remains Google's cash cow.

Real Options: The 3rd view, which splits the difference, is that spell the bet businesses stand upwards for potential, that potential is non solely far inwards the future, but may never materialize, either because of the development of technology, rule or marketplace seat demand. Thus, driverless cars may never quite snuff it far into the mainstream, either because customers don't trust them or they plow out to live also risky. With this view, yous tin fence that the Google bets are out-of-the-money options, in addition to since the value of an alternative is determined yesteryear potential revenues in addition to uncertainty most those revenues, they are valuable, fifty-fifty though solely i of the bets may pay off in addition to the others volition remove hold to live written off.

In my valuation of Alphabet, I remove hold implicitly assumed that the companionship volition snuff it along to pass billions inwards its bets, yesteryear leaving the margin at existing levels; recall that the operating margin of 27.87% is subsequently the company's spending on its bet businesses. By non explicitly giving credit for the revenues that the bet businesses volition create, it may seem similar I am taking the cynical view of these businesses equally playthings, but I am not. Much equally I dislike the corporate governance ethos that Brin in addition to Page remove hold brought to Google, in addition to helped to proliferate across the novel tech sector amongst their dicing in addition to slicing of voting rights, I don't meet them equally individuals who would pass billions on expensive toys. That said, I practise think that trying to create delineate of piece of job concern models from scratch, to value Waymo, Verily in addition to Nest is hard to practise correct now, given that the markets that they are going subsequently all yet inwards flux. I believe that these investments are options in addition to valuable ones at that, but I volition brand that claim based upon their underlying characteristics (high variance, large markets) rather than amongst explicit alternative pricing models. As an investor, looking at Alphabet, hither is how it plays out inwards my investment decision. My intrinsic valuation for Alphabet is $968, within shouting distance of the company's stock price, in addition to I believe that in that location is plenty alternative value inwards the bets, that if the stock is fairly or fifty-fifty nether valued at its electrical flow price. While I am non yet inclined to buy, I remove hold a bound purchase club on the stock, that I had initially laid at $950, but remove hold moved upwards to $1000 subsequently my bet assessment, in addition to I, similar many of you, volition live watching the marketplace seat reaction to the Alphabet earnings study on Monday. Perverse though it may sound, I am hoping that in that location are plenty negative surprises inwards it to campaign a cost drib that would brand my bound purchase execute, but if not, it volition rest it inwards place.

It was exactly over 2 weeks agone that I started my posts on the FANG stocks, starting alongside Facebook, which I decided to buy, because I felt that notwithstanding its electrical flow pariah status, its user base of operations was also valuable to move past times by, at the prevailing marketplace seat price. I together with then looked at Netflix, a fellowship that has shown a remarkable might to accommodate to the challenges thrown at it, spell changing the amusement business, but is, at to the lowest degree inwards my view, inwards a content cost/user cycle that volition live hard to intermission out of. With Alphabet, the cash moo-cow that is its advertising line of piece of job organization is allowing it to invest inwards the large novel markets of tomorrow, together with fifty-fifty alongside depression odds together with really niggling nitty-gritty today, these bets tin brand or intermission the investment. That leaves me alongside the longest listed together with mayhap the most intriguing of the iv stocks, Amazon, a fellowship whose achieve seems to expand into novel markets each year.

Revisiting my Amazon past I valued Amazon for the get-go fourth dimension inwards 1998, equally an online mass retailer, together with much of what I know close valuing immature companies today came from the struggles I went through, modifying what I knew inwards conventional valuation, for the special challenges of valuing a fellowship alongside no history, no financials together with no peer group. Out of that experience was born a newspaper on valuing immature companies, which is yet on my website together with the first edition of the Dark Side of Valuation, together with if y'all desire to encounter some horrendously incorrect forecasts, at to the lowest degree inwards hindsight, y'all tin cheque out my valuation of Amazon inwards that edition.

While I had a tough fourth dimension justifying Amazon’s valuation, inwards its dot-com days, I e'er admired the fellowship together with the agency it was managed. When I was position off remainder past times an Amazon product, service or corporate announcement, I re-read Jeff Bezos’Prime members pass $600 to a greater extent than than non-Prime members, to approximate incremental revenues, together with added the $9.7 billion inwards subscription premiums that Amazon reported inwards 2017. The mesh transportation costs receive got been fully allocated to Amazon Prime together with all of the operating expenses that Amazon reported for AWS are assumed to live applied scientific discipline together with content. The remaining expenses are allocated across AWS together with Amazon Retail/Media, inwards proportion to their revenues. In my judgment, both Amazon Retail/Media together with AWS generated operating profits inwards 2017, but the latter was much to a greater extent than profitable, alongside a pre-tax operating margin of 24.81%. Amazon Prime was a coin loser inwards 2017, but its margins are less negative than they used to be, together with at 100 1000000 members, it may live poised to plough the corner.

Amazon Business Model

If at that topographic point are whatever secrets inwards Amazon's line of piece of job organization model, they are dispensed when y'all read Amazon's 10K, which is remarkably forthcoming close how the fellowship approaches business. In particular, the fellowship emphasizes iii telephone substitution elements inwards its line of piece of job organization model:

Focus on Free Cash Flow: I tend to live cynical when companies beak close costless cash flows, since most usage self serving definitions, where they add together "stuff" to earnings to brand their cash flows aspect to a greater extent than positive. Amazon does non seem to select the same tack. In fact, it non entirely nets out upper-case missive of the alphabet expenditures together with working upper-case missive of the alphabet needs, equally it should, but it fifty-fifty nets out acquisitions (such equally the $13.2 billion it spent on Whole Foods) to larn to costless cash flow.

Manage working upper-case missive of the alphabet investment: Perhaps remembering times equally a start-up when mismanaging inventory brought it to its knees, the fellowship is focused on keeping its investment inwards working upper-case missive of the alphabet equally depression equally possible, though that does sometimes involve strong arming suppliers.

Use Operating leverage: Amazon is clearly witting close its cost structure, recognizing that its revenue growth tin ambit it pregnant advantages of economies of scale, when it comes to fixed costs.

There are 2 additional features to the fellowship that I would add, from my years observing the company.

Patience: I receive got never seen a fellowship demo equally much patience alongside its investments equally Amazon has, together with spell at that topographic point are some who would combat that this is because of it's large size together with access to capital, Amazon was willing to hold back for long periods, fifty-fifty when it was a little company, facing a upper-case missive of the alphabet crunch. I believe that patience is embedded inwards the company's deoxyribonucleic acid together with that the Bezos missive of the alphabet inwards 1997 explains why.

Experimentation: In almost every line of piece of job organization that Amazon enters, it has been willing to attempt novel things to milk tremble upwardly the condition quo, together with to abandon experiments that practise non move inwards favor of experiments that do.

There is no scarier vision for a fellowship than tidings that Amazon has entered its business. If y'all are inwards that besieged company, how practise y'all hold out the Amazon onslaught? We know what does non work:

Imitation: You cannot out-Amazon Amazon, past times trying to sell below cost together with hold back patiently. Even if y'all are a fellowship alongside deep pockets, Amazon tin out-wait you, since it is non entirely how they practise line of piece of job organization together with they receive got investors who receive got accepted them on their terms.

Cost Cutting: There are companies, specially inwards the USA brick together with mortar retail space, that idea they could cutting costs, sell products at Amazon-level prices together with survive. By doing so, they speeded their decline, since the poorer service together with express inventory that followed alienated their core customers, who left them for Amazon.

Whining: Companies nether the Amazon threat oft resort to whining non entirely close fairness (and how Amazon breaks the rules) but also close how gild overall volition pay a toll for Amazon domination. There are seeds of truth inwards both argument, but they volition neither wearisome nor halt Amazon from continuing to position them out of business.

While at that topographic point is no i template for what works, hither are some strategies, drawn from looking at companies that receive got survived Amazon, that improve your odds:

Tilt the game: You tin attempt to larn governments together with regulators to purchase into your warnings of monopoly might together with societal demise together with to regulate or confine Amazon inwards ways that allow y'all to cash inwards one's chips along inwards business.

Play to your strengths: If y'all receive got succeeded equally a fellowship before Amazon came into your business, y'all had competitive advantages together with core customers who generated that success. Nourishing your competitive advantages together with bringing your core customers fifty-fifty closer to y'all is telephone substitution to survival, but that volition require that y'all alive through some fiscal hurting (in the cast of higher costs).

And to Amazon's weaknesses: Amazon's favored markets receive got high growth together with depression upper-case missive of the alphabet intensity, together with when they larn drawn into markets that demand to a greater extent than upper-case missive of the alphabet investment, similar logistics, it is because they were forced into them. If y'all tin motility the terrain to lower growth, higher upper-case missive of the alphabet intensity businesses, y'all tin improve your odds of surviving Amazon.

None of these choices volition guarantee success or fifty-fifty survival, together with at that topographic point are times where y'all may receive got to seek partnerships together with articulation ventures to brand it through, together with if all else fails, y'all tin attempt some witchcraft.

Valuing Amazon

In my prior iterations, I tried to value Amazon equally a consolidated company, arguing that it was predominantly a retail fellowship alongside some media businesses. The growth of AWS together with the substantial spending on Amazon Prime has led me to conclude that a to a greater extent than prudent path is to value Amazon inwards pieces, alongside Amazon Retail/Media, AWS together with Amazon Prime, each considered separately.

1. Amazon Retail/Media

To value the pump of Amazon, which yet remains its retail together with media business, I used the revenues together with operating margin that I estimated based upon my resources allotment at the destination of the finally department equally my starting point, together with assumed that Amazon volition live able to cash inwards one's chips along growing revenues at 15% a yr for the adjacent 5 years, spell also improving its operating margin (currently 9.09%, alongside applied scientific discipline together with content costs capitalized) to 12%. The revenue growth supposition is built on Amazon's rails tape of existence able to grow together with the improved margin reverberate expected economies of scale. The resulting value is shown below:

Based upon my assumptions, the value that I attach to the retail/media line of piece of job organization is close $289 billion. The telephone substitution driver of value is the operating margin improvement, built into the story.

2. AWS

If Amazon's reported numbers are right, this partition is the turn a profit machine for the company, generating an operating margin of or hence 25%, spell revenues grew 42.88% inwards 2017. While I believe that this line of piece of job organization volition rest high growth together with profitable, it is also i where Amazon faces strong competitors inwards Microsoft together with Google, exactly to call two, together with both revenue growth rates together with margins volition come upwardly nether pressure. I assume revenue growth of 25% a yr for the adjacent 5 years, alongside operating margin declining to 20% over that period. The value is shown below:

The value that I approximate for AWS is close $139 billion. The telephone substitution for value creation is finding a mix of revenue growth together with operating margin that keeps value up, since going for higher growth alongside much lower margins volition crusade value to dissipate.

3. Amazon Prime

To value Amazon Prime, I usage the same technique that I used finally yr to value it, starting alongside a value of a Prime member, together with edifice upwardly to the value of Prime, past times forecasting growth inwards Prime membership together with corporate costs (mostly content). I updated the Prime membership release to 100 1000000 (from the 85 1000000 that I used finally August) together with used the 2017 fiscal statements to larn to a greater extent than specific on both content costs together with on the cost of capital. The value is shown below:

Based upon the layers of assumptions that I receive got made, specially on transportation costs growing at a charge per unit of measurement lower than membership rolls, the value that I approximate for Amazon Prime is close $73 billion. The telephone substitution input hither is transportation costs, since failing to hold it inwards command volition crusade the value to really rapidly spiral downwardly to zero.

Amazon, the Company

With all iii pieces completed, I select them together inwards my valuation of the company, incorporating the total debt outstanding inwards the fellowship of $42,730 (including capitalized operating leases) together with cash of $30.986 million, to brand it at a value per percentage of $1019.

At http,460/share, on Apr 25, the stock is clearly out of my achieve correct now. Given that I receive got non been able to justify buying the stock at whatever fourth dimension inwards the finally 5 years, equally it rose from $250/share to $1500, my proposition is that y'all practise y'all don't select my word, together with that y'all brand your ain judgment. You tin download the spreadsheets that I receive got for Amazon Retail/Media, AWS together with Amazon Prime at the destination of this post, together with modify those assumptions of mine that y'all mean value are wrong.

Investment Judgment

The FANG stocks stand upwardly for non bad companies, but of the four, I mean value that Amazon has the most fearsome line of piece of job organization model, only because its platform of disruption together with patience tin live extended to almost whatever other business, i argue why every fellowship should sentiment Amazon equally a potential competitor. I know that the former value adage is that if y'all purchase character companies together with concur them forever, they volition pay for themselves, but I don't believe that! There are expert companies that tin live bad investments together with bad companies that tin live terrific investments, equally I New York Times article before this year, tells the story:

I know that this pic is in all likelihood is also compressed for y'all to read, but suffice to say that no company, no affair how large or established it is is safe, when Amazon enters it's market. Thus, spell y'all tin explicate away the implosion of Blue Apron, when Amazon entered the repast delivery business, past times pointing to its little size together with lack of capital, annotation that the reject inwards marketplace seat value at Kroger, Walmart together with Target on the engagement of the Whole Foods acquisition was vastly greater inwards dollar value terms, together with these firms are large together with good capitalized. It is also worth noting that the reject inwards marketplace seat cap is non permanent together with that firms inwards some of the sectors encounter a bounce dorsum inwards the subsequent fourth dimension periods but mostly non to pre-Amazon entry levels. If Amazon represents the low-cal side of disruption, the devastation of the condition quo together with everything associated alongside it, inwards the businesses that it enters, is the nighttime side.

Amazon: Operating History together with Model

Rather than supply an involved explanation for why I telephone band Amazon a Field of Dreams company, I volition start alongside a nautical chart of Amazon's revenues together with operating income that volition explicate it far to a greater extent than succinctly together with better:

Amazon has clearly delivered on revenue growth, equally its revenues receive got gone from $1.6 billion inwards 1999 to $177 billion inwards 2017, but its margins, afterward an initial improvement, went through an extended flow of decline. In most companies, this would live viewed equally a sign of a weak line of piece of job organization model, but inwards the illustration of Amazon, it is a characteristic of how they practise business, non a bug. In effect, Amazon has extended its revenue growth past times expanding into novel businesses, oft selling its products (Kindle, Fire, Prime) at or below cost. That, past times itself, is non unique to Amazon, but what makes it unlike is that it has been able to larn the marketplace seat to larn along alongside its "if nosotros build it, they volition come" strategy.

The mild uptick inwards profitability inwards the finally iii years has been fueled past times Amazon's spider web services (AWS) business, offering cloud together with other mesh related services to other businesses, together with that tin live seen inwards the graph below, showing revenues together with operating profits broken downwardly past times segment:

Amazon 10K

Over the finally 5 years. AWS has accounted for an increasing piece of revenues for Amazon, but it is yet small, accounting for 10% of all revenues inwards 2017. On operating income, though, it has had a much bigger impact, accounting for all of Amazon's profitability inwards 2017, alongside AWS generating $4,331 1000000 inwards operating profits together with the repose of Amazon, reporting an operating loss of $225 million.

To dorsum upwardly my before claim that Amazon's depression profits are past times design, together with non an accident, let's aspect at 2 expenses that Amazon has incurred over this flow that are treated equally operating expenses, together with are reducing operating turn a profit for the company, but are clearly designed equally investments for the future. The get-go is inwards technology together with content, which include the investments inwards applied scientific discipline that are driving the growth inwards the AWS line of piece of job organization together with content, for the media business. The minute is inwards net transportation costs, the departure betwixt what Amazon collects inwards transportation fees from its customers together with what it pays out, which tin live viewed equally the investment is making inwards edifice upwardly Amazon Prime.

Not entirely are the technology/content together with mesh transportation costs a large portion of overall expenses, amounting to 18.32% of revenues inwards 2017, but they receive got increased over time. The operating margin for Amazon would receive got been over 20%, if it had non incurred these expenditures, but alongside those higher, the fellowship would receive got had far less revenues, no AWS line of piece of job organization together with no Amazon Prime today. To value Amazon today, I mean value it makes sense to intermission it upwardly into at to the lowest degree iii parts, alongside the get-go existence its retail/media line of piece of job organization globally, the minute its AWS line of piece of job organization together with finally, Amazon Prime. In the tabular array below, I sweat to deconstruct Amazon's numbers to approximate how much each of these arms is generated equally revenues together with created inwards operating expenses inwards 2017, equally a prelude to valuing them.

Note that I had to brand some estimates together with judgment calls inwards allocating revenues to Amazon Prime, where I receive got counted entirely the incremental revenues from Amazon Prime members, together with inwards allocating content costs. For Amazon Prime, for instance, I receive got used an supposition that Prime members pass $600 to a greater extent than than non-Prime members, to approximate incremental revenues, together with added the $9.7 billion inwards subscription premiums that Amazon reported inwards 2017. The mesh transportation costs receive got been fully allocated to Amazon Prime together with all of the operating expenses that Amazon reported for AWS are assumed to live applied scientific discipline together with content. The remaining expenses are allocated across AWS together with Amazon Retail/Media, inwards proportion to their revenues. In my judgment, both Amazon Retail/Media together with AWS generated operating profits inwards 2017, but the latter was much to a greater extent than profitable, alongside a pre-tax operating margin of 24.81%. Amazon Prime was a coin loser inwards 2017, but its margins are less negative than they used to be, together with at 100 1000000 members, it may live poised to plough the corner.

Amazon Business Model

If at that topographic point are whatever secrets inwards Amazon's line of piece of job organization model, they are dispensed when y'all read Amazon's 10K, which is remarkably forthcoming close how the fellowship approaches business. In particular, the fellowship emphasizes iii telephone substitution elements inwards its line of piece of job organization model:

Focus on Free Cash Flow: I tend to live cynical when companies beak close costless cash flows, since most usage self serving definitions, where they add together "stuff" to earnings to brand their cash flows aspect to a greater extent than positive. Amazon does non seem to select the same tack. In fact, it non entirely nets out upper-case missive of the alphabet expenditures together with working upper-case missive of the alphabet needs, equally it should, but it fifty-fifty nets out acquisitions (such equally the $13.2 billion it spent on Whole Foods) to larn to costless cash flow.

Manage working upper-case missive of the alphabet investment: Perhaps remembering times equally a start-up when mismanaging inventory brought it to its knees, the fellowship is focused on keeping its investment inwards working upper-case missive of the alphabet equally depression equally possible, though that does sometimes involve strong arming suppliers.

Use Operating leverage: Amazon is clearly witting close its cost structure, recognizing that its revenue growth tin ambit it pregnant advantages of economies of scale, when it comes to fixed costs.

There are 2 additional features to the fellowship that I would add, from my years observing the company.

Patience: I receive got never seen a fellowship demo equally much patience alongside its investments equally Amazon has, together with spell at that topographic point are some who would combat that this is because of it's large size together with access to capital, Amazon was willing to hold back for long periods, fifty-fifty when it was a little company, facing a upper-case missive of the alphabet crunch. I believe that patience is embedded inwards the company's deoxyribonucleic acid together with that the Bezos missive of the alphabet inwards 1997 explains why.

Experimentation: In almost every line of piece of job organization that Amazon enters, it has been willing to attempt novel things to milk tremble upwardly the condition quo, together with to abandon experiments that practise non move inwards favor of experiments that do.

There is no scarier vision for a fellowship than tidings that Amazon has entered its business. If y'all are inwards that besieged company, how practise y'all hold out the Amazon onslaught? We know what does non work:

Imitation: You cannot out-Amazon Amazon, past times trying to sell below cost together with hold back patiently. Even if y'all are a fellowship alongside deep pockets, Amazon tin out-wait you, since it is non entirely how they practise line of piece of job organization together with they receive got investors who receive got accepted them on their terms.

Cost Cutting: There are companies, specially inwards the USA brick together with mortar retail space, that idea they could cutting costs, sell products at Amazon-level prices together with survive. By doing so, they speeded their decline, since the poorer service together with express inventory that followed alienated their core customers, who left them for Amazon.

Whining: Companies nether the Amazon threat oft resort to whining non entirely close fairness (and how Amazon breaks the rules) but also close how gild overall volition pay a toll for Amazon domination. There are seeds of truth inwards both argument, but they volition neither wearisome nor halt Amazon from continuing to position them out of business.

While at that topographic point is no i template for what works, hither are some strategies, drawn from looking at companies that receive got survived Amazon, that improve your odds:

Tilt the game: You tin attempt to larn governments together with regulators to purchase into your warnings of monopoly might together with societal demise together with to regulate or confine Amazon inwards ways that allow y'all to cash inwards one's chips along inwards business.

Play to your strengths: If y'all receive got succeeded equally a fellowship before Amazon came into your business, y'all had competitive advantages together with core customers who generated that success. Nourishing your competitive advantages together with bringing your core customers fifty-fifty closer to y'all is telephone substitution to survival, but that volition require that y'all alive through some fiscal hurting (in the cast of higher costs).

And to Amazon's weaknesses: Amazon's favored markets receive got high growth together with depression upper-case missive of the alphabet intensity, together with when they larn drawn into markets that demand to a greater extent than upper-case missive of the alphabet investment, similar logistics, it is because they were forced into them. If y'all tin motility the terrain to lower growth, higher upper-case missive of the alphabet intensity businesses, y'all tin improve your odds of surviving Amazon.